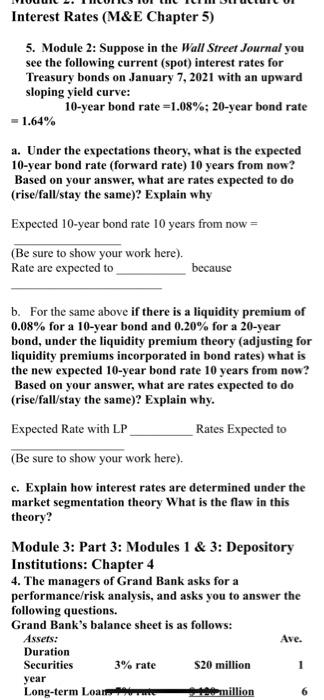

Question: Interest Rates (M&E Chapter 5) 5. Module 2: Suppose in the Wall Street Journal you see the following current (spot) interest rates for Treasury bonds

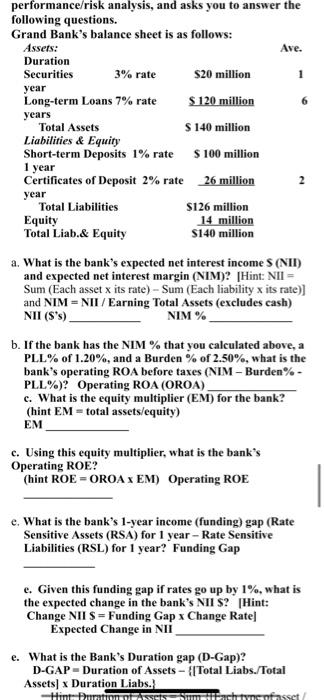

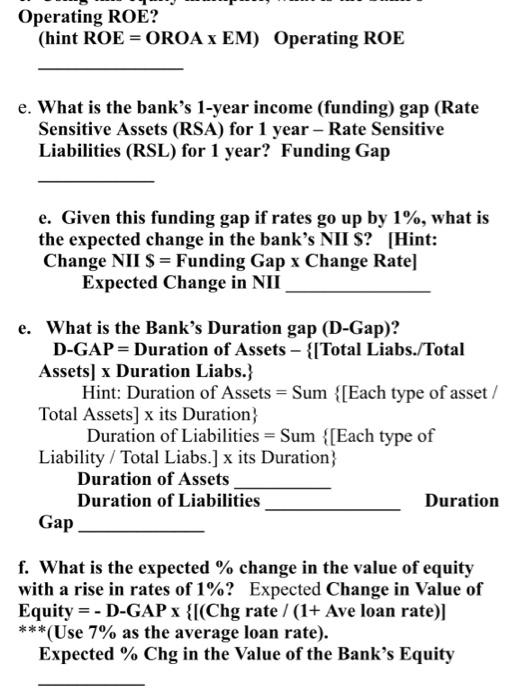

Interest Rates (M&E Chapter 5) 5. Module 2: Suppose in the Wall Street Journal you see the following current (spot) interest rates for Treasury bonds on January 7, 2021 with an upward sloping yield curve: 10-year bond rate=1.08%; 20-year bond rate = 1.64% a. Under the expectations theory, what is the expected 10-year bond rate (forward rate) 10 years from now? Based on your answer, what are rates expected to do (rise/fall/stay the same)? Explain why Expected 10-year bond rate 10 years from now = (Be sure to show your work here). Rate are expected to because b. For the same above if there is a liquidity premium of 0.08% for a 10-year bond and 0.20% for a 20-year bond, under the liquidity premium theory (adjusting for liquidity premiums incorporated in bond rates) what is the new expected 10-year bond rate 10 years from now? Based on your answer, what are rates expected to do (rise/fall/stay the same)? Explain why. Expected Rate with LP _Rates Expected to (Be sure to show your work here). c. Explain how interest rates are determined under the market segmentation theory What is the flaw in this theory? Module 3: Part 3: Modules 1 & 3: Depository Institutions: Chapter 4 4. The managers of Grand Bank asks for a performance/risk analysis, and asks you to answer the following questions. Grand Bank's balance sheet is as follows: Assets: Duration Securities 3% rate $20 million year Long-term Loan million Ave. 1 1 performance/risk analysis, and asks you to answer the following questions. Grand Bank's balance sheet is as follows: Assets: Ave. Duration Securities 3% rate $20 million year Long-term Loans 7% rate $ 120 million years Total Assets S 140 million Liabilities & Equity Short-term Deposits 1% rate $ 100 million 1 year Certificates of Deposit 2% rate 26 million year Total Liabilities S126 million Equity 14 million Total Liab.& Equity S140 million a. What is the bank's expected net interest income S (NII) and expected net interest margin (NIM)? [Hint: NII = Sum (Each asset x its rate) - Sum (Each liability x its rate)] and NIMENII / Earning Total Assets (excludes cash) NII (S's) NIM% b. If the bank has the NIM% that you calculated above, a PLL% of 1.20%, and a Burden % of 2.50%, what is the bank's operating ROA before taxes (NIM - Burden%- PLL%Operating ROA (OROA) c. What is the equity multiplier (EM) for the bank? (hint EM-total assets/equity) EM c. Using this equity multiplier, what is the bank's Operating ROE? (hint ROE = OROA XEM) Operating ROE e. What is the bank's 1-year income (funding) gap (Rate Sensitive Assets (RSA) for 1 year - Rate Sensitive Liabilities (RSL) for 1 year? Funding Gap e. Given this funding gap if rates go up by 1%, what is the expected change in the bank's NII S? [Hint: Change NII S = Funding Gap Change Rate] Expected Change in NII e. What is the Bank's Duration gap (D-Gap)? D-GAP - Duration of Assets - {[Total Liabs./Total Assets) * Duration Liabs. -Hint Finn SEIS tymenfasset Operating ROE? (hint ROE = OROA XEM) Operating ROE e. What is the bank's 1-year income (funding) gap (Rate Sensitive Assets (RSA) for 1 year - Rate Sensitive Liabilities (RSL) for 1 year? Funding Gap e. Given this funding gap if rates go up by 1%, what is the expected change in the bank's NII S? (Hint: Change NII S = Funding Gap x Change Rate] Expected Change in NII e. What is the Bank's Duration gap (D-Gap)? D-GAP = Duration of Assets {[Total Liabs./Total Assets) x Duration Liabs.} Hint: Duration of Assets = Sum {[Each type of asset / Total Assets] x its Duration Duration of Liabilities = Sum {[Each type of Liability/Total Liabs.] x its Duration Duration of Assets Duration of Liabilities Duration Gap f. What is the expected % change in the value of equity with a rise in rates of 1%? Expected Change in Value of Equity = - D-GAP x {[(Chg rate / (1+ Ave loan rate) ***(Use 7% as the average loan rate). Expected % Chg in the Value of the Bank's Equity Interest Rates (M&E Chapter 5) 5. Module 2: Suppose in the Wall Street Journal you see the following current (spot) interest rates for Treasury bonds on January 7, 2021 with an upward sloping yield curve: 10-year bond rate=1.08%; 20-year bond rate = 1.64% a. Under the expectations theory, what is the expected 10-year bond rate (forward rate) 10 years from now? Based on your answer, what are rates expected to do (rise/fall/stay the same)? Explain why Expected 10-year bond rate 10 years from now = (Be sure to show your work here). Rate are expected to because b. For the same above if there is a liquidity premium of 0.08% for a 10-year bond and 0.20% for a 20-year bond, under the liquidity premium theory (adjusting for liquidity premiums incorporated in bond rates) what is the new expected 10-year bond rate 10 years from now? Based on your answer, what are rates expected to do (rise/fall/stay the same)? Explain why. Expected Rate with LP _Rates Expected to (Be sure to show your work here). c. Explain how interest rates are determined under the market segmentation theory What is the flaw in this theory? Module 3: Part 3: Modules 1 & 3: Depository Institutions: Chapter 4 4. The managers of Grand Bank asks for a performance/risk analysis, and asks you to answer the following questions. Grand Bank's balance sheet is as follows: Assets: Duration Securities 3% rate $20 million year Long-term Loan million Ave. 1 1 performance/risk analysis, and asks you to answer the following questions. Grand Bank's balance sheet is as follows: Assets: Ave. Duration Securities 3% rate $20 million year Long-term Loans 7% rate $ 120 million years Total Assets S 140 million Liabilities & Equity Short-term Deposits 1% rate $ 100 million 1 year Certificates of Deposit 2% rate 26 million year Total Liabilities S126 million Equity 14 million Total Liab.& Equity S140 million a. What is the bank's expected net interest income S (NII) and expected net interest margin (NIM)? [Hint: NII = Sum (Each asset x its rate) - Sum (Each liability x its rate)] and NIMENII / Earning Total Assets (excludes cash) NII (S's) NIM% b. If the bank has the NIM% that you calculated above, a PLL% of 1.20%, and a Burden % of 2.50%, what is the bank's operating ROA before taxes (NIM - Burden%- PLL%Operating ROA (OROA) c. What is the equity multiplier (EM) for the bank? (hint EM-total assets/equity) EM c. Using this equity multiplier, what is the bank's Operating ROE? (hint ROE = OROA XEM) Operating ROE e. What is the bank's 1-year income (funding) gap (Rate Sensitive Assets (RSA) for 1 year - Rate Sensitive Liabilities (RSL) for 1 year? Funding Gap e. Given this funding gap if rates go up by 1%, what is the expected change in the bank's NII S? [Hint: Change NII S = Funding Gap Change Rate] Expected Change in NII e. What is the Bank's Duration gap (D-Gap)? D-GAP - Duration of Assets - {[Total Liabs./Total Assets) * Duration Liabs. -Hint Finn SEIS tymenfasset Operating ROE? (hint ROE = OROA XEM) Operating ROE e. What is the bank's 1-year income (funding) gap (Rate Sensitive Assets (RSA) for 1 year - Rate Sensitive Liabilities (RSL) for 1 year? Funding Gap e. Given this funding gap if rates go up by 1%, what is the expected change in the bank's NII S? (Hint: Change NII S = Funding Gap x Change Rate] Expected Change in NII e. What is the Bank's Duration gap (D-Gap)? D-GAP = Duration of Assets {[Total Liabs./Total Assets) x Duration Liabs.} Hint: Duration of Assets = Sum {[Each type of asset / Total Assets] x its Duration Duration of Liabilities = Sum {[Each type of Liability/Total Liabs.] x its Duration Duration of Assets Duration of Liabilities Duration Gap f. What is the expected % change in the value of equity with a rise in rates of 1%? Expected Change in Value of Equity = - D-GAP x {[(Chg rate / (1+ Ave loan rate) ***(Use 7% as the average loan rate). Expected % Chg in the Value of the Bank's Equity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts