Question: In my practice question I found this one: No other information is provided. How can I solve it? 23. Find the value of a three-year

In my practice question I found this one:

No other information is provided. How can I solve it?

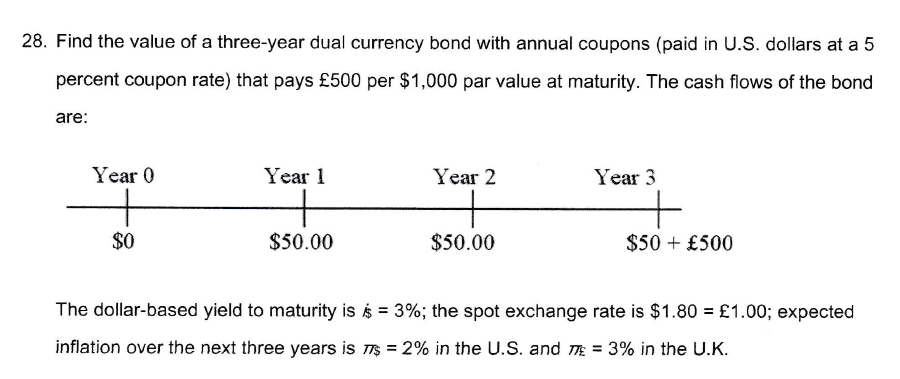

23. Find the value of a three-year dual currency bond with annual coupons (paid in U.S. dollars at a 5 percent coupon rate) that pays 500 per $1,000 par value at maturity. The cash flows of the bond are: Year 0 Year 1 Year 2 Year 3 $0 $50.00 $50.00 $50 + 500 The dollar-based yield to maturity is e = 3%; the spot exchange rate is $1.80 = 1.00; expected inflation over the next three years is m = 2% in the U.S. and m = 3% in the U.K

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock