Question: In the Cutting through the Fog: Finding a future to Fintech case (attached) Carolina Costa is advising a large global bank. Costa is evaluating 4

In the Cutting through the Fog: Finding a future to Fintech case (attached) Carolina Costa is "advising a large global bank". Costa is evaluating 4 possible choices for the bank to address the changing landscape in the industry: do nothing, partner with a fintech company, become a fintech company, and acquire fintech firms. Assume that the "do nothing" and the "become a fintech company" options are not viable. Work with Carolina Costa to:

Devise the pros and cons of the "acquire fintech firms" option.

Make a recommendation to the bank based on your analysis of: (a) the "acquire fintech firms" option, (b) the facts provided by the case, and (c) "partner with a fintech company" option. Would you recommend the bank to acquire or partner with fintech firms? Why?

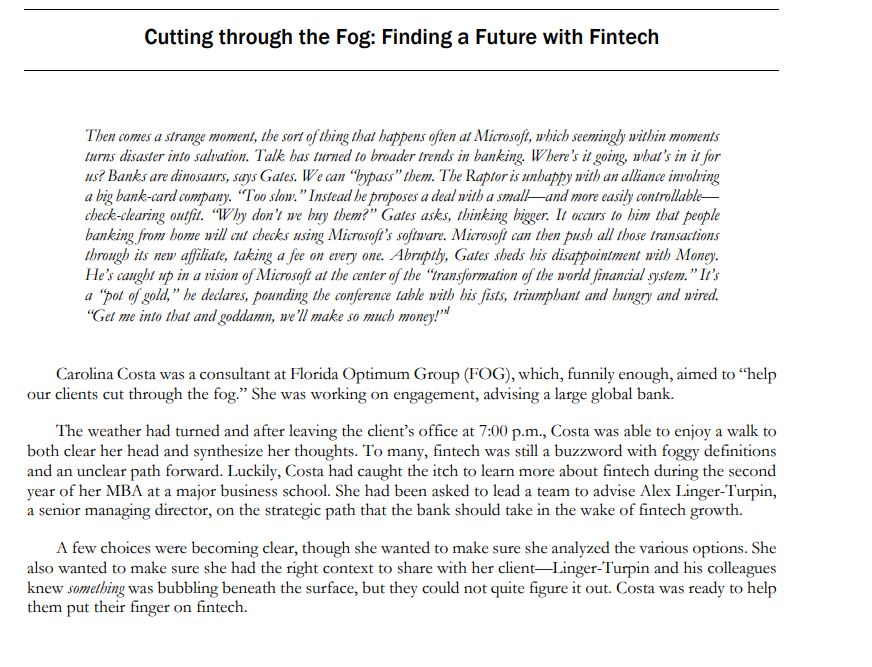

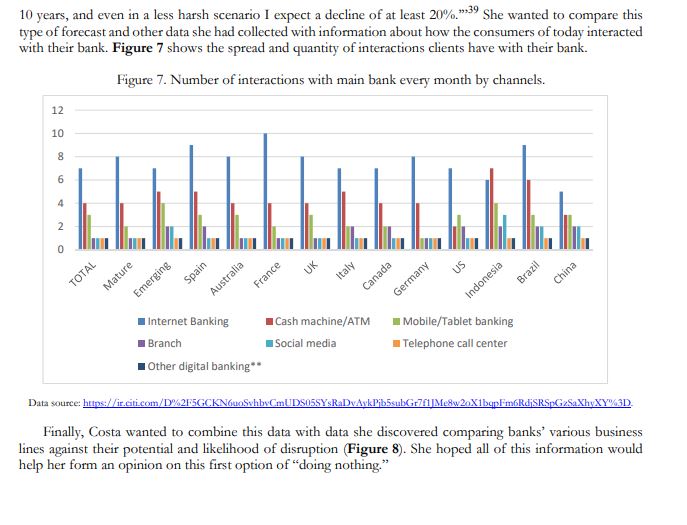

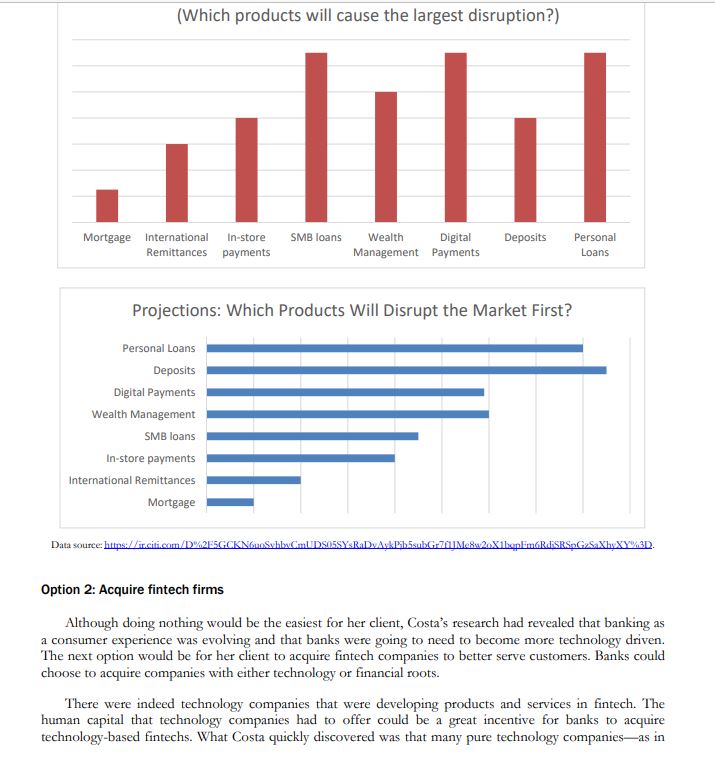

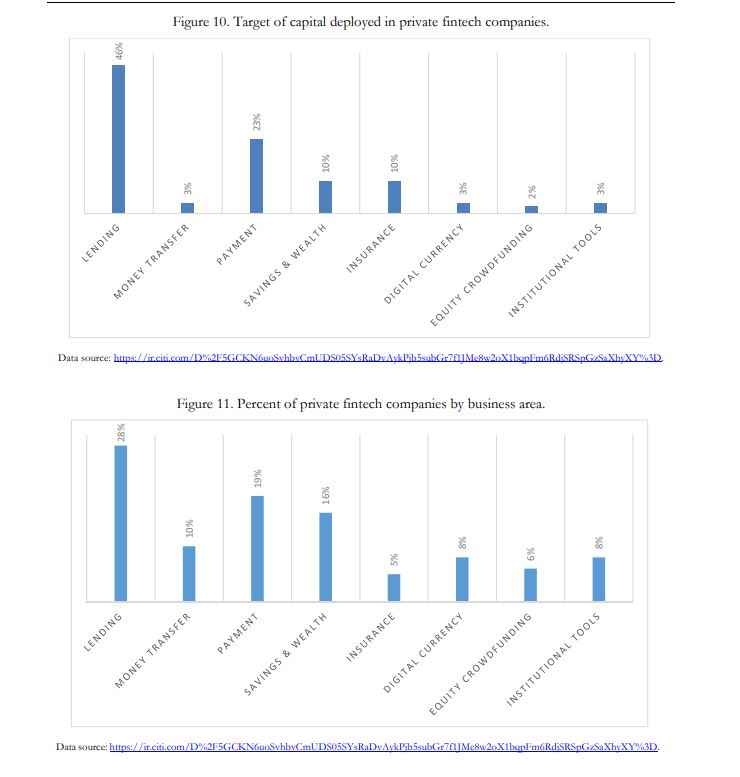

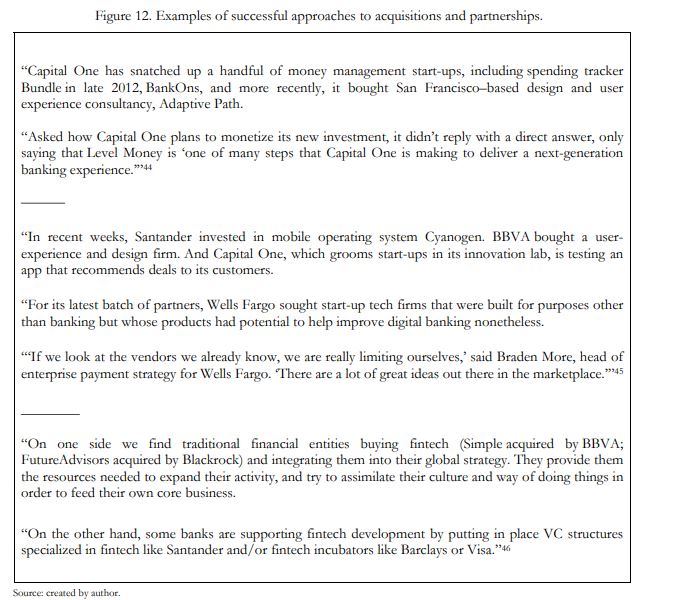

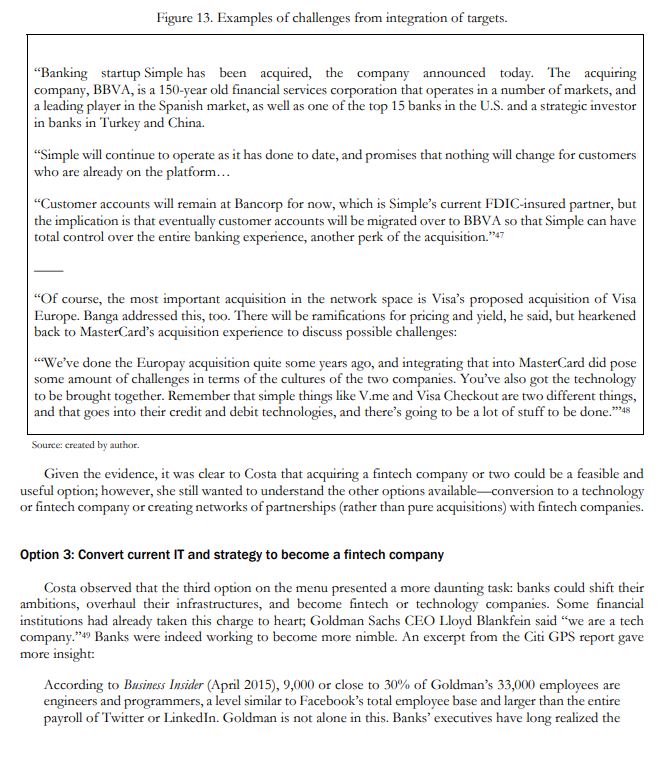

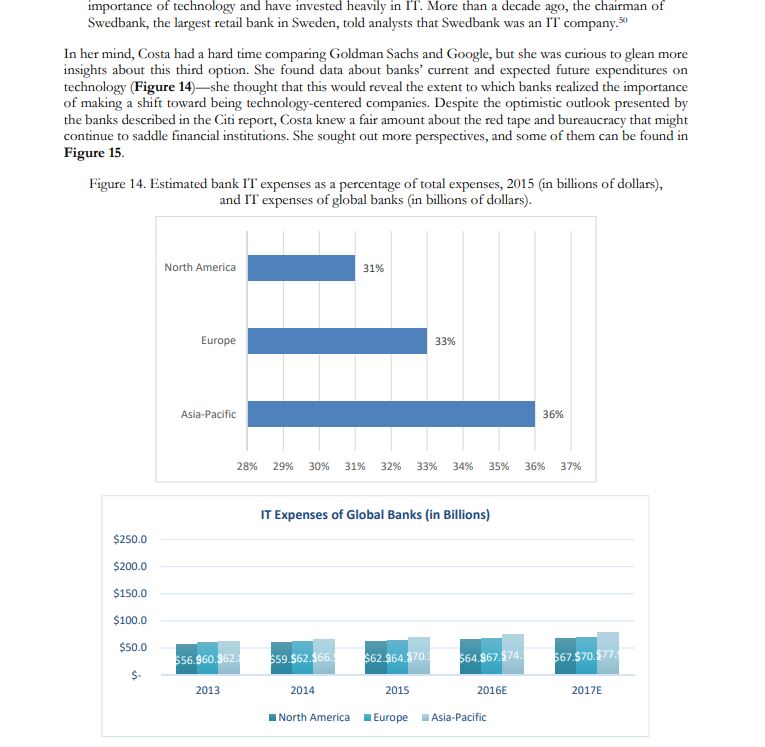

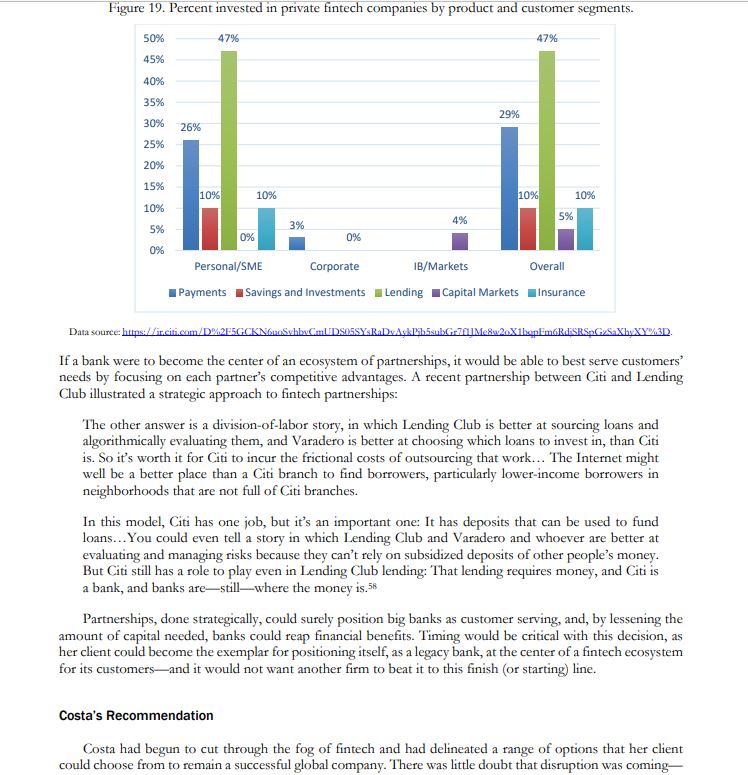

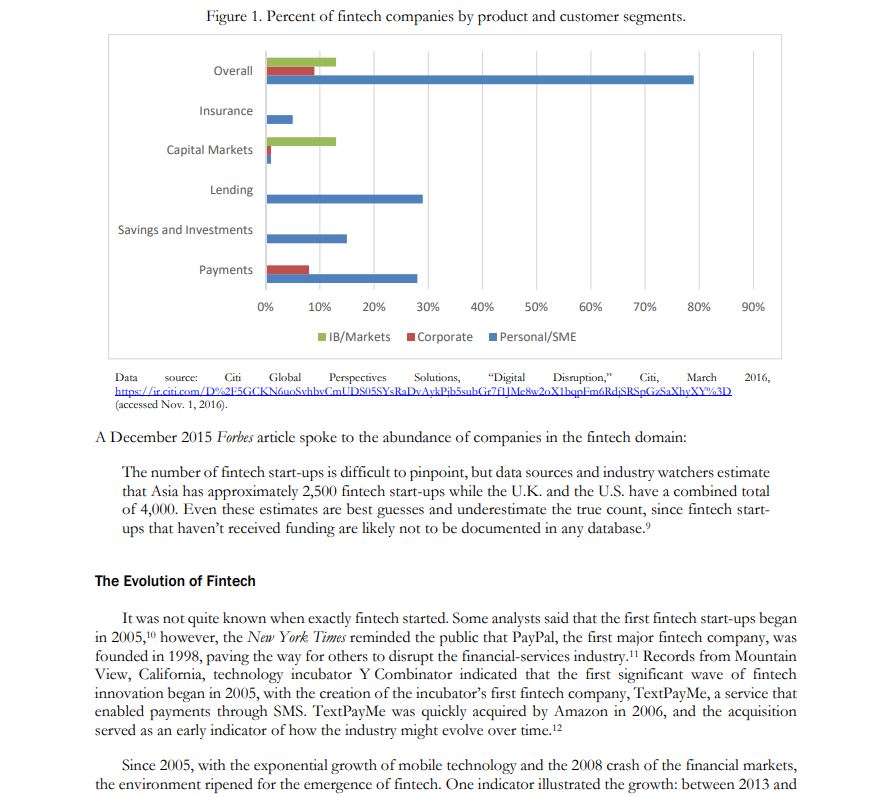

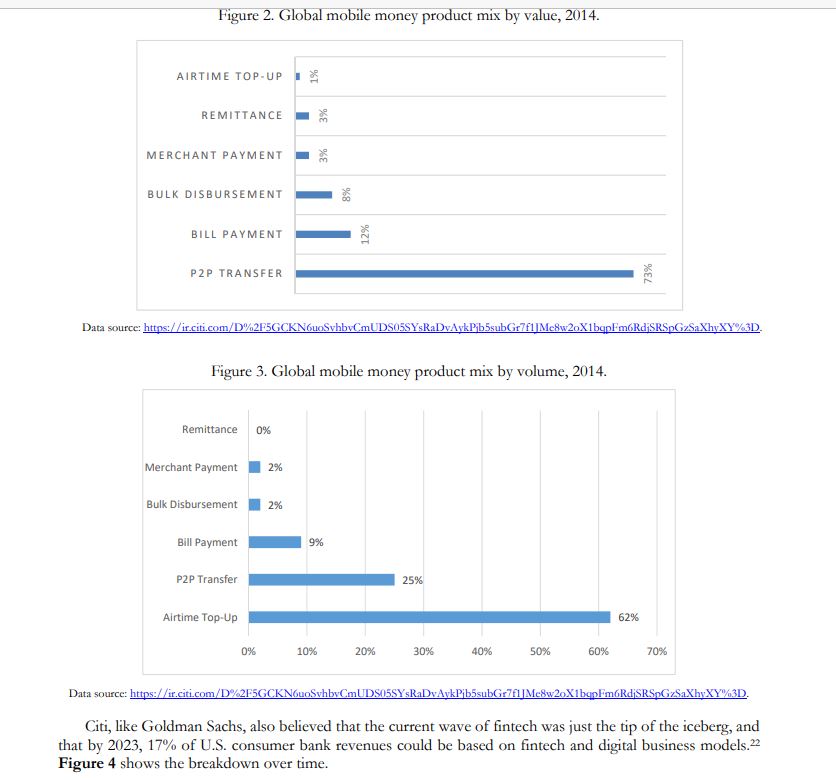

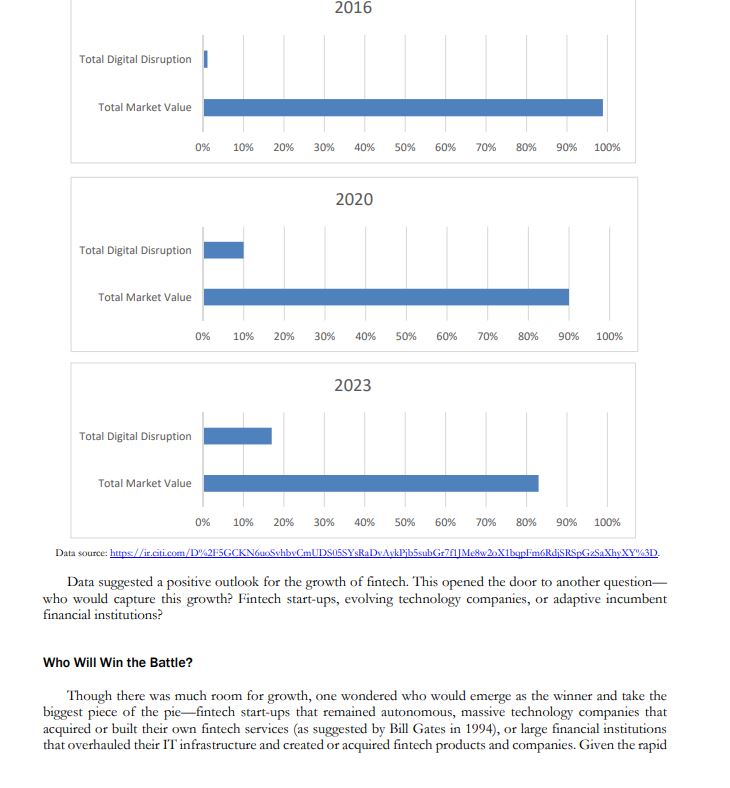

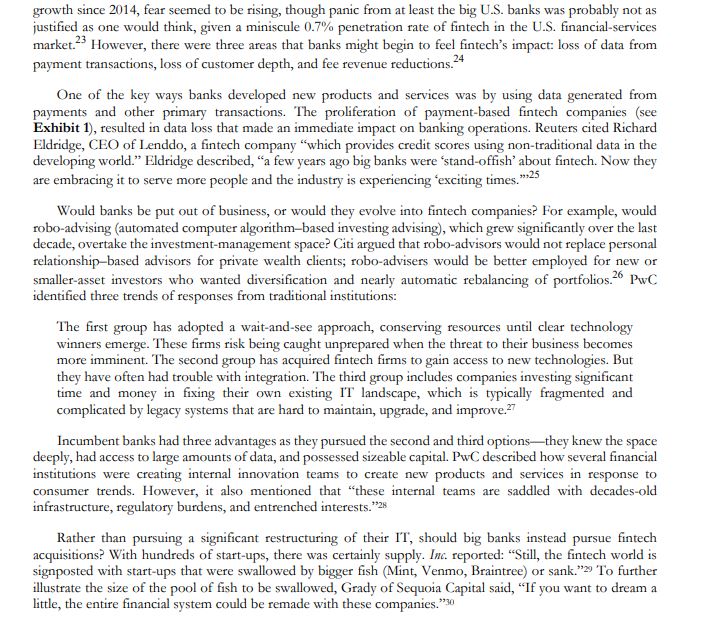

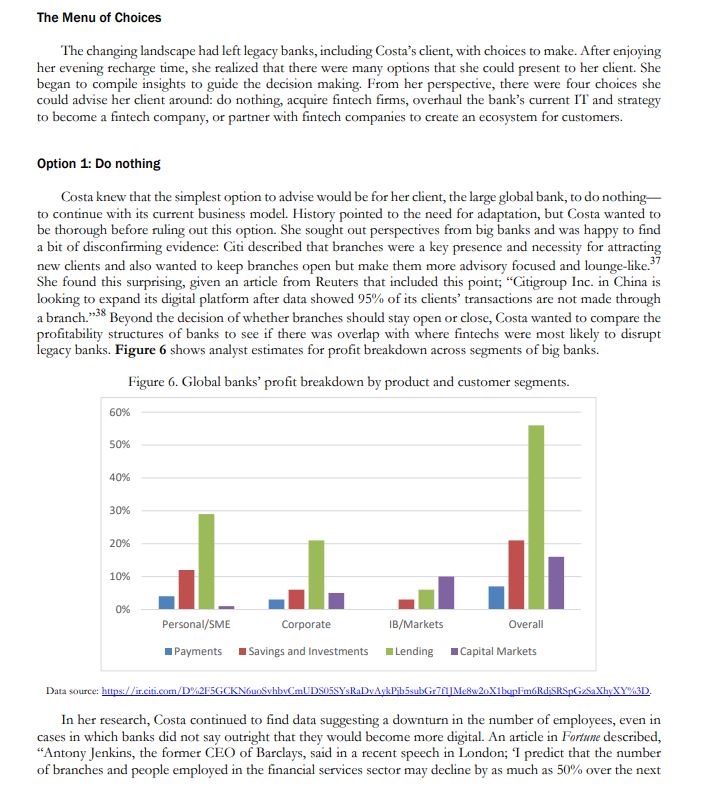

Cutting through the Fog: Finding a Future with Fintech Then comes a strange moment, the sort of thing that happens often at Microsoft, which seemingly within moments turns disaster into salvation. Talk has turned to broader trends in banking. Where's it going, what's in it for us? Banks are dinosaurs, says Gates. We can "bypass" them. The Raptor is unhappy with an alliance involving a big bank-card company. "Too slow. " Instead he proposes a deal with a small-and more easily controllable- check-clearing outfit. "Why don't we buy them?" Gates asks, thinking bigger. It occurs to him that people banking from home will cut checks using Microsoft's software. Microsoft can then push all those transactions through its new affiliate, taking a fee on every one. Abruptly, Gates sheds his disappointment with Money. He's caught up in a vision of Microsoft at the center of the "transformation of the world financial system. " It's a "pot of gold, " be declares, pounding the conference table with his fists, triumphant and hungry and wired. "Get me into that and goddamn, we'll make so much money!" Carolina Costa was a consultant at Florida Optimum Group (FOG), which, funnily enough, aimed to "help our clients cut through the fog." She was working on engagement, advising a large global bank. The weather had turned and after leaving the client's office at 7:00 p.m., Costa was able to enjoy a walk to both clear her head and synthesize her thoughts. To many, fintech was still a buzzword with foggy definitions and an unclear path forward. Luckily, Costa had caught the itch to learn more about fintech during the second year of her MBA at a major business school. She had been asked to lead a team to advise Alex Linger-Turpin, a senior managing director, on the strategic path that the bank should take in the wake of fintech growth. A few choices were becoming clear, though she wanted to make sure she analyzed the various options. She also wanted to make sure she had the right context to share with her client-Linger-Turpin and his colleagues knew something was bubbling beneath the surface, but they could not quite figure it out. Costa was ready to help them put their finger on fintech.10 years, and even in a less harsh scenario I expect a decline of at least 20%." She wanted to compare this type of forecast and other data she had collected with information about how the consumers of today interacted with their bank. Figure 7 shows the spread and quantity of interactions clients have with their bank. Figure 7. Number of interactions with main bank every month by channels. 12 10 8 6 O TOTAL Mature Spain UK Italy US Emerging Australl France Canada Germany China Indonesia Internet Banking Cash machine/ATM I Mobile/Tablet banking Branch Social media Telephone call center Other digital banking* * Data source: https://ir.citi.com/D%2F5GCKNounSchbyCmUD505SYsRaDyArkPib5subGr7/1/Me:w20X1bunFmGRdjSRSpGzSaXhyXYiD Finally, Costa wanted to combine this data with data she discovered comparing banks' various business lines against their potential and likelihood of disruption (Figure 8). She hoped all of this information would help her form an opinion on this first option of "doing nothing."[Which products will cause the largest disruption?)- Mortgage International In-store SMEioans Wealth Digital Deposits Personal Remittances payments Management Payments Loans Projections: Which Products Will Disrupt the Market First? Person a1 Loans Deposits Digital Payments a wealth Management 5MB loans In-store payments International Remittances Mortgage Dela mum: Option 2: Acquire ntech firms Although doing nothing would be the easiest for her client, Costa's research had revealed that banking as a consumer experience was evolving and that banks were going to need to become more technology driven. The next option would be for her client to acquire ntech companies to better serve customers. Banks could choose to acquire companies with ei'ler technology or financial roots. There were indeed technology companies that were developing products and services in ntech_ The human capital that technology companies had to offer could be a great incentive for banks no acquire technologybased fintechs. \\Vr'har Costa quickly discovered was d1at many pure technology companiesas in those that did not set out m be fintechs, but instead set out to serve customers in other wayswere also the largest companies and were likely too big to be bought even by dte world's largest banl-Ls. According to l'wC, ve of the largest tech companies{:mgle, Apple, Iiacebook, Amazon, and Samsunghad all begun making plays in the fintech space.\" Not only could banks not acquire pure technology companies due to costs and regulations, they also needed to watch out, as the big four [{ioogle, Amazon, Apple, and liacebook} could be in banks' blind spot as competitors in the liritech evolution. Bunker: Jamie!" described the context best, saying, \"But it's not just banks that are trying to conquer the fintech space. Amazon is about to cry its hand in this market, as the e-commerte giant's head of payments, Patrick Gauthier, recently announced that the company is considering making some ntech acquisitions as valuations in the space start to decline and lintech becomes a more affordable investment\"" Globally, big technology rms, such as ecommerce giant Alibaba Group (J'tlibaba) in China, were developing d1eir own banklike subsidiaries. {\\lihaba had created Ant Financial Services, which, according to Pedal\46% LEND ING 3% 23% Figure 10. Target of capital deployed in private fintech companies. MONEY TRANSFER PAYMENT 10% 28% SAVINGS & WEALTH 10%% INSURANCE DIGITAL CURRENCY 10% ENDIN ING Data source: hups://it.citi.com/D.2:5GCKNounSchbyCmUDSISSY:RaDyAck LibSaubGr70M.8w2xX1bopEmiGRESRSp25. XIXY3D. 19% Figure 11. Percent of private fintech companies by business area. EQUITY CROWDFUNDING MONEY TRANSFER 16% INSTITUTIONAL TOOLS PAYMENT SAVINGS & WEALTH INSURANCE DIGITAL CURRENCY Data source: https://ir.citi.com/D%21:5GCKNounSchbyCmUDSOSSY's RaDyArkPib5subGr/f1|Me&w20XIbunFmGRd'SRS GzSXhyXYD. EQUITY CROWDFUNDING INSTITUTIONAL TOOLSFigure 12. Examples of successful approaches to acquisitions and partnerships. "Capital One has snatched up a handful of money management start-ups, including spending tracker Bundle in late 2012, BankOns, and more recently, it bought San Francisco-based design and user experience consultancy, Adaptive Path. "Asked how Capital One plans to monetize its new investment, it didn't reply with a direct answer, only saying that Level Money is one of many steps that Capital One is making to deliver a next-generation banking experience."*44 "In recent weeks, Santander invested in mobile operating system Cyanogen. BBVA bought a user- experience and design firm. And Capital One, which grooms start-ups in its innovation lab, is testing an app that recommends deals to its customers. "For its latest batch of partners, Wells Fargo sought start-up tech firms that were built for purposes other than banking but whose products had potential to help improve digital banking nonetheless. "If we look at the vendors we already know, we are really limiting ourselves,' said Braden More, head of enterprise payment strategy for Wells Fargo. 'There are a lot of great ideas out there in the marketplace."145 "On one side we find traditional financial entities buying fintech (Simple acquired by BBVA; FutureAdvisors acquired by Blackrock) and integrating them into their global strategy. They provide them the resources needed to expand their activity, and try to assimilate their culture and way of doing things in order to feed their own core business. "On the other hand, some banks are supporting fintech development by putting in place VC structures specialized in fintech like Santander and/ or fintech incubators like Barclays or Visa."46 Source: created by author.Figure I3. Examples of challenges from integration of targets. \"Banking startup Simple has been acquired, the company announced today. The acquiring company, BBVA, is a lSEl-year old nancial services corporation that operates in a number of markets, and a leading player in the Spanish market, as well as one of the top '1 5 banks in the U5. and a strategic investor in banks in Turkey and China. \"Simple will continue to operate as it has done to date, and promises that nothing will change for customers who are already on the platform. .. \"Customer accounts will remain at Bancorp for now, which is Simple's current l'DlC-insured partner, but the implication is that eventually customer accounts will be migrated over to BBVA so that Simple can have total control over the entire banking experience, another perk of the acquisition?\" \"Of course, the most important acquisition in the network space is V'isa's proposed acquisition of Visa Iiurope. Banga addressed this, too There will be ramications for pricing and yield, he said, but heartened baclt to MasterCard's acquisition experience to discuss possible challenges: \"We've done the liunopay acquisition quite some years ago, and integrating that into MasterCard did pose some amount ofcl'iallenges in terms of the cultures of the two companies. You've also got the technology to be brought together. Remember that simple things like VIIIC and Visa Checkout are two different things, and that goes into their credit and debit technologies, and there's going to be a lot of stuff to be done."""' :i'lul'tui manual by auilmr. (liven the evidence, it was clear to Costa that acquiring a ntech company or two could he a feasible and useful option; however, she still wanted to understand the other options availableconversion to a technology or ntech company or creating networks ot'partnerships [rather than pure acquisitions) with ntech companies. Option 3: Convert current TT and strategy to become a ntech company {'Josta observed that the third option on the menu presented. a more daunting task: banks could shift their ambitions, overhaul their infrastructures, and become ntech or technology companies. Some nancial institutions had already taken this charge to heart, Goldman Sachs CEO Lloyd Blankfein said \"we are a tech company. \"4" Banks were indeed working to become more nimble. An excerpt From the {liti UPS report gave more insight: According to Hashim imiri'cr [Ade 2.015), 9,090 or close to 31]"Ai of Goldman's 33,090 employees are engineers and programmers, a level similar to liacebooli's total employee base and larger than the entire payroll of'l'wit'ter or Linkedln. Goldman is not alone in this. BanILs' executives have long realized [he importance of technology and have invested heavily in IT. More than a decade ago, the chairman of Swedbank, the largest retail bank in Sweden, told analysts that Swedbank was an IT company. In her mind, Costa had a hard time comparing Goldman Sachs and Google, but she was curious to glean more insights about this third option. She found data about banks' current and expected future expenditures on technology (Figure 14)-she thought that this would reveal the extent to which banks realized the importance of making a shift toward being technology-centered companies. Despite the optimistic outlook presented by the banks described in the Citi report, Costa knew a fair amount about the red tape and bureaucracy that might continue to saddle financial institutions. She sought out more perspectives, and some of them can be found in Figure 15. Figure 14. Estimated bank IT expenses as a percentage of total expenses, 2015 (in billions of dollars), and IT expenses of global banks (in billions of dollars). North America 31% Europe 33% Asia-Pacific 36% 28% 29% 30% 31% 32% 33% 34% 3 35% 36% 37% IT Expenses of Global Banks (in Billions) $250.0 $200.0 $150.0 $100.0 $50.0 $56.960.962 $59.562.366. $62 964.$70. 564.867.574 $67 570.577. 2013 2014 2015 2016E 2017E North America Europe Asia-Pacific\f\fFigure 17. Capital deployed in private fintech companies by segment. 80% 70% 60% 50% 40% 30%% 20% 10% 0% Personal & SME Asset Insurance Investment Large Corporate Management & Banking Wealth Figure 18. Percent of private fintech companies by segment. 70% 60% 50% 40% 30% 20% 10% 0% Personal & SME Asset Management Insurance Investment Banking Large Corporate & Wealth Data source: https:/ /ir.citi.com/D%%2F5GCKNGuoSchbyCmUD505SYs RaDyArkPibSsubGr7f1/Me:w20X1bopFmaRdiSRS GzSXhyXY

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!