Question: Intermediate 1 Terry Part #1: Chapter 3 Goal: To practice making necessary correcting and adjusting entries and using them to create an adjusted trial balance.

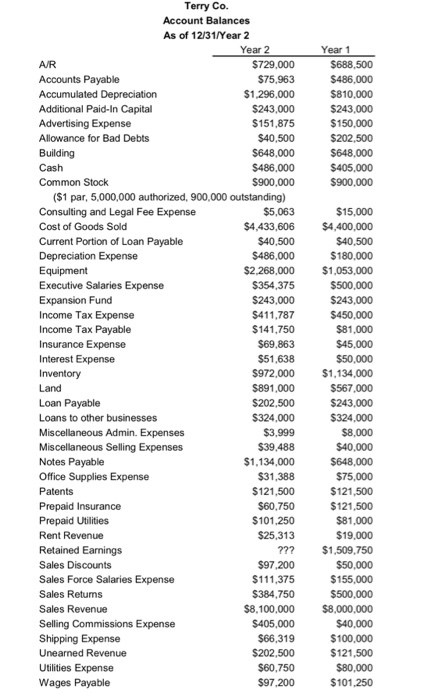

Intermediate 1 Terry Part #1: Chapter 3 Goal: To practice making necessary correcting and adjusting entries and using them to create an adjusted trial balance. (See Topic Guides AC 6, 11, 12, 14). Information: The table on the next page reports Terry's account balances on December 31" for the current and prior years. The following entries have not yet been made for the current year: . During the year the sales department wrote off $162,000 of accounts receivable (already included in the current account balances). They have now decided that 7% of their ending A/R balance is uncollectible. Terry uses the Percentage of A/R method for recognizing bad debt expense. . During the year the board declared and paid a $120,000 dividend. . On September ist, a year's premiums on a new insurance policy was prepaid for $120,000. The original payment was recorded as a debit to Prepaid Insurance. No other entries have been made for this contract since that time. Terry's reported income tax expense (see below) includes an estimate for this year's taxes. Only the three adjustments mentioned above have not yet been included in this tax estimate. Because of this, you will need to record any tax effects from the transactions throughout this case (starting with the tax effects, if any, of these three entries). Since another tax payment will not be made until April, these adjustments should be accounted for in Income Tax Expense and Income Tax Payable. Terry's tax rate is 30%. Assignment: Calculations 1. Make the appropriate journal entries, if any, to account for the adjustments mentioned above (including any necessary changes to income tax expense). 2. Create Terry's Year 2 adjusted trial balance. Hint: Trial balances need to be in a specific order and they are only for the current year! Critical Thinking 3. Do you think it's a problem that Terry is still making these changes, even when all of their other numbers are set? What do these last minute corrections suggest about the company's accounting department? Year 1 $688,500 $486.000 $810,000 $243,000 $150.000 $202,500 $648,000 $405,000 $900,000 Building Terry Co. Account Balances As of 12/31/Year 2 Year 2 A/R $729,000 Accounts Payable $75,963 Accumulated Depreciation $1.296,000 Additional Paid-In Capital $243,000 Advertising Expense $151,875 Allowance for Bad Debts $40,500 $648,000 Cash $486,000 Common Stock $900,000 ($1 par, 5,000,000 authorized, 900,000 outstanding) Consulting and Legal Fee Expense $5,063 Cost of Goods Sold $4,433,606 Current Portion of Loan Payable $40,500 Depreciation Expense $486.000 Equipment $2,268,000 Executive Salaries Expense $354,375 Expansion Fund $243,000 Income Tax Expense $411,787 Income Tax Payable $141.750 Insurance Expense $69.863 Interest Expense $51,638 Inventory $972.000 Land $891,000 Loan Payable $202,500 Loans to other businesses $324,000 Miscellaneous Admin. Expenses $3,999 Miscellaneous Selling Expenses $39.488 Notes Payable $1,134,000 Office Supplies Expense $31,388 Patents $121,500 Prepaid Insurance $60.750 Prepaid Utilities $101,250 Rent Revenue $25,313 Retained Earnings ??? Sales Discounts $97,200 Sales Force Salaries Expense $111,375 Sales Returns $384.750 Sales Revenue $8,100,000 Selling Commissions Expense $405,000 Shipping Expense $66,319 Unearned Revenue $202,500 Utilities Expense $60.750 Wages Payable $97,200 $15,000 $4,400,000 $40,500 $180.000 $1,053,000 $500,000 $243,000 $450,000 $81,000 $45,000 $50,000 $1,134,000 $567.000 $243,000 $324.000 $8,000 $40,000 $648,000 $75,000 $121,500 $121,500 $81,000 $19.000 $1,509.750 $50,000 $ 155,000 $500,000 $8,000,000 $40.000 $100,000 $121,500 $80,000 $101.250

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts