Question: Integrative Expected return, standard deviation, and coefficient of variation An asset is currently being considered by Perth Industries. The probability distribution of expected returns for

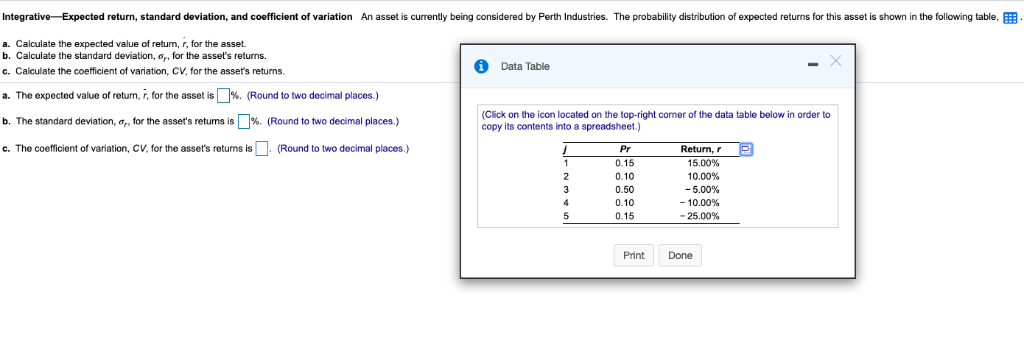

Integrative Expected return, standard deviation, and coefficient of variation An asset is currently being considered by Perth Industries. The probability distribution of expected returns for this asset is shown in the following table, E a. Calculate the expected value of retum, r, for the asset. b. Calculate the standard deviation, o, for the asset's returns. c. Calculate the coefficient of variation, CV, for the asset's returns. Data Table |N(Round a. The expected value of retun, r, for the asset is b. The standard deviation, n for the asset's returns is 1%. (Round to two decimal places.) c. The coefficient of variation, CV, for the asset's returns is. (Round to two decimal places.) to two decimal places.) (Click on the icon located on the top-right corner of the data table below in order to copy its contents into a spreadsheet.) Pr 0.15 0.10 0.50 0.10 0.15 Return, r 15.00% 10.00% -5.00% -10.00% -25.00% Print Done

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts