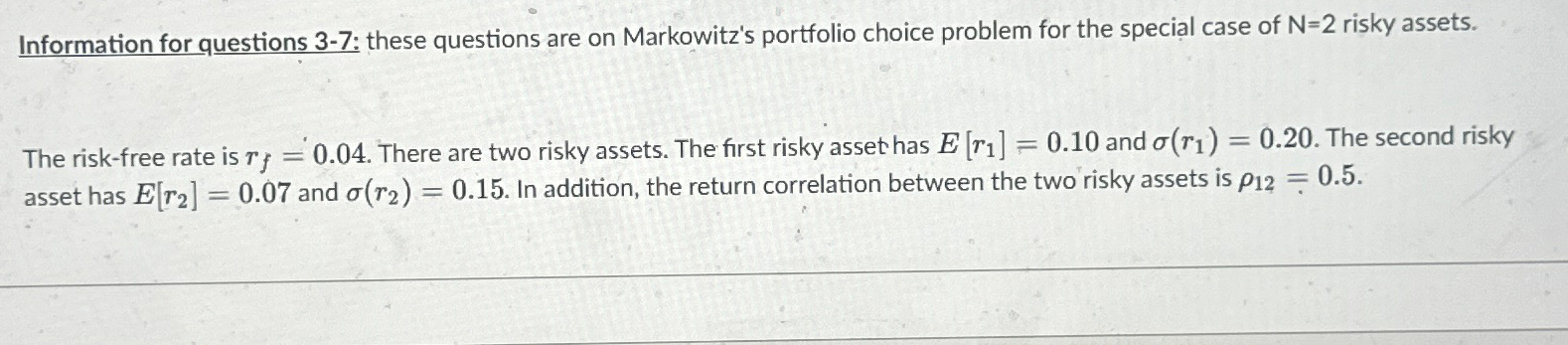

Question: Information for questions 3 - 7 : these questions are on Markowitz's portfolio choice problem for the special case of N = 2 risky assets.

Information for questions : these questions are on Markowitz's portfolio choice problem for the special case of N risky assets.

The riskfree rate is There are two risky assets. The first risky asset has and The second risky asset has and In addition, the return correlation between the two risky assets is

Answer all questions in excel ROUND ALL ANSWERS decimal places

Question what is the weight on the first risky asset round decimal places

Question what is thr weight of the second risky asset in the minimum variance portfoilio

Question what is the volatility

Question what is the weight on the first risky asset in the tangent portfolio

Question what is the maximal sharpe ratio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock