Question: Instructions for Questions 13-19 Create a dataset that has monthly returns for the following stocks: TSLA, JNJ, GOOGL, and GE from January 1, 2018 to

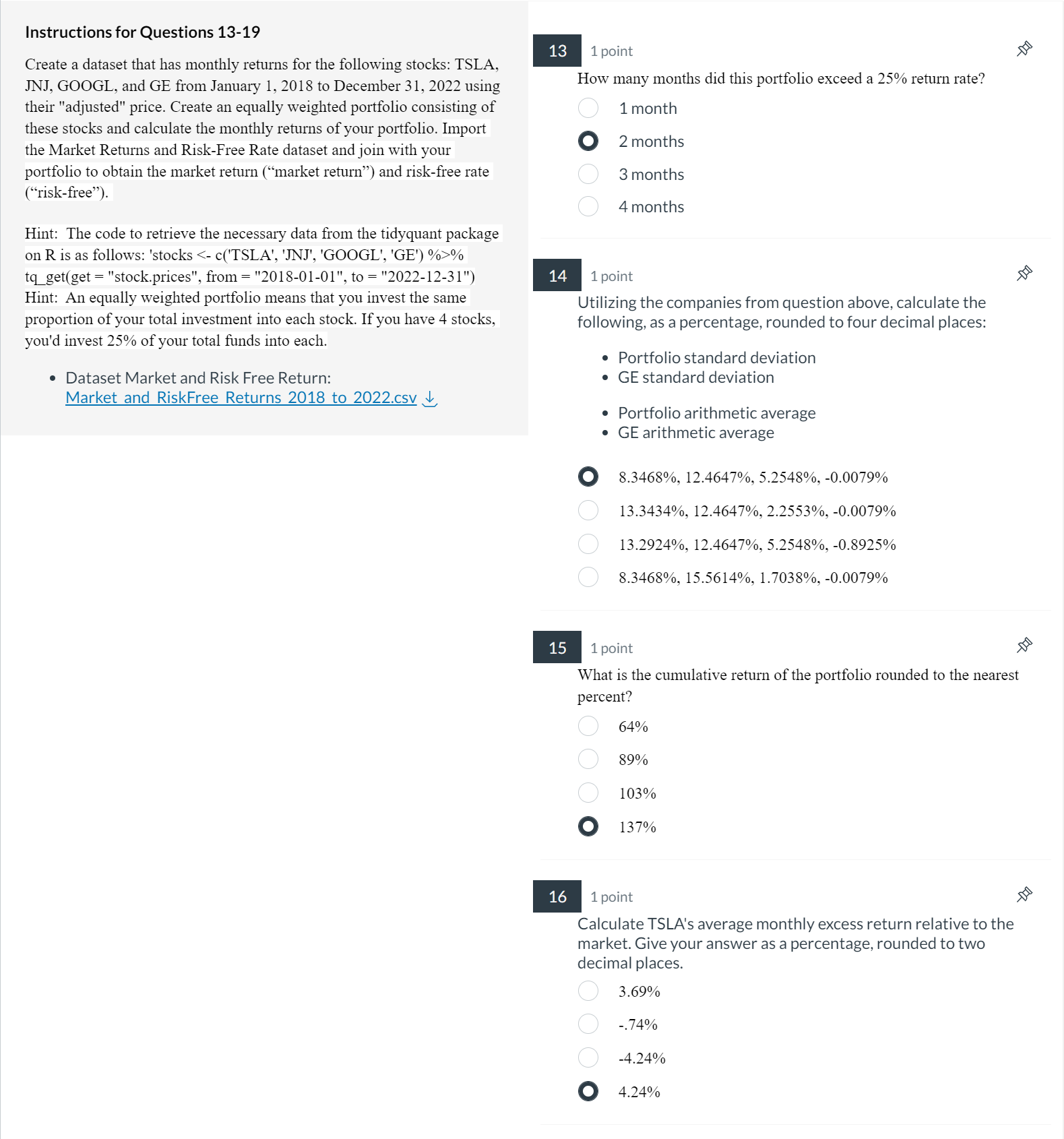

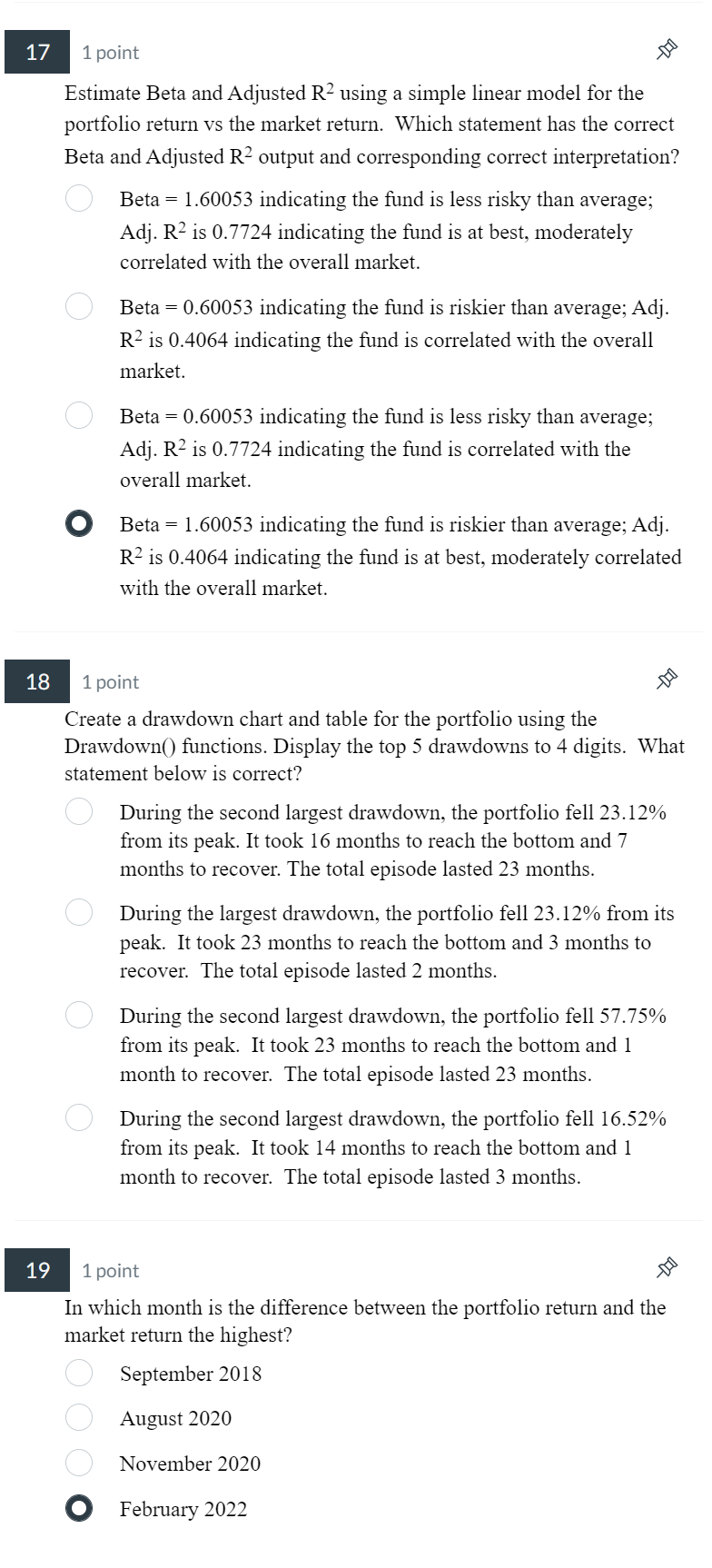

Instructions for Questions 13-19 Create a dataset that has monthly returns for the following stocks: TSLA, JNJ, GOOGL, and GE from January 1, 2018 to December 31, 2022 using their "adjusted" price. Create an equally weighted portfolio consisting of these stocks and calculate the monthly returns of your portfolio. Import the Market Returns and Risk-Free Rate dataset and join with your portfolio to obtain the market return (\"market return\") and risk-free rate (\"risk-free\"). Hint: The code to retrieve the necessary data from the tidyquant package on R is as follows: 'stocks % tq get(get = "stock.prices", from = "2018-01-01", to = "2022-12-31") Hint: An equally weighted portfolio means that you invest the same proportion of your total investment into each stock. If you have 4 stocks, you'd invest 25% of your total funds into each. e Dataset Market and Risk Free Return: Market and RiskFree Returns 2018 to 2022.csv ~r 1 point How many months did this portfolio exceed a 25% return rate? 1 month o 2 months 3 months 4 months 1 point Utilizing the companies from question above, calculate the following, as a percentage, rounded to four decimal places: * Portfolio standard deviation GE standard deviation * Portfolio arithmetic average GE arithmetic average 8.3468%, 12.4647%, 5.2548%, -0.0079% 13.3434%, 12.4647%, 2.2553%, -0.0079% 13.2924%, 12.4647%, 5.2548%, -0.8925% 8.3468%, 15.5614%, 1.7038%, -0.0079% 1 point % $ brg What is the cumulative return of the portfolio rounded to the nearest percent? 64% 89% 103% 137% o 1 point Calculate TSLA's average monthly excess return relative to the market. Give your answer as a percentage, rounded to two decimal places. 3.69% -74% -4.24% 4.24% 5 1 point }9' Estimate Beta and Adjusted RZ using a simple linear model for the portfolio return vs the market return. Which statement has the correct Beta and Adjusted R2 output and corresponding correct interpretation? Beta = 1.60053 indicating the fund is less risky than average; Adj. R?is 0.7724 indicating the fund is at best, moderately correlated with the overall market. Beta = 0.60053 indicating the fund is riskier than average; Adj. R?is 0.4064 indicating the fund is correlated with the overall market. Beta = 0.60053 indicating the fund 1s less risky than average; Adj. R?is 0.7724 indicating the fund is correlated with the overall market. o Beta = 1.60053 indicating the fund is riskier than average; Adj. R2 is 0.4064 indicating the fund is at best, moderately correlated with the overall market. 1 point 5' Create a drawdown chart and table for the portfolio using the Drawdown() functions. Display the top 5 drawdowns to 4 digits. What statement below is correct? During the second largest drawdown, the portfolio fell 23.12% from its peak. It took 16 months to reach the bottom and 7 months to recover. The total episode lasted 23 months. During the largest drawdown, the portfolio fell 23.12% from its peak. It took 23 months to reach the bottom and 3 months to recover. The total episode lasted 2 months. During the second largest drawdown, the portfolio fell 57.75% from its peak. It took 23 months to reach the bottom and 1 month to recover. The total episode lasted 23 months. During the second largest drawdown, the portfolio fell 16.52% from its peak. It took 14 months to reach the bottom and 1 month to recover. The total episode lasted 3 months. 1 point 5 In which month is the difference between the portfolio return and the market return the highest? September 2018 August 2020 November 2020 o February 2022

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!