Question: INTEGRATED CASE APPLICATION- PINNACLE MANUFACTURING: PART IV 12-37 (OBJECTIVES 12-1, 12-2) In Parts I and II of this case, you performed preliminary analytical procedures and

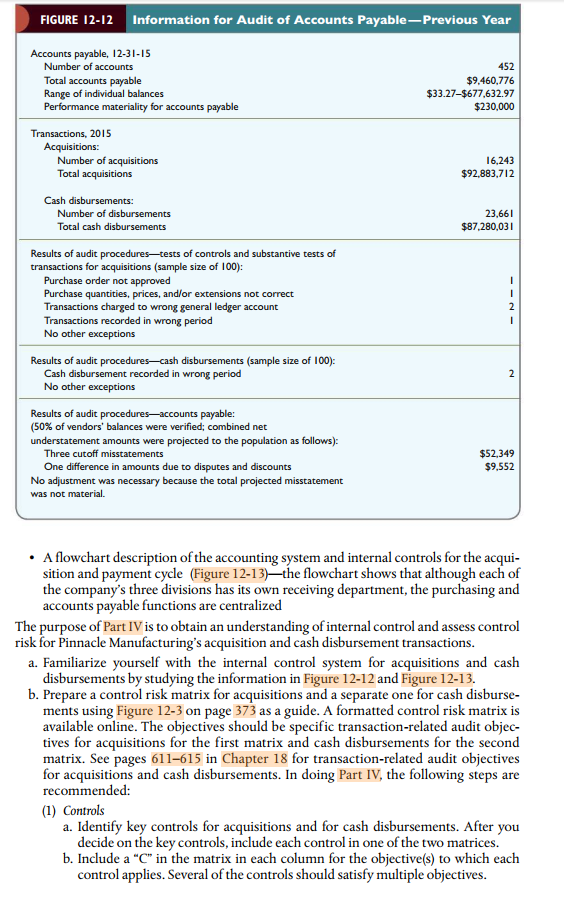

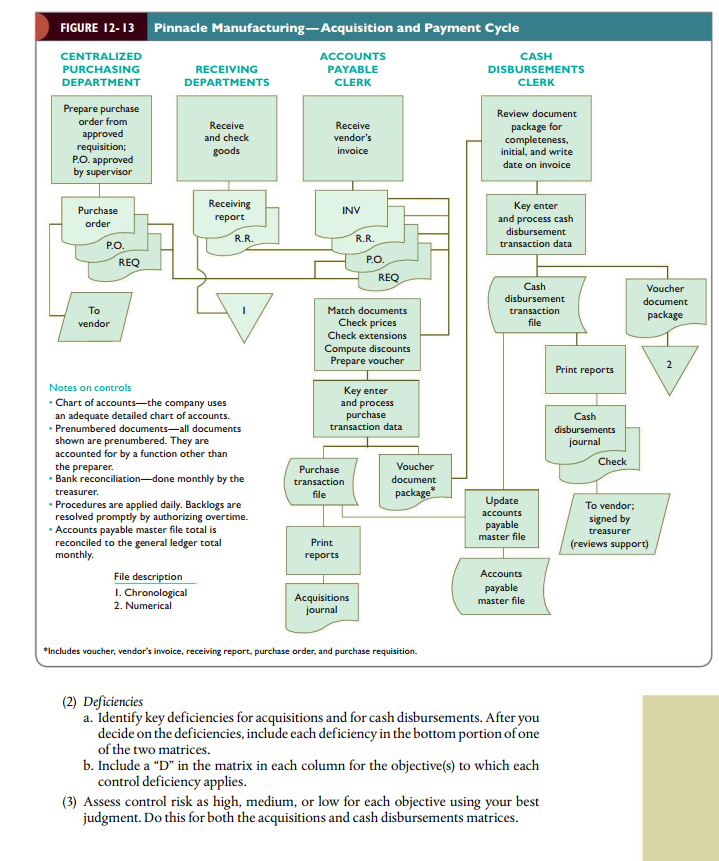

INTEGRATED CASE APPLICATION- PINNACLE MANUFACTURING: PART IV 12-37 (OBJECTIVES 12-1, 12-2) In Parts I and II of this case, you performed preliminary analytical procedures and assessed acceptable audit risk and inherent risk for Pinnacle Manufacturing. In Part III, you considered fraud risks. Your team has been assigned the responsibility of auditing the acquisition and payment cycle and one related balance sheet account, accounts payable. The general approach to be taken will be to reduce assessed control risk to a low level, if possible, for the two main types of transactions affecting accounts payable: acquisitions and cash disbursements. The following are furnished as background information: A summary of key information from the audit of the acquisition and payment cycle and accounts payable in the prior year, which was extracted from the previous audit firm's audit files (Figure 12-12, p. 406) FIGURE 12-12 Information for Audit of Accounts Payable-Previous Year 452 Accounts payable, 12-31-15 Number of accounts Total accounts payable Range of individual balances Performance materiality for accounts payable $9.460.776 $33.27-5677,632.97 $230,000 Transactions, 2015 Acquisitions: Number of acquisitions Total acquisitions 16,243 $92,883.712 Cash disbursements: Number of disbursements Total cash disbursements 23,661 $87,280,031 Results of audit procedures-tests of controls and substantive tests of transactions for acquisitions (sample size of 100): Purchase order not approved Purchase quantities, prices, and/or extensions not correct Transactions charged to wrong general ledger account Transactions recorded in wrong period No other exceptions N- - Results of audit procedures-cash disbursements (sample size of 100): Cash disbursement recorded in wrong period No other exceptions Results of audit procedures-accounts payable: (50% of vendors' balances were verified; combined net understatement amounts were projected to the population as follows): Three cutoff misstatements One difference in amounts due to disputes and discounts No adjustment was necessary because the total projected misstatement was not material. $52,349 $9.552 A flowchart description of the accounting system and internal controls for the acqui- sition and payment cycle (Figure 12-13)-the flowchart shows that although each of the company's three divisions has its own receiving department, the purchasing and accounts payable functions are centralized The purpose of Part IV is to obtain an understanding of internal control and assess control risk for Pinnacle Manufacturing's acquisition and cash disbursement transactions. a. Familiarize yourself with the internal control system for acquisitions and cash disbursements by studying the information in Figure 12-12 and Figure 12-13. b. Prepare a control risk matrix for acquisitions and a separate one for cash disburse- ments using Figure 12-3 on page 373 as a guide. A formatted control risk matrix is available online. The objectives should be specific transaction-related audit objec- tives for acquisitions for the first matrix and cash disbursements for the second matrix. See pages 611-615 in Chapter 18 for transaction-related audit objectives for acquisitions and cash disbursements. In doing Part IV, the following steps are recommended: (1) Controls a. Identify key controls for acquisitions and for cash disbursements. After you decide on the key controls, include each control in one of the two matrices. b. Include a "C" in the matrix in each column for the objective(s) to which each control applies. Several of the controls should satisfy multiple objectives. FIGURE 12-13 Pinnacle Manufacturing-Acquisition and Payment Cycle CENTRALIZED PURCHASING DEPARTMENT RECEIVING DEPARTMENTS ACCOUNTS PAYABLE CLERK CASH DISBURSEMENTS CLERK Prepare purchase order from approved requisition; P.O. approved by supervisor Receive and check goods Receive vendor's invoice Review document package for completeness, initial, and write date on invoice Receiving report Purchase order INV Key enter and process cash disbursement transaction data R.R R.R. P.O REQ P.O. REQ Cash disbursement transaction Voucher document package To vendor Match documents Check prices Check extensions Compute discounts Prepare voucher Print reports Key enter and process purchase transaction data Cash disbursements journal Check Notes on controls Chart of accountsthe company uses an adequate detailed chart of accounts. Prenumbered documentsall documents shown are prenumbered. They are accounted for by a function other than the preparer. Bank reconciliationdone monthly by the treasurer. Procedures are applied daily. Backlogs are resolved promptly by authorizing overtime. Accounts payable master file total is reconciled to the general ledger total monthly Purchase transaction Voucher document package Update accounts payable master file To vendor: signed by treasurer (reviews support) Print reports File description I. Chronological 2. Numerical Accounts payable master file Acquisitions journal *Includes voucher, vendor's invoice, receiving report, purchase order, and purchase requisition. (2) Deficiencies a. Identify key deficiencies for acquisitions and for cash disbursements. After you decide on the deficiencies, include each deficiency in the bottom portion of one of the two matrices. b. Include a "D" in the matrix in each column for the objective(s) to which each control deficiency applies. (3) Assess control risk as high, medium, or low for each objective using your best judgment. Do this for both the acquisitions and cash disbursements matrices. INTEGRATED CASE APPLICATION- PINNACLE MANUFACTURING: PART IV 12-37 (OBJECTIVES 12-1, 12-2) In Parts I and II of this case, you performed preliminary analytical procedures and assessed acceptable audit risk and inherent risk for Pinnacle Manufacturing. In Part III, you considered fraud risks. Your team has been assigned the responsibility of auditing the acquisition and payment cycle and one related balance sheet account, accounts payable. The general approach to be taken will be to reduce assessed control risk to a low level, if possible, for the two main types of transactions affecting accounts payable: acquisitions and cash disbursements. The following are furnished as background information: A summary of key information from the audit of the acquisition and payment cycle and accounts payable in the prior year, which was extracted from the previous audit firm's audit files (Figure 12-12, p. 406) FIGURE 12-12 Information for Audit of Accounts Payable-Previous Year 452 Accounts payable, 12-31-15 Number of accounts Total accounts payable Range of individual balances Performance materiality for accounts payable $9.460.776 $33.27-5677,632.97 $230,000 Transactions, 2015 Acquisitions: Number of acquisitions Total acquisitions 16,243 $92,883.712 Cash disbursements: Number of disbursements Total cash disbursements 23,661 $87,280,031 Results of audit procedures-tests of controls and substantive tests of transactions for acquisitions (sample size of 100): Purchase order not approved Purchase quantities, prices, and/or extensions not correct Transactions charged to wrong general ledger account Transactions recorded in wrong period No other exceptions N- - Results of audit procedures-cash disbursements (sample size of 100): Cash disbursement recorded in wrong period No other exceptions Results of audit procedures-accounts payable: (50% of vendors' balances were verified; combined net understatement amounts were projected to the population as follows): Three cutoff misstatements One difference in amounts due to disputes and discounts No adjustment was necessary because the total projected misstatement was not material. $52,349 $9.552 A flowchart description of the accounting system and internal controls for the acqui- sition and payment cycle (Figure 12-13)-the flowchart shows that although each of the company's three divisions has its own receiving department, the purchasing and accounts payable functions are centralized The purpose of Part IV is to obtain an understanding of internal control and assess control risk for Pinnacle Manufacturing's acquisition and cash disbursement transactions. a. Familiarize yourself with the internal control system for acquisitions and cash disbursements by studying the information in Figure 12-12 and Figure 12-13. b. Prepare a control risk matrix for acquisitions and a separate one for cash disburse- ments using Figure 12-3 on page 373 as a guide. A formatted control risk matrix is available online. The objectives should be specific transaction-related audit objec- tives for acquisitions for the first matrix and cash disbursements for the second matrix. See pages 611-615 in Chapter 18 for transaction-related audit objectives for acquisitions and cash disbursements. In doing Part IV, the following steps are recommended: (1) Controls a. Identify key controls for acquisitions and for cash disbursements. After you decide on the key controls, include each control in one of the two matrices. b. Include a "C" in the matrix in each column for the objective(s) to which each control applies. Several of the controls should satisfy multiple objectives. FIGURE 12-13 Pinnacle Manufacturing-Acquisition and Payment Cycle CENTRALIZED PURCHASING DEPARTMENT RECEIVING DEPARTMENTS ACCOUNTS PAYABLE CLERK CASH DISBURSEMENTS CLERK Prepare purchase order from approved requisition; P.O. approved by supervisor Receive and check goods Receive vendor's invoice Review document package for completeness, initial, and write date on invoice Receiving report Purchase order INV Key enter and process cash disbursement transaction data R.R R.R. P.O REQ P.O. REQ Cash disbursement transaction Voucher document package To vendor Match documents Check prices Check extensions Compute discounts Prepare voucher Print reports Key enter and process purchase transaction data Cash disbursements journal Check Notes on controls Chart of accountsthe company uses an adequate detailed chart of accounts. Prenumbered documentsall documents shown are prenumbered. They are accounted for by a function other than the preparer. Bank reconciliationdone monthly by the treasurer. Procedures are applied daily. Backlogs are resolved promptly by authorizing overtime. Accounts payable master file total is reconciled to the general ledger total monthly Purchase transaction Voucher document package Update accounts payable master file To vendor: signed by treasurer (reviews support) Print reports File description I. Chronological 2. Numerical Accounts payable master file Acquisitions journal *Includes voucher, vendor's invoice, receiving report, purchase order, and purchase requisition. (2) Deficiencies a. Identify key deficiencies for acquisitions and for cash disbursements. After you decide on the deficiencies, include each deficiency in the bottom portion of one of the two matrices. b. Include a "D" in the matrix in each column for the objective(s) to which each control deficiency applies. (3) Assess control risk as high, medium, or low for each objective using your best judgment. Do this for both the acquisitions and cash disbursements matrices

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts