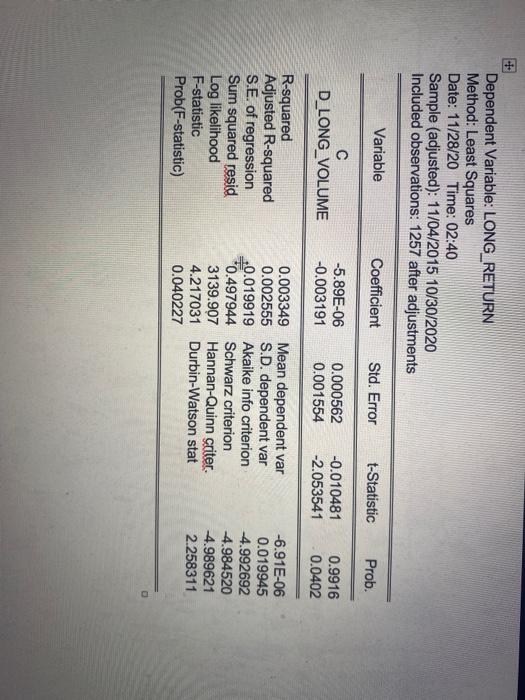

Question: intercept it 10 Dependent Variable: LONG_RETURN Method: Least Squares Date: 11/28/20 Time: 02:40 Sample (adjusted): 11/04/2015 10/30/2020 Included observations: 1257 after adjustments Variable Coefficient Std.

10 Dependent Variable: LONG_RETURN Method: Least Squares Date: 11/28/20 Time: 02:40 Sample (adjusted): 11/04/2015 10/30/2020 Included observations: 1257 after adjustments Variable Coefficient Std. Error t-Statistic Prob. C D_LONG_VOLUME -5.89E-06 -0.003191 0.000562 0.001554 -0.010481 -2.053541 0.9916 0.0402 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.003349 Mean dependent var 0.002555 S.D. dependent var 0.019919 Akaike info criterion *0.497944 Schwarz criterion 3139.907 Hannan-Quinn criter. 4.217031 Durbin-Watson stat 0.040227 -6.91E-06 0.019945 4.992692 4.984520 4.989621 2.258311

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts