In March 2010 Fernandez and Sicilia signed an LOI with an enterprise valuation of MX $389 million

Question:

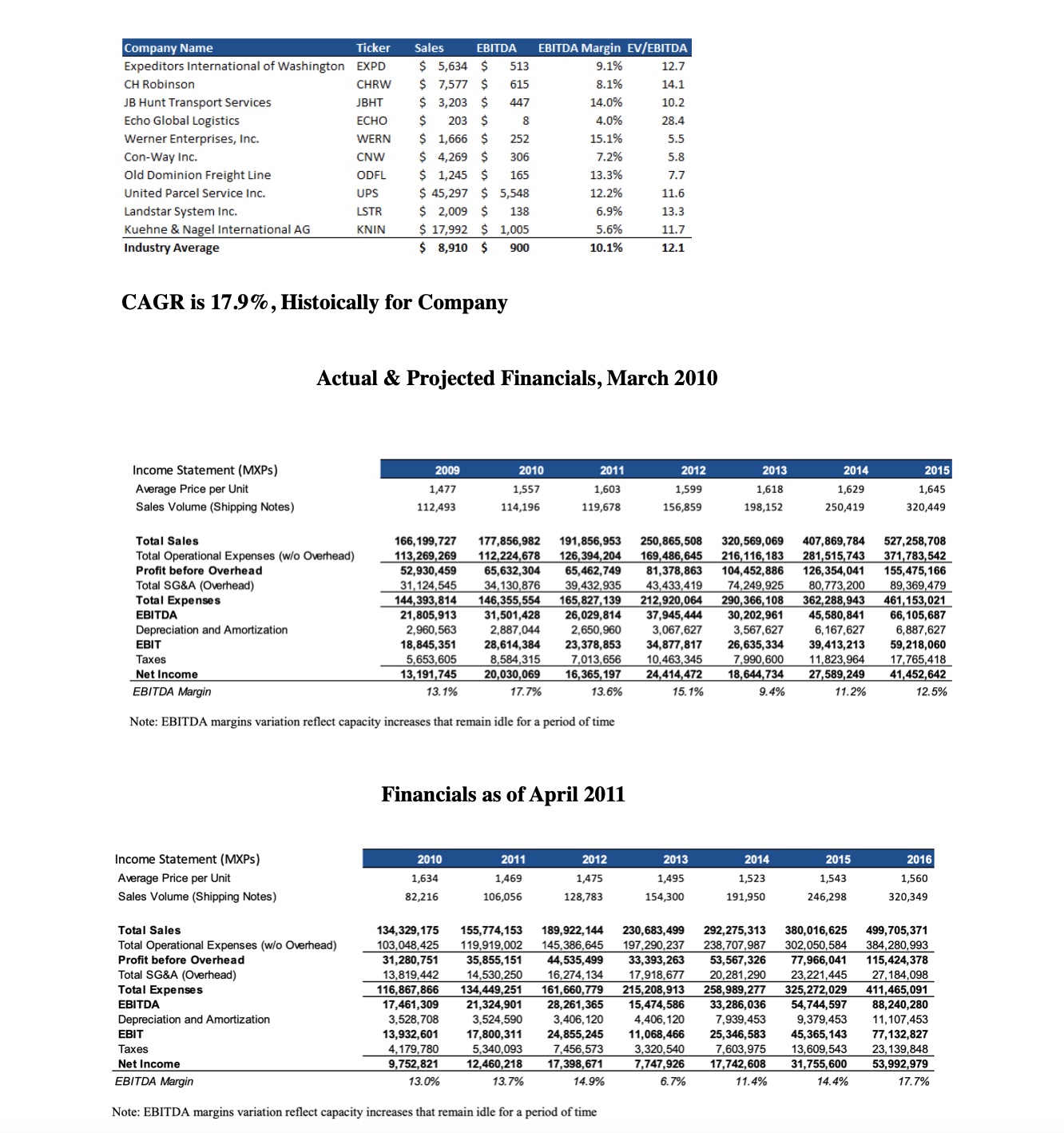

In March 2010 Fernandez and Sicilia signed an LOI with an enterprise valuation of MX $389 million (US $30 million). They valued the company with a number of measures, including comparable logistics industry multiples, next to which the implied purchase multiple of Bomi was an attractive discount. They also used company projections (See Exhibits 5 and 6 for comparable multiples analysis and company financials). Finally, they considered the 35 plus percent internal rate of return (IRR) they hoped to generate for investors over five to seven years and backed into the exit valuation they needed to achieve that return. The LOI valuation was twice the top end of the target deal range of US $5-$15 million that Fernandez and Sicilia had presented, but they were hopeful that their investors would commit more or that they could find additional capital.

Of particular interest were Bomi Mexico's customers, who were primarily multinational pharmaceutical and medical device companies. The customers required highly specialized and customized warehousing and transportation (e.g., for refrigerated or frozen products), and margins on such services were lucrative. Multiyear customer contracts ensured a consistent, recurring revenue stream for the company. Bomi's customer concentration was high, with the top four comprising 61 percent of the company's sales. When Sicilia and Fernandez got word that J&J, Bomi Mexico's largest customer at 26 percent of sales, would not renew its contract, conversation turned back to valuation.

Bomi Group argued that the loss of J&J to Bomi Mexico would reduce EBITDA by 20 percent, but Vestige calculated the impact at 35 percent or more and worried that the company's reputation would be damaged. Fernandez and Sicilia had spent five months in discussions with Estrada and had recently presented their investors with a deal memo, but the deal went short.

Of all the companies Fernandez and Sicilia reassessed in the spring of 2011, Bomi Mexico was at the top of their list. The two had stayed in touch with Estrada and knew how the company was faring. The industry was taking off, and they believed that Bomi Mexico had strong growth prospects. More to the point, they were aware that Estrada remained interested in selling. While Bomi Mexico's EBITDA had in fact fallen 45 percent after the loss of J&J, the company had also signed four new customers that Estrada said would more than compensate for the loss. Estrada provided Vestige with new projections and a new look at historical sales (See Exhibit 8 and 9), but, having seen the result of the J&J departure, Fernandez and Sicilia were skeptical of Bomi's ability to forecast accurately.

Question 1: Present Bomi's new projections to existing and new investors, adjust their partnership relationship and work to close a deal.

Expert Answer:

Cost management a strategic approach

ISBN: 978-0073526942

5th edition

Authors: Edward J. Blocher, David E. Stout, Gary Cokins