Question: INSTRUCTIONS You can use any of the references from weeks 1-7 in our classroom including discussion postings and the links to the COSO internal control

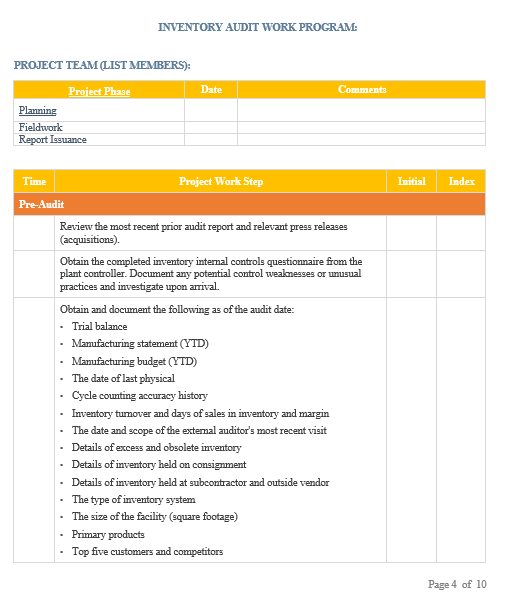

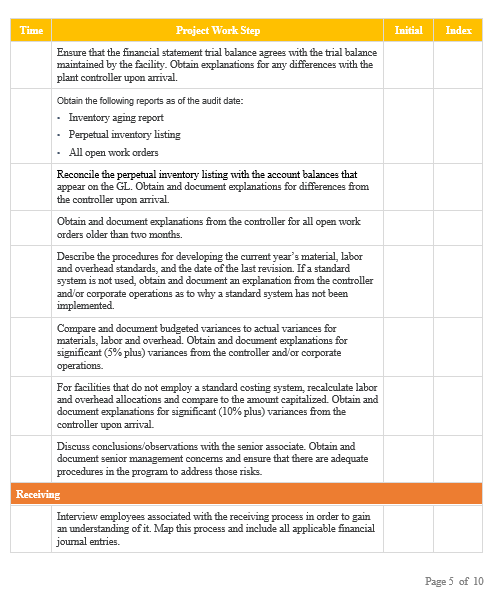

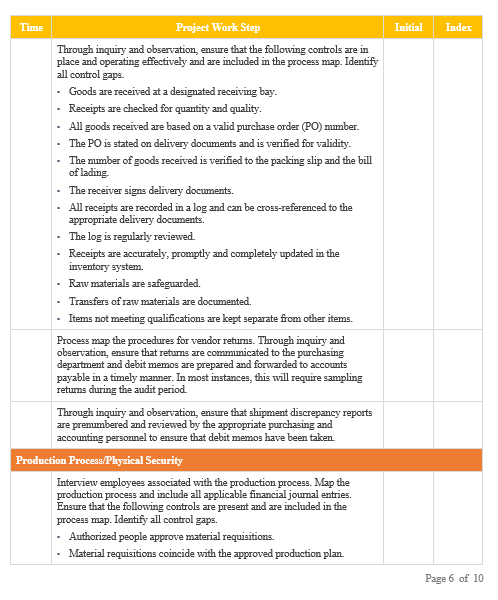

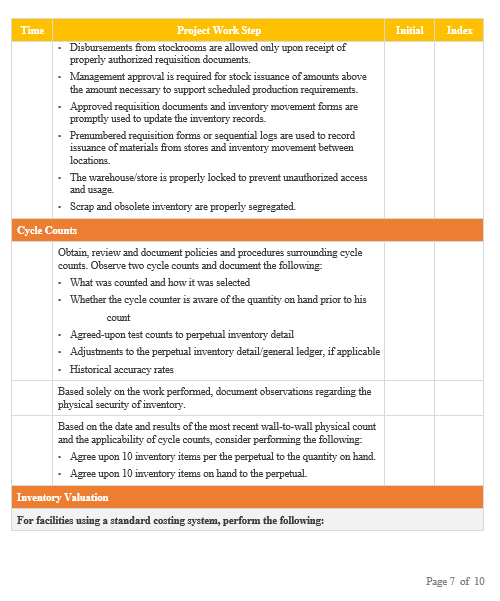

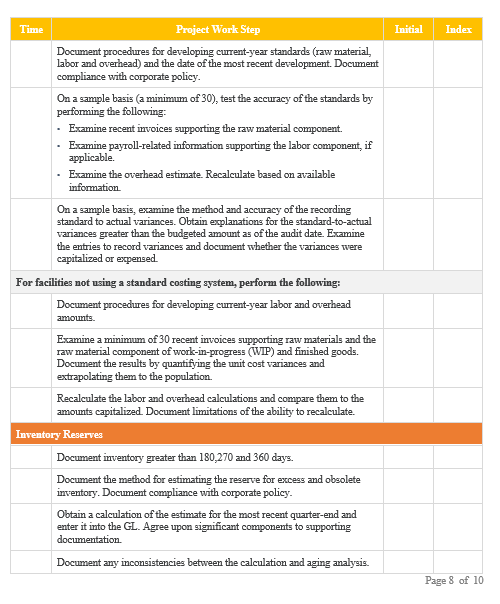

INSTRUCTIONS You can use any of the references from weeks 1-7 in our classroom including discussion postings and the links to the COSO internal control and ERM materials. The responses must be in your own words. I do not expect citations. You are not allowed to use other sources or discuss the exam with other students. You must submit your responses in a Word document. Questions 1-4 are worth 20 points each. The other two questions are worth 10 points each. 1) Internal auditing is going to be performing an assurance engagement dealing with controls over production and inventory. Some of the items to be covered in the engagement include: Determine if there is an issue with excess, obsolete or unsaleable inventory. Determine if there are inventory shortfalls ve. what is shown in the general ledger. Determine if there are issues with late shipments or errors in what material is being shipped to customers. Determine if there are material issues with the quality of the company's finished products. For each item, select the two best tests in the reading Audit Test Type Guide which in your judgment are the most appropriate to gather the required evidence. Briefly explain why you selected each test. Briefly describe what evidence you are trying to obtain from each test. For your response, you can create a chart. 1) Go to the inventory audit program at the bottom of this document. Identify three steps in the audit program where audit software can be used to perform testing Explain how the audit software can be used to perform these steps (ie, the basic logic each query or program would use). Here is a helpful hint on how to go about responding to this question. I am going to use accounts parable as an example. Let's say the audit step is to test for payments to unauthorized suppliers. One approach is to match the vendor master file to the popment history file using vendor number as the common piece of data in the two files. List any records in the payment history file without a corresponding match in the vendor master file. 3) A staff internal auditor was assigned to audit one of the company's wholesale distribution locations. The staff auditor returned to the office after a week and said that every thing was fine. The senior auditor reviewed the staff auditor's working papers and noted that there was a year-end adjustment in excess of US $100,000-a debit to sales and a credit to accounts receivable. "To adjust the general ledger accounts receivable account to the accounts receivable subsidiary ledger" is how the description read. The senior asked the staff auditor how an error that big could have happened. He told her the location manager said there had been some problems installing the accounting system at the new store. Initially, the senior auditor thought the adjustment was proper since the general ledger balance was now in agreement with the subsidiary ledger. However, a short time later she was reviewing the analytical procedures performed by the staff auditor and noted that the gross margin percentage at that location was significantly lower than the gross margin at the other Page 1 of 10locations. The staff auditor's working papers included the following explanation: "Per the store manager, prices were reduced at the Wichita store to attract customers in a new location." The next day, the senior auditor was talking to the company controller. "I guess those price reductions earlier in the year really worked to attract new customers," she said. "Price reductions?" said the controller. "What price reductions?" The company is a wholesale distributor-it does not have sales like one might find in a retail store. The senior auditor questioned the controller about the problems the company had encountered installing the accounts receivable system. The controller said that the staff auditor must have misunderstood because no problems had ever been reported Accordingly, the auditors expanded their fieldwork, tracing customer payments back and forth between the subsidiary ledger and the general ledger. Their expanded work uncovered the fact that the location manager was stealing payments customers made on account. That is why the subsidiary ledger was out of balance with the general ledger. To cover up his theft, the manager debited the sales account, which was why the gross margins of the two stores were not aligned. The staff auditor originally failed to give due consideration to the apparent warning signs of fraud. What are some of the more likely reasons why he either missed the red flags or failed to pursue them? 4) A summary of an internal audit engagement performed at the request of executive management is presented below. The claims department of XYZ Insurance Company has instituted new claims procedures for local offices. The new procedures were designed to improve the review of claims and to prevent both overpayment and payment of false claims. Management mentioned concern about the new procedures at the opening conference of the audit engagement. Management told the internal auditors that 20 complaints had been received recently about the excessive time it took to receive the mourance proceeds for their claims. The company advertises 48-hour claim service. Each of the 20 claims that generated the complaints took seven days. Management said these were the first complaints of this type and were received only after the new procedures were implemented. Management feared that if the claims took too long to process, many clients would switch to another company. The internal auditors decided to find out if processing time had really increased, and if so, whether this was because of the new procedures. The internal auditors decided to test 25 randomly selected claims made since the change in the procedures and 25 claims from before the procedures and compare them. The tests revealed that the new process had caused an increase in the processing time for two reasons. First, there was a learning effect with the new required forms The headquarters claims department often had to correct the forms and request additional information before claims could be processed. Second, the new process required a more extensive review than before, sometimes even including a field visit by one of the claims staff in addition to the regular inquiry by one of the company's claims adjusters. The internal auditors estimated that the delayed disposition of the claims seriously eroded the marketability of the company's insurance policies, perhaps decreasing sales by as much as 10 percent the first year and up to 25 percent in subsequent years. The new procedure also increased the cost of servicing claims by 5 percent to 10 percent, depending on whether an additional inquiry is conducted by one of the claims department staff members. The estimated savings on payment of improper claims was equivalent to a maximum of 10 percent of total expenditures in any one year. Page 2 of 10There were significant differences of opinion within the audit team as to the appropriate course of action. After much debate within the audit team, the final audit report recommended returning to the previous claims service procedures, with minor modifications, to avoid the problems associated with the revised procedures. The additional review procedure recommended in the report was a computer scan of company records to ascertain any previous claims by the 20 claimants and the nature as well as the number of prior claims. Required: A) Describe some alternative internal audit procedures the audit team might have chosen to those procedures the team performed. Do you consider your procedures to be superior to the ones chosen? If so, why? B) Write an alternative internal audit recommendation to the one in the final audit report. You should include two specific actions in your recommendation. 5) Explain whether you agree or disagree with the following statement: For every control selected for testing, the internal auditor requires the same quality (relevance and reliability) and quantity (sufficiency) of audit evidence. A yes or no answer is not sufficient. I need to know why. You must provide an example in your response. 6) The Foundation for Critical Thinking states that all subjects have a fundamental thought process. To understand the thought process, they recommend raising some questions. Please respond in your own words to the four questions below using what you have learned in this course. a) What viewpoint is fostered in this field (i.e., how do internal auditors tend to view the world)? b) What kinds of problems do they try to solve? c) How do they go about gathering information? d) What types of judgments and assumptions do internal auditors make? Page 3 of 10INVENTORY AUDIT WORK PROGRAM: PROJECT TEAM (LIST MEMBERS): Project Phase Date Comments Planning Fieldwork Report Issuance Time Project Work Step Initial Index Pre-Audit Review the most recent prior audit report and relevant press releases (acquisitions). Obtain the completed inventory internal controls questionnaire from the plant controller. Document any potential control weaknesses or unusual practices and investigate upon arrival Obtain and document the following as of the audit date: Trial balance Manufacturing statement (YTD) Manufacturing budget (YTD) The date of last physical Cycle counting accuracy history Inventory turnover and days of sales in inventory and margin The date and scope of the external auditor's most recent visit Details of excess and obsolete inventory Details of inventory held on consignment Details of inventory held at subcontractor and outside vendor The type of inventory system The size of the facility (square footage) Primary products Top five customers and competitors Page 4 of 10Time Project Work Step Initial Index Engure that the financial statement trial balance agrees with the trial balance maintained by the facility. Obtain explanations for any differences with the plant controller upon arrival. Obtain the following reports as of the audit date: Inventory aging report Perpetual inventory listing . All open work orders Reconcile the perpetual inventory listing with the account balances that appear on the GL. Obtain and document explanations for differences from the controller upon arrival. Obtain and document explanations from the controller for all open work orders older than two months. Describe the procedures for developing the current year's material, labor and overhead standards, and the date of the last revision. If a standard system is not used, obtain and document an explanation from the controller and or corporate operations as to why a standard system has not been implemented Compare and document budgeted variances to actual variances for materials, labor and overhead. Obtain and document explanations for significant (3% plus) variances from the controller and or corporate operations. For facilities that do not employ a standard costing system, recalculate labor and overhead allocations and compare to the amount capitalized. Obtain and document explanations for significant (10% plus) variances from the controller upon arrival. Discuss conclusions/observations with the senior associate. Obtain and document senior management concerns and ensure that there are adequate procedures in the program to address those risks. Receiving Interview employees associated with the recerving process in order to gain an understanding of it. Map this process and include all applicable financial journal entries. Page 5 of 10Time Project Work Step Initial Index Through inquiry and observation, ensure that the following controls are in place and operating effectively and are included in the process map. Identify all control gaps. Goods are received at a designated receiving bay. Receipts are checked for quantity and quality. All goods received are based on a valid purchase order (PO) number. The PO is stated on delivery documents and is verified for validity. The number of goods received is verified to the packing slip and the bill of lading- The receiver signs delivery documents. All receipts are recorded in a log and can be cross-referenced to the appropriate delivery documents. The log is regularly reviewed Receipts are accurately, promptly and completely updated in the inventory system. Raw materials are safeguarded. Transfers of raw materials are documented. Items not meeting qualifications are kept separate from other items. Process map the procedures for vendor returns. Through inquiry and observation, ensure that returns are communicated to the purchasing department and debit memos are prepared and forwarded to accounts payable in a timely manner. In most instances, this will require sampling returns during the audit period Through inquiry and observation, ensure that shipment discrepancy reports are prenumbered and reviewed by the appropriate purchasing and accounting personnel to ensure that debit memos have been taken Production Process Physical Security Interview employees associated with the production process. Map the production process and include all applicable financial journal entries. Ensure that the following controls are present and are included in the process map. Identify all control gaps. Authorized people approve material requisitions. Material requisitions coincide with the approved production plan. Page 6 of 10Time Project Work Step Initial Index Disbursements from stockrooms are allowed only upon receipt of properly authorized requisition documents. Management approval is required for stock issuance of amounts above the amount necessary to support scheduled production requirements. Approved requisition documents and inventory movement forms are promptly used to update the inventory records. Prenumbered requisition forms or sequential logs are used to record issuance of materials from stores and inventory movement between locations. The warehouse store is properly locked to prevent unauthorized access and usage Scrap and obsolete inventory are properly segregated. Cycle Counts Obtain, review and document policies and procedures surrounding cycle counts. Observe two cycle counts and document the following What was counted and how it was selected Whether the cycle counter is aware of the quantity on hand prior to his count Agreed-upon test counts to perpetual inventory detail Adjustments to the perpetual inventory detail/general ledger, if applicable Historical accuracy rates Based solely on the work performed, document observations regarding the physical security of inventory. Based on the date and results of the most recent wall-to-wall physical count and the applicability of cycle counts, consider performing the following Agree upon 10 inventory items per the perpetual to the quantity on hand. . Agree upon 10 inventory items on hand to the perpetual Inventory Valuation For facilities using a standard costing system, perform the following: Page 7 of 10Time Project Work Step Initial Index Document procedures for developing current-year standards (raw material, labor and overhead) and the date of the most recent development. Document compliance with corporate policy. On a sample basis (a minimum of 30), test the accuracy of the standards by performing the following: Examine recent invoices supporting the raw material component Examine payroll-related information supporting the labor component, if applicable. Examine the overhead estimate. Recalculate based on available information On a sample basis, examine the method and accuracy of the recording standard to actual variances. Obtain explanations for the standard-to-actual variances greater than the budgeted amount as of the audit date. Examine the entries to record variances and document whether the variances were capitalized or expensed For facilities not using a standard costing system, perform the following: Document procedures for developing current-year labor and overhead amounts. Examine a minimum of 30 recent invoices supporting raw materials and the raw material component of work-in-progress (WIP) and finished goods. Document the results by quantifying the unit cost variances and extrapolationg them to the population Recalculate the labor and overhead calculations and compare them to the amounts capitalized. Document limitations of the ability to recalculate. Inventory Reserves Document inventory greater than 180,270 and 360 days. Document the method for estimating the reserve for excess and obsolete inventory. Document compliance with corporate policy. Obtain a calculation of the estimate for the most recent quarter-end and enter it into the GL. Agree upon significant components to supporting documentation. Document any inconsistencies between the calculation and aging analysis. Page & of 10Time Project Work Step Initial Index Ensure that authorized people adequately approve provisions or write-offs. Review for evidence of approval of inventory write-offs before they are recorded Consignment Inventory Document policies and procedures for consigned inventory. At a minimum, address the following items: The existence of perpetual detail The process for reporting, recording and verifying changes The process for accounting for scrap The results of recent physical counts Document compliance with the corporate policy on consigned inventories. Scrap Document the method for accounting for inventory scrap. At a minimum, address the following The method used to quantify The method used to cost The method used to dispose Through inquiry and observation, ensure that scrap proceeds are collected from the scrap vendor promptly after the collection of scrap materials. Through inquiry and observation, ensure that approval is granted before materials are sent to scrap. Through inquiry and observation, ensure that accounting and the warehouse verify the weight of the scrap materials. Through inquiry and observation, verify that scrap vendors are selected through a bidding process. Page 9 of 10ACCT 436 SECTION INTERNAL AUDITING EXAM 2 Page 10 of 10

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!