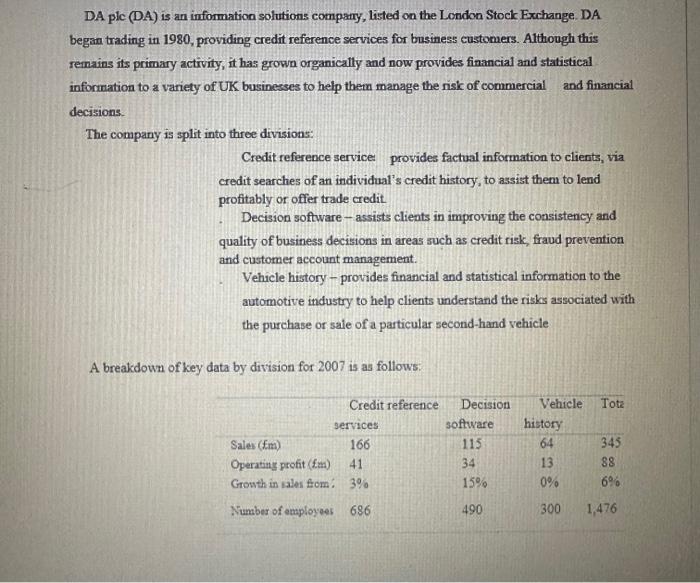

DA plc (DA) is an information solutions company, listed on the London Stock Exchange. DA began...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

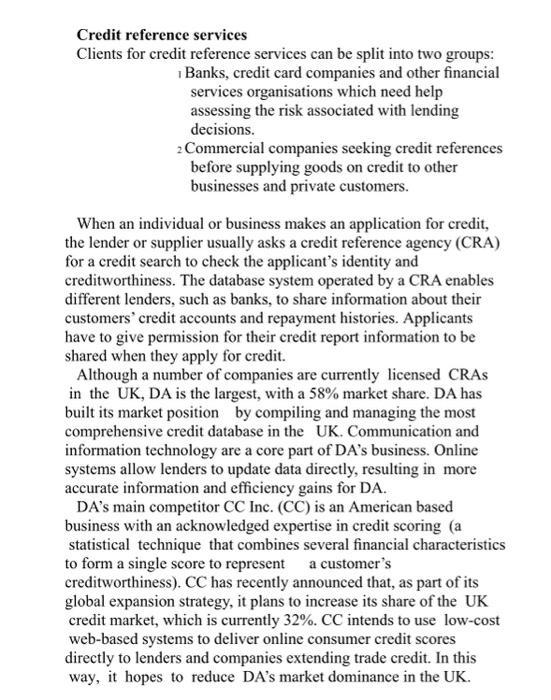

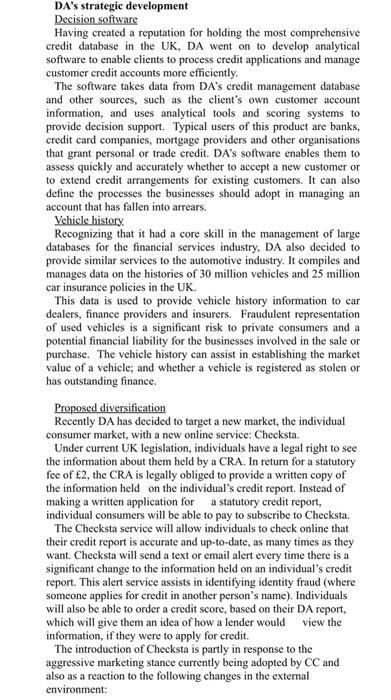

DA plc (DA) is an information solutions company, listed on the London Stock Exchange. DA began trading in 1980, providing credit reference services for business customers. Although this remains its primary activity, it has grown organically and now provides financial and statistical information to a variety of UK businesses to help them manage the risk of commercial and financial decisions. The company is split into three divisions: Credit reference service provides factual information to clients, via credit searches of an individual's credit history, to assist them to lend profitably or offer trade credit. Decision software-assists clients in improving the consistency and quality of business decisions in areas such as credit risk, fraud prevention and customer account management. Vehicle history - provides financial and statistical information to the automotive industry to help clients understand the risks associated with the purchase or sale of a particular second-hand vehicle A breakdown of key data by division for 2007 is as follows: Credit reference Decision Vehicle Tota services software 166 115 34 15% 490 Sales (Em) Operating profit (fm) 41 Growth in sales from: 3% Number of employees 686 history 64 13 0% 300 345 88 6% 1,476 Credit reference services Clients for credit reference services can be split into two groups: Banks, credit card companies and other financial services organisations which need help assessing the risk associated with lending decisions. 2 Commercial companies seeking credit references before supplying goods on credit to other businesses and private customers. When an individual or business makes an application for credit, the lender or supplier usually asks a credit reference agency (CRA) for a credit search to check the applicant's identity and creditworthiness. The database system operated by a CRA enables different lenders, such as banks, to share information about their customers' credit accounts and repayment histories. Applicants have to give permission for their credit report information to be shared when they apply for credit. Although a number of companies are currently licensed CRAS in the UK, DA is the largest, with a 58% market share. DA has built its market position by compiling and managing the most comprehensive credit database in the UK. Communication and information technology are a core part of DA's business. Online systems allow lenders to update data directly, resulting in more accurate information and efficiency gains for DA. DA's main competitor CC Inc. (CC) is an American based business with an acknowledged expertise in credit scoring (a statistical technique that combines several financial characteristics to form a single score to represent a customer's creditworthiness). CC has recently announced that, as part of its global expansion strategy, it plans to increase its share of the UK credit market, which is currently 32%. CC intends to use low-cost web-based systems to deliver online consumer credit scores directly to lenders and companies extending trade credit. In this way, it hopes to reduce DA's market dominance in the UK. DA's strategic development Decision software Having created a reputation for holding the most comprehensive credit database in the UK, DA went on to develop analytical software to enable clients to process credit applications and manage customer credit accounts more efficiently. The software takes data from DA's credit management database and other sources, such as the client's own customer account information, and uses analytical tools and scoring systems to provide decision support. Typical users of this product are banks, credit card companies, mortgage providers and other organisations that grant personal or trade credit. DA's software enables them to assess quickly and accurately whether to accept a new customer or to extend credit arrangements for existing customers. It can also define the processes the businesses should adopt in managing an account that has fallen into arrears. Vehicle history Recognizing that it had a core skill in the management of large databases for the financial services industry, DA also decided to provide similar services to the automotive industry. It compiles and manages data on the histories of 30 million vehicles and 25 million car insurance policies in the UK. This data is used to provide vehicle history information to car dealers, finance providers and insurers. Fraudulent representation of used vehicles is a significant risk to private consumers and a potential financial liability for the businesses involved in the sale or purchase. The vehicle history can assist in establishing the market value of a vehicle; and whether a vehicle is registered as stolen or has outstanding finance. Proposed diversification Recently DA has decided to target a new market, the individual consumer market, with a new online service: Checksta. Under current UK legislation, individuals have a legal right to see the information about them held by a CRA. In return for a statutory fee of £2, the CRA is legally obliged to provide a written copy of the information held on the individual's credit report. Instead of making a written application for a statutory credit report, individual consumers will be able to pay to subscribe to Checksta. The Checksta service will allow individuals to check online that their credit report is accurate and up-to-date, as many times as they want. Checksta will send a text or email alert every time there is a significant change to the information held on an individual's credit report. This alert service assists in identifying identity fraud (where someone applies for credit in another person's name). Individuals will also be able to order a credit score, based on their DA report, which will give them an idea of how a lender would view the information, if they were to apply for credit. The introduction of Checksta is partly in response to the aggressive marketing stance currently being adopted by CC and also as a reaction to the following changes in the external environment: Changing attitudes to money and credit. An increase in spending has led to an increase in demand for credit and it is very easy to apply now, both by telephone and online. This means that individuals are more likely to shop around for credit and lenders have to carry out more checks. Changes in legislation. DA has to conform to the UK laws that govern the way it does business. Government concerns that debt levels are too high have caused a tightening of the legislation to give consumers better access to information held on them, more rights regarding disputes with lenders and more protection from rogue lenders. As a result, CRAs have had to implement a consumer education programme, working closely with consumer organisations to help consumers to understand how credit referencing works. The growth of e-commerce (products bought online). This has necessitated more frequent and rapid credit checks and a subsequent upgrading of DA's information technology systems. An increase in identity fraud. Identity criminals steal people's personal information and use these details to commit crimes, usually obtaining credit illegally. Marketing To date, DA has mainly worked with business clients, attracting business customers through personal selling and retaining them by developing strong client relationships. The sales director is aware that to succeed in the consumer market, DA will need to use a different marketing strategy for Checksta. DA intends to use its knowledge of consumers who have applied for their statutory credit reports in the past, to build up a profile of consumers it wants to target with its online service. Preliminary market research suggests that those most likely are people who are internet users, credit users and those keen to manage their financial affairs effectively. Such people are likely to read the financial pages in newspapers or visit personal finance websites. Required (a) Explain the factors that may have contributed to DA's competitive advantage. (30 marks) (b) Prepare a PESTEL analysis on the credit reference industry, clearly explaining the implications for DA's plans to implement the Checksta product. (30 marks). DA plc (DA) is an information solutions company, listed on the London Stock Exchange. DA began trading in 1980, providing credit reference services for business customers. Although this remains its primary activity, it has grown organically and now provides financial and statistical information to a variety of UK businesses to help them manage the risk of commercial and financial decisions. The company is split into three divisions: Credit reference service provides factual information to clients, via credit searches of an individual's credit history, to assist them to lend profitably or offer trade credit. Decision software-assists clients in improving the consistency and quality of business decisions in areas such as credit risk, fraud prevention and customer account management. Vehicle history - provides financial and statistical information to the automotive industry to help clients understand the risks associated with the purchase or sale of a particular second-hand vehicle A breakdown of key data by division for 2007 is as follows: Credit reference Decision Vehicle Tota services software 166 115 34 15% 490 Sales (Em) Operating profit (fm) 41 Growth in sales from: 3% Number of employees 686 history 64 13 0% 300 345 88 6% 1,476 Credit reference services Clients for credit reference services can be split into two groups: Banks, credit card companies and other financial services organisations which need help assessing the risk associated with lending decisions. 2 Commercial companies seeking credit references before supplying goods on credit to other businesses and private customers. When an individual or business makes an application for credit, the lender or supplier usually asks a credit reference agency (CRA) for a credit search to check the applicant's identity and creditworthiness. The database system operated by a CRA enables different lenders, such as banks, to share information about their customers' credit accounts and repayment histories. Applicants have to give permission for their credit report information to be shared when they apply for credit. Although a number of companies are currently licensed CRAS in the UK, DA is the largest, with a 58% market share. DA has built its market position by compiling and managing the most comprehensive credit database in the UK. Communication and information technology are a core part of DA's business. Online systems allow lenders to update data directly, resulting in more accurate information and efficiency gains for DA. DA's main competitor CC Inc. (CC) is an American based business with an acknowledged expertise in credit scoring (a statistical technique that combines several financial characteristics to form a single score to represent a customer's creditworthiness). CC has recently announced that, as part of its global expansion strategy, it plans to increase its share of the UK credit market, which is currently 32%. CC intends to use low-cost web-based systems to deliver online consumer credit scores directly to lenders and companies extending trade credit. In this way, it hopes to reduce DA's market dominance in the UK. DA's strategic development Decision software Having created a reputation for holding the most comprehensive credit database in the UK, DA went on to develop analytical software to enable clients to process credit applications and manage customer credit accounts more efficiently. The software takes data from DA's credit management database and other sources, such as the client's own customer account information, and uses analytical tools and scoring systems to provide decision support. Typical users of this product are banks, credit card companies, mortgage providers and other organisations that grant personal or trade credit. DA's software enables them to assess quickly and accurately whether to accept a new customer or to extend credit arrangements for existing customers. It can also define the processes the businesses should adopt in managing an account that has fallen into arrears. Vehicle history Recognizing that it had a core skill in the management of large databases for the financial services industry, DA also decided to provide similar services to the automotive industry. It compiles and manages data on the histories of 30 million vehicles and 25 million car insurance policies in the UK. This data is used to provide vehicle history information to car dealers, finance providers and insurers. Fraudulent representation of used vehicles is a significant risk to private consumers and a potential financial liability for the businesses involved in the sale or purchase. The vehicle history can assist in establishing the market value of a vehicle; and whether a vehicle is registered as stolen or has outstanding finance. Proposed diversification Recently DA has decided to target a new market, the individual consumer market, with a new online service: Checksta. Under current UK legislation, individuals have a legal right to see the information about them held by a CRA. In return for a statutory fee of £2, the CRA is legally obliged to provide a written copy of the information held on the individual's credit report. Instead of making a written application for a statutory credit report, individual consumers will be able to pay to subscribe to Checksta. The Checksta service will allow individuals to check online that their credit report is accurate and up-to-date, as many times as they want. Checksta will send a text or email alert every time there is a significant change to the information held on an individual's credit report. This alert service assists in identifying identity fraud (where someone applies for credit in another person's name). Individuals will also be able to order a credit score, based on their DA report, which will give them an idea of how a lender would view the information, if they were to apply for credit. The introduction of Checksta is partly in response to the aggressive marketing stance currently being adopted by CC and also as a reaction to the following changes in the external environment: Changing attitudes to money and credit. An increase in spending has led to an increase in demand for credit and it is very easy to apply now, both by telephone and online. This means that individuals are more likely to shop around for credit and lenders have to carry out more checks. Changes in legislation. DA has to conform to the UK laws that govern the way it does business. Government concerns that debt levels are too high have caused a tightening of the legislation to give consumers better access to information held on them, more rights regarding disputes with lenders and more protection from rogue lenders. As a result, CRAs have had to implement a consumer education programme, working closely with consumer organisations to help consumers to understand how credit referencing works. The growth of e-commerce (products bought online). This has necessitated more frequent and rapid credit checks and a subsequent upgrading of DA's information technology systems. An increase in identity fraud. Identity criminals steal people's personal information and use these details to commit crimes, usually obtaining credit illegally. Marketing To date, DA has mainly worked with business clients, attracting business customers through personal selling and retaining them by developing strong client relationships. The sales director is aware that to succeed in the consumer market, DA will need to use a different marketing strategy for Checksta. DA intends to use its knowledge of consumers who have applied for their statutory credit reports in the past, to build up a profile of consumers it wants to target with its online service. Preliminary market research suggests that those most likely are people who are internet users, credit users and those keen to manage their financial affairs effectively. Such people are likely to read the financial pages in newspapers or visit personal finance websites. Required (a) Explain the factors that may have contributed to DA's competitive advantage. (30 marks) (b) Prepare a PESTEL analysis on the credit reference industry, clearly explaining the implications for DA's plans to implement the Checksta product. (30 marks).

Expert Answer:

Related Book For

Posted Date:

Students also viewed these accounting questions

-

This assignment will focus on some of the stressors encountered by law enforcement officers. You will explore how these stressors affect police officers. Learning about the incidence and prevalence...

-

In this mini-case you will focus on performing one aspect of the test of details on the accounts payable balance ? the search for unrecorded liabilities. To Identify possible unrecorded liabilities...

-

For this discussion report on some of the different methods for raising proceeds through contributed capital, the advantages of doing this, and the disadvantages as well. Which methodology would you...

-

Charlie invested $2,000 at the end of 2015, $2,500 at the end of 2016 and $550 at the end of 2017.She earned 8% on her investment.How much money did she have at the end of 2017?

-

How does a catalyst speed up a reaction? How can a catalyst be involved in a reaction without being consumed by it?

-

A design-to-cost approach to product pricing involves determining the selling price of the product and then figuring out if it can be made at a cost lower than that. Banner Engineering's QT50R...

-

This case deals with several issues regarding contract formation under the UCC. Logan and Kanawha Coal agreed to purchase coal from Detherage via a fax dated March 9, 2010. The fax stated that it had...

-

Nonmonetary Exchanges During the current year, Marshall Construction trades an old crane that has a book value of $90,000 (original cost $140,000 less accumulated depreciation $50,000) for a new...

-

Netflix estimates that North American demand for its streaming service has an elasticity of approximately -1.5. In 2022, 74 million subscribers generated revenues of just over $14 billion at an...

-

Complete Tsate's Form 1040-SR, Schedules A, B and D, Form 8949, Form 6252 and Qualified Dividends and Capital Gain Tax Worksheet. Tsate Kongia (birthdate 02/14/1954) is an unmarried high school...

-

Bond P is a premium bond with a coupon of 8 percent, a YTM of 6 percent, and 15 years to maturity. Bond D is a discount bond with a coupon of 8 percent, a YTM of 10 percent, and also has 15 years to...

-

An individual can build up his or her capital ______. a) by working longer hours only b) by cutting back on consumption only c) by both cutting back on consumption and working longer hours d) by...

-

Where is a price ceiling with respect to equilibrium price? What will be the relative size of quantity demanded and quantity supplied?

-

Which statement is the most accurate? a) Most of the worlds economies are close copies of the American capitalist model. b) The Chinese economy can best be described as democratic socialist. c)...

-

Capital comes from ______. a) gold b) savings c) high consumption d) the government

-

Which statement is the most accurate? a) During the 1980s, people in the Soviet Union and China who worked their own private plots were much more productive than those working on large collective...

-

make scheduling policy for Pediatric Clinic Again, this should be tailored to the specific needs of the fictional facility. Include any instructions for pre-editing, abbreviations, length of...

-

What is an insurable interest? Why is it important?

-

1. Which training methods described earlier in this chapter appear in these scenes? Link the training methods discussed to specific moments and examples in the scenes. 2. Did Brian McCaffrey receive...

-

1. Is Jack Elliot culturally sensitive or culturally insensitive? 2. Does he make any cross-cultural errors on his arrival in Japan? If yes, what are they? 3. Review the earlier chapter section...

-

1. Why was it a good idea for UPS to put its employees in charge of their own safety? 2. Should all companies make employees responsible for their own safety? What drawbacks do you see to such a...

-

Calculate (in terms of a single ket state and no operators) exp{ila a+ B(a+a)]}|a). (8.108)

-

Calculate \(\left\langle x^{2} ightangle_{n}\) and \(\left\langle x^{3} ightangle_{n}\) in the state \(|nangle\) of the harmonic oscillator.

-

Use the Sommerfeld method for a particle in one dimension with a quartic potential, instead of a quadratic one, \(V(x)=\lambda x^{4}\). What is the resulting reduced equation, and can you describe...

Study smarter with the SolutionInn App