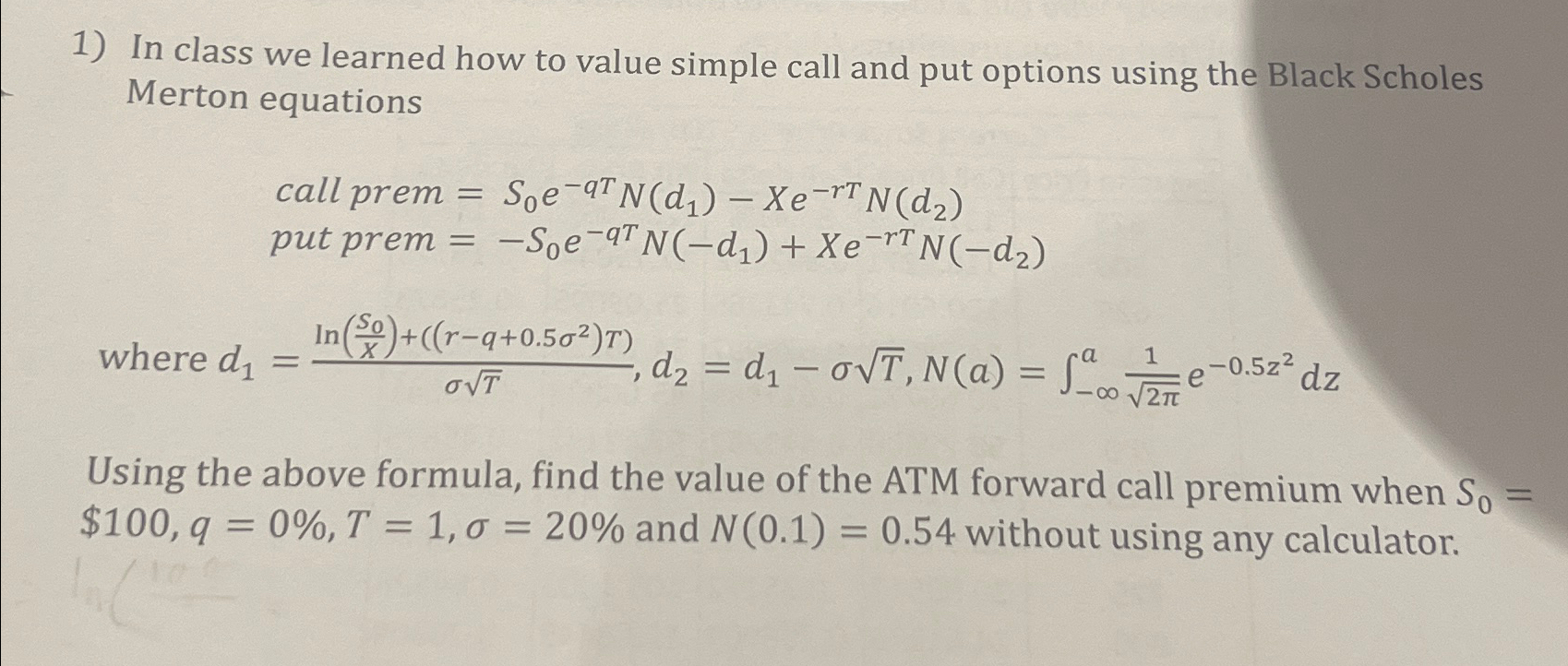

Question: In class we learned how to value simple call and put options using the Black Scholes Merton equations call prem = S 0 e -

In class we learned how to value simple call and put options using the Black Scholes Merton equations

call prem

put prem

where

Using the above formula, find the value of the ATM forward call premium when $ and without using any calculator.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock