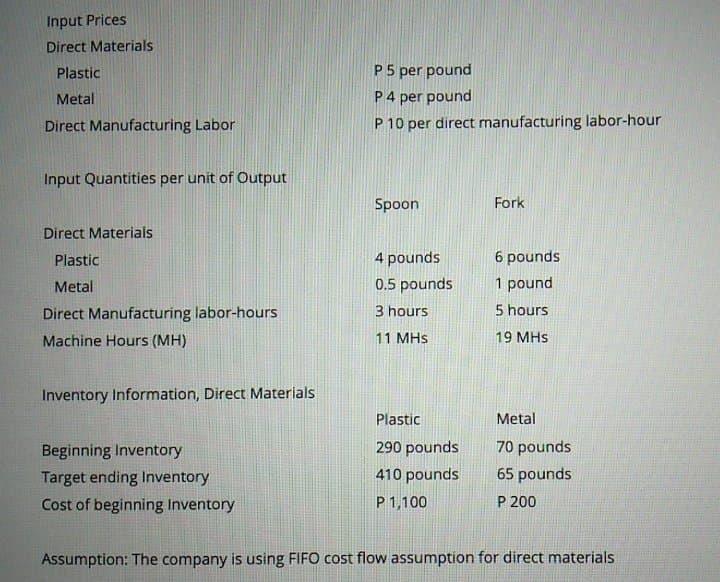

Question: Input Prices Direct Materials Plastic Metal P5 per pound P4 per pound P 10 per direct manufacturing labor-hour Direct Manufacturing Labor Input Quantities per unit

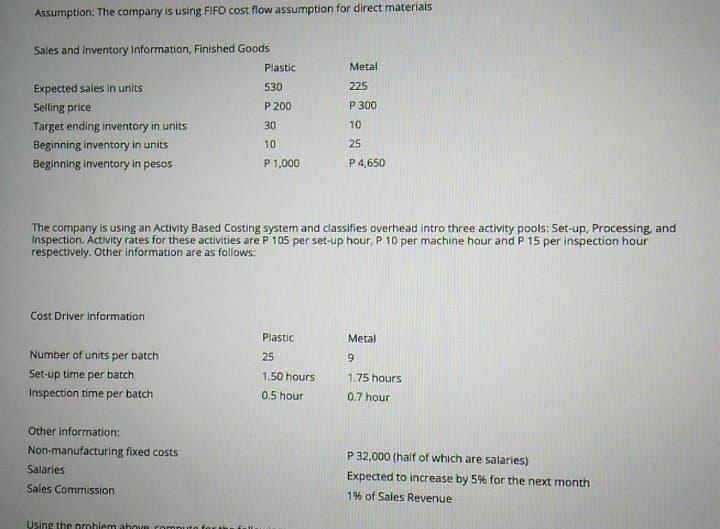

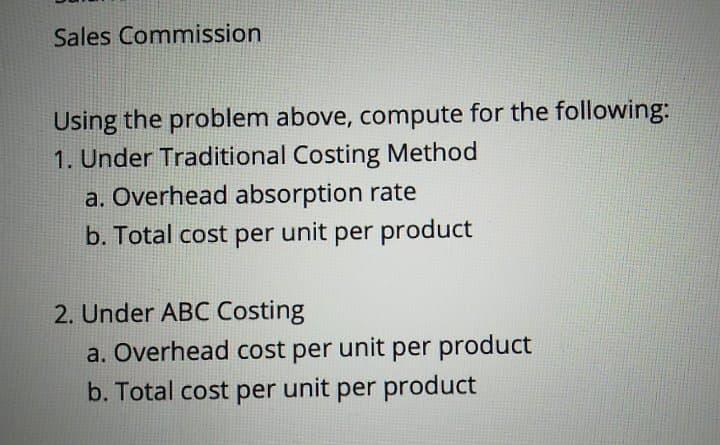

Input Prices Direct Materials Plastic Metal P5 per pound P4 per pound P 10 per direct manufacturing labor-hour Direct Manufacturing Labor Input Quantities per unit of Output Spoon Fork Direct Materials Plastic Metal Direct Manufacturing labor-hours Machine Hours (MH) 4 pounds 0.5 pounds 3 hours 11 MHS 6 pounds 1 pound 5 hours 19 MHs Inventory Information, Direct Materials Beginning Inventory Target ending Inventory Cost of beginning Inventory Plastic 290 pounds 410 pounds P 1,100 Metal 70 pounds 65 pounds P 200 Assumption: The company is using FIFO cost flow assumption for direct materials Assumption: The company is using FIFO cost flow assumption for direct materials Metal 225 Sales and Inventory Information, Finished Goods Plastic Expected sales in units 530 Selling price P200 Target ending inventory in units 30 Beginning inventory in units 10 Beginning inventory in pesos P 1,000 P 300 10 25 P 4,650 The company is using an Activity Based Costing system and classifies overhead into three activity pools: Set-up, Processing and Inspection Activity rates for these activities are P 105 per set-up hour P 10 per machine hour and P 15 per inspection hour respectively. Other information are as follows: Cost Driver Information Plastic Metal 9 25 Number of units per batch Set-up time per batch Inspection time per batch 1.50 hours 1.75 hours 0.5 hour 0.7 hour Other information: Non-manufacturing fixed costs Salaries P 32,000 (half of which are salaries) Expected to increase by 5% for the next month 1% of Sales Revenue Sales Commission Using the problem abn romuito forth Sales Commission Using the problem above, compute for the following: 1. Under Traditional Costing Method a. Overhead absorption rate b. Total cost per unit per product 2. Under ABC Costing a. Overhead cost per unit per product b. Total cost per unit per product Input Prices Direct Materials Plastic Metal P5 per pound P4 per pound P 10 per direct manufacturing labor-hour Direct Manufacturing Labor Input Quantities per unit of Output Spoon Fork Direct Materials Plastic Metal Direct Manufacturing labor-hours Machine Hours (MH) 4 pounds 0.5 pounds 3 hours 11 MHS 6 pounds 1 pound 5 hours 19 MHs Inventory Information, Direct Materials Beginning Inventory Target ending Inventory Cost of beginning Inventory Plastic 290 pounds 410 pounds P 1,100 Metal 70 pounds 65 pounds P 200 Assumption: The company is using FIFO cost flow assumption for direct materials Assumption: The company is using FIFO cost flow assumption for direct materials Metal 225 Sales and Inventory Information, Finished Goods Plastic Expected sales in units 530 Selling price P200 Target ending inventory in units 30 Beginning inventory in units 10 Beginning inventory in pesos P 1,000 P 300 10 25 P 4,650 The company is using an Activity Based Costing system and classifies overhead into three activity pools: Set-up, Processing and Inspection Activity rates for these activities are P 105 per set-up hour P 10 per machine hour and P 15 per inspection hour respectively. Other information are as follows: Cost Driver Information Plastic Metal 9 25 Number of units per batch Set-up time per batch Inspection time per batch 1.50 hours 1.75 hours 0.5 hour 0.7 hour Other information: Non-manufacturing fixed costs Salaries P 32,000 (half of which are salaries) Expected to increase by 5% for the next month 1% of Sales Revenue Sales Commission Using the problem abn romuito forth Sales Commission Using the problem above, compute for the following: 1. Under Traditional Costing Method a. Overhead absorption rate b. Total cost per unit per product 2. Under ABC Costing a. Overhead cost per unit per product b. Total cost per unit per product

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts