The Starbucks integrative case provides you with an opportunity to apply the entire six-step analysis framework of

Question:

The Starbucks integrative case provides you with an opportunity to apply the entire six-step analysis framework of this textbook to Starbucks, an interesting, profitable, and growing company. Beginning in Chapter 1, and following each chapter of the book, we use the Starbucks Integrative Case to illustrate and apply all of the tools of financial statements analysis and valuation throughout the book. This chapter illustrates the six-step forecasting procedure by applying it to PepsiCo to develop complete financial statement forecasts through Year + 5. In this portion of the integrative case, we rely on our analysis of Starbucks? financial statements through fiscal Year 4 and apply the six-step forecasting procedure of this chapter to develop complete forecasts of Starbucks' financial statements through Year +5.

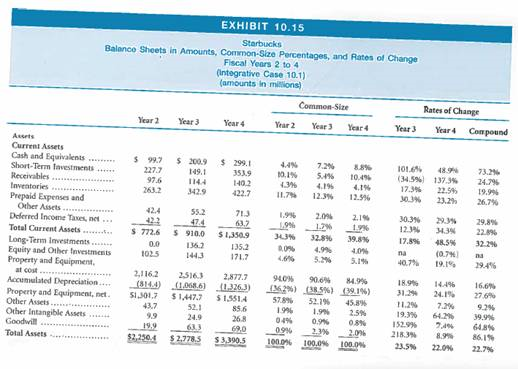

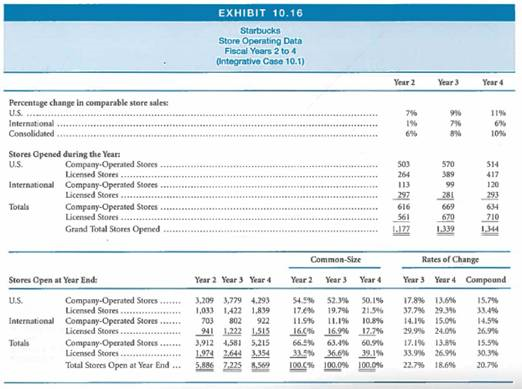

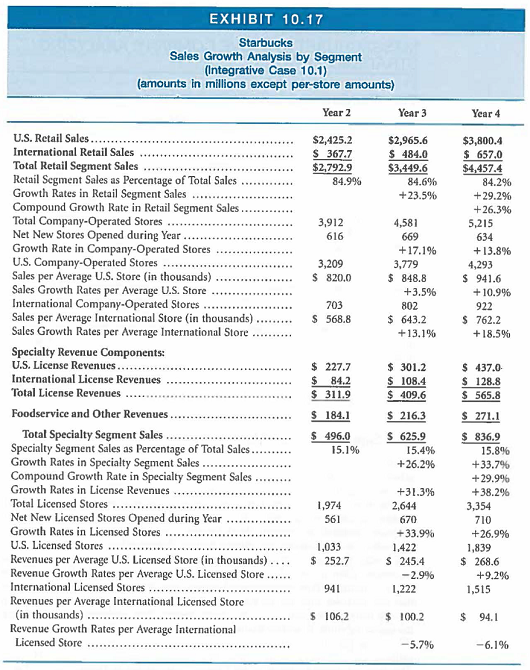

Exhibits 10.14 and 10.15 provide Starbucks? financial statements for fiscal Year 2 through fiscal Year 4, in dollar amounts, common-size, and rate-of-change formats. These data report the financial performance and position of Starbucks and summarize the results of Starbucks' operating, investing, and financing activities. The common-size and rate-of-change balance sheets and income statements for Starbucks highlight relations among accounts and trends over time. Exhibit 10.16 provides store operating data through fiscal Year 4 for Starbucks, including same-store sales growth rates, new store openings, and total numbers of stores open. In addition, Exhibit 10.17 provides a detailed breakdown of Starbucks' revenues and revenue growth by segment and by store. You may wish to refer back to Exhibits 1.24 through 1.28 (Chapter 1) for additional financial statement data. You may also wish to refer back to Exhibit 4.45 (Chapter 4) for a ratio analysis of Starbucks' financial statements. All of the other chapters throughout the text have also illustrated accounting-quality issues and financial statement analysis issues for Starbucks. All of these data and analyses now come into play in this portion of the comprehensive Star bucks case, as we develop forecasts of Star bucks' future financial statements.

Required

Develop complete forecasts of Starbucks? income statements, balance sheets, and statements of cash flows for Years + 1 through +5. As illustrated in this chapter, develop objective and unbiased forecast assumptions for all of Starbucks' future operating, investing, and financing activities through Year + 5, and capture those expectations using financial statement forecasts.

Specifications

a. Build your own spreadsheets to develop and capture your financial statement fore9 cast assumptions and data for Starbucks. Building your own financial statement forecast spreadsheets is an extremely valuable learning exercise in its own right. You can use the examples we developed throughout this chapter for PepsiCo as a model to follow in building your own spreadsheets. If you have already had the learning experience of building your own forecasting spreadsheets, you can build your financial statement forecasts using the FSAP template for Starbucks that accompanies this book. You can download the blank FSAP template from the book?s website address: www.thomsonedu.com/accountinglstickney. Input the accounting data for Starbucks from Exhibits 1.24 to 1.26 (Chapter 1) into the Data Spreadsheet within the blank FSAP template.

b. Starbucks? operating, investing, and financing activities revolve primarily around opening and operating company-owned retail coffee shops in the United States and around the world. Starbucks' annual reports provide useful data on the number of company-operated stores Starbucks owns, the new stores it opens each year, and the same-store sales growth rates. These data reveal that Starbucks' revenues and revenue growth rates differ significantly across different segments and across U.S. versus international stores. Use these data, summarized in Exhibits 10.13 and 10.14, as a basis to forecast (a) Starbucks' future sales from existing stores, (b) the number of new company-operated stores Starbucks will open, (c) future sales from new stores, and (d) capital expenditures for new stores.

c. Starbucks? business also involves generating revenues from licensing Starbucks stores and selling Starbucks coffee and other products through foodservice accounts, grocery stores, warehouse clubs, etc. Use the data in Exhibits 10.13 and 10.14 to build forecasts of future revenues from licensing activities and foodservice and other activities.

d. Use your forecasts of capital expenditures for new stores, together with Starbucks? data on property, plant, and equipment and depreciation, to build a schedule to forecast property, plant, and equipment, and depreciation expense, as described in the chapter and illustrated in Appendix C for PepsiCo.

e. Starbucks appears to use marketable securities as the flexible financial account for balancing the balance sheet. If we follow Starbucks? practice and use marketable securities to balance the balance sheet forecasts, under reasonable forecast assumptions the forecast amounts for marketable securities will become excessively large proportions of total assets by Year +4 and + 5. Therefore, build your financial statement forecasts using dividends as the flexible financial account. This assumption does not match Starbucks' policy through Year 4 of paying zero dividends, But as Starbucks matures and continues to produce excess capital, you can predict that it will initiate a dividend payment policy (or equivalently, a share repurchase policy) to begin distributing excess capital to common equity shareholders.

f. Save your forecast spreadsheets. In subsequent chapters, we will continue to use Starbucks as a comprehensive integrative case. In those chapters, we will apply the valuation models to your forecasts of Starbucks? future earnings, cash flows, and dividends to assess Starbucks' share value.

Expert Answer:

Step 1 of 6 FIFO First In First Out Under this method cost of goods sold is the earliest purchases a... View the full answer

Management Accounting

ISBN: 978-0132570848

6th Canadian edition

Authors: Charles T. Horngren, Gary L. Sundem, William O. Stratton, Phillip Beaulieu