Question: In excel link or file only DO NOT ANSWER IF NOT IN EXCEL LINK OR FILE / follow the format below. The transactions of the

In excel link or file only DO NOT ANSWER IF NOT IN EXCEL LINK OR FILE

/ follow the format below.

The transactions of the firm are as follows:

Edgar Detoya, tax consultant, began his practice on Dec. 1, 2019.

Dec.

1 Detoya invested P150,000 in the firm.

2 Paid rent for December to Recoletos Realty, P8,000.

2 Purchased supplies on account, P7,200.

3 Acquired P75,000 of office equipmeent, paying P37,000 down with the balance due in 30 days.

8 Paid P7,200 on account for supplies purchased.

14 Paid assistant's salaries for two weeks, P6,000.

20 Performed consulting services for cash, P20,000.

28 Paid assistant's salaries for two weeks, P6,000.

30 Billed clients for December consulting services, P48,000.

31 Detoya withdrew P12,000 from the business.

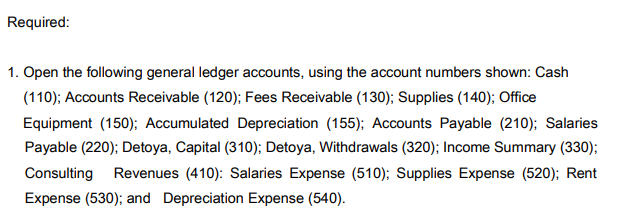

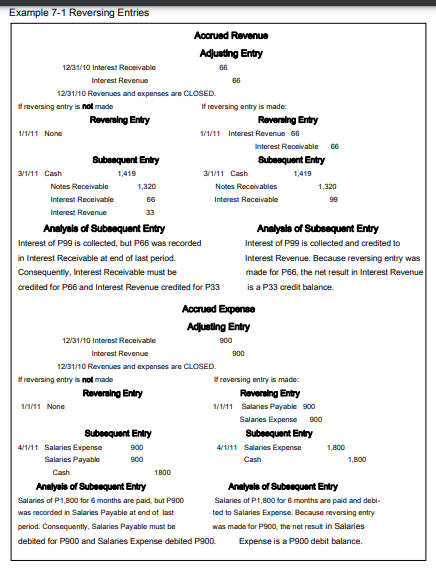

Required: 1. Open the following general ledger accounts, using the account numbers shown: Cash (110); Accounts Receivable (120); Fees Receivable (130); Supplies (140); Office Equipment (150); Accumulated Depreciation (155); Accounts Payable (210); Salaries Payable (220); Detoya, Capital (310); Detoya, Withdrawals (320); Income Summary (330); Consulting Revenues (410): Salaries Expense (510); Supplies Expense (520); Rent Expense (530); and Depreciation Expense (540).Example 7-1 Reversing Entries Accrued Revenue Adjusting Entry 12/31/10 Interest Receivable Interest Revenue 12/31/10 Revenues and expenses are CLOSED. If reversing entry is not made If reversing entry is made: Reversing Entry Reversing Entry 1/1/11 None 1/1/11 Interest Revenue 65 Interest Receivable Subsequent Entry Bubaaquant Entry 3/1/11 Cash 1,419 1/1/11 Cash 1,419 Notes Reochable 1,320 Notes Receivables 1 320 Interest Receivable Interest Receivable Interest Revenue Analysis of Subsequent Entry Analysis of Subsequent Entry Interest of P89 is collected, but P66 was recorded Interest of P89 is collected and credited to in Interest Receivable al end of last period. Interest Revenue. Because reversing entry was Consequently, Interest Receivable must be made for P86, the net result in Interest Revenue credited for P66 and Interest Revenue credited for P33 is a P33 credit balance. Accrued Expense Adjusting Entry 12/31/10 Interest Receivable 900 Interest Revenue 12/31/10 Revenues and expenses are CLOSED. If reversing entry is not made If reversing entry is made: Reversing Entry Reversing Entry 1MM1 None 1/1/11 Salaries Payable 900 Salaries Expense 900 Subsequent Entry Subsequent Entry 4/1/11 Salaries Expense 900 4/1/11 Salaries Expense 1,800 Salaries Payable 900 Cash 1,800 Cash 1800 Analyals of Subsequent Entry Analysis of Subarquant Entry Salaries of P1,800 for 6 months are paid, but P900 Salaries of P1,800 for 6 months are paid and debi- was recorded in Salaries Payable at end of last ted to Salaries Expense. Because reversing entry period. Consequently, Salaries Payable must be was made for P900, the net result in Salaries debited for P900 and Salaries Expense debited P900. Expense is a P900 debit balance

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!