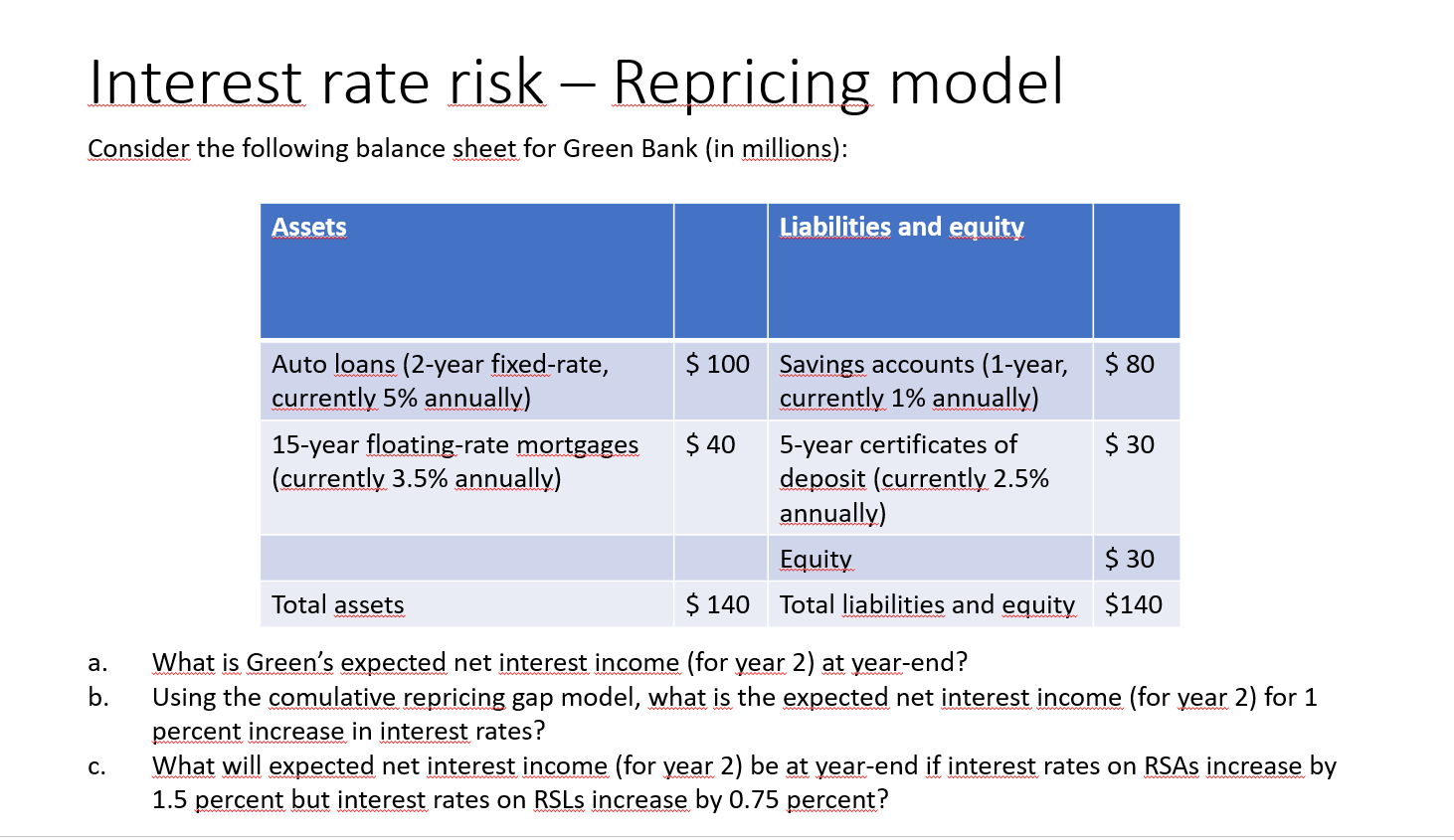

Question: - Interest rate risk Repricing model Consider the following balance sheet for Green Bank (in millions): Assets Liabilities and equity Auto loans (2-year fixed-rate,

- Interest rate risk Repricing model Consider the following balance sheet for Green Bank (in millions): Assets Liabilities and equity Auto loans (2-year fixed-rate, currently 5% annually) $ 100 Savings accounts (1-year, $ 80 currently 1% annually) 15-year floating-rate mortgages (currently 3.5% annually) $ 40 5-year certificates of deposit (currently 2.5% $ 30 annually) Equity $ 30 Total assets $ 140 Total liabilities and equity $140 a. What is Green's expected net interest income (for year 2) at year-end? b. C. Using the comulative repricing gap model, what is the expected net interest income (for year 2) for 1 percent increase in interest rates? What will expected net interest income (for year 2) be at year-end if interest rates on RSAs increase by 1.5 percent but interest rates on RSLs increase by 0.75 percent?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts