Question: Intermediate Accounting A B C D 1 Question Three Klitschko Theft Prevention entered into a one-year contract with J-Mart to provide security at their retail

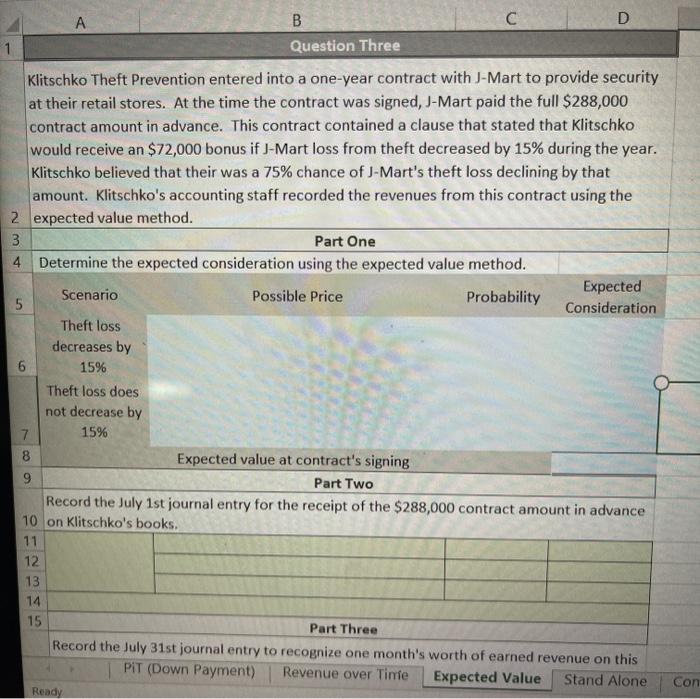

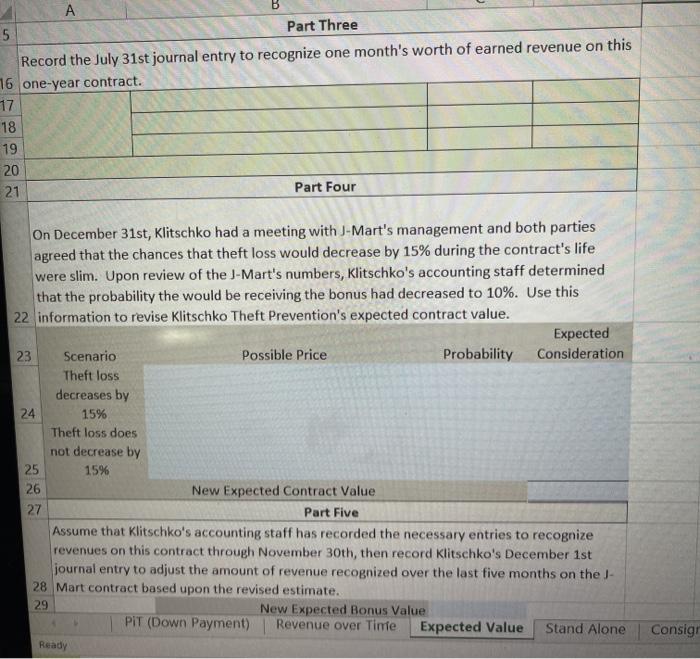

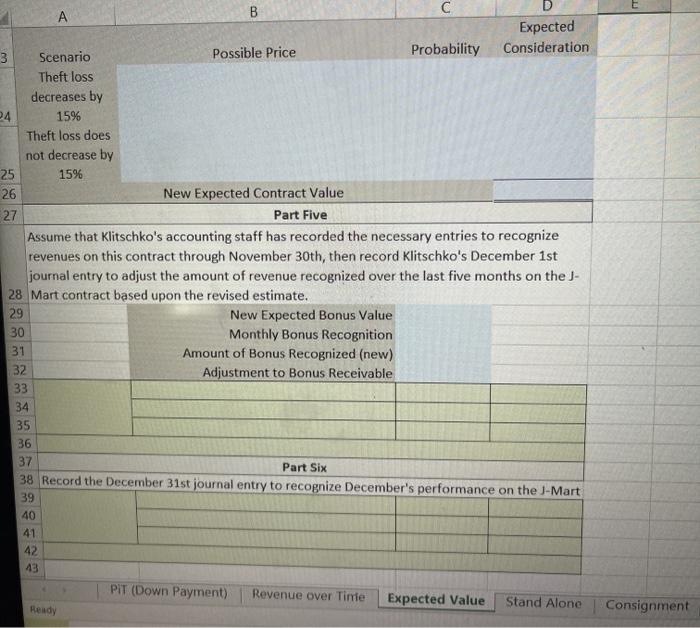

A B C D 1 Question Three Klitschko Theft Prevention entered into a one-year contract with J-Mart to provide security at their retail stores. At the time the contract was signed, J-Mart paid the full $288,000 contract amount in advance. This contract contained a clause that stated that Klitschko would receive an $72,000 bonus if J-Mart loss from theft decreased by 15% during the year. Klitschko believed that their was a 75% chance of J-Mart's theft loss declining by that amount. Klitschko's accounting staff recorded the revenues from this contract using the 2 expected value method. 3 Part One 4 Determine the expected consideration using the expected value method. Expected Scenario Possible Price Probability 5 Consideration Theft loss decreases by 6 15% Theft loss does not decrease by 7 15% Expected value at contract's signing 9 Part Two Record the July 1st journal entry for the receipt of the $288,000 contract amount in advance 10 on Klitschko's books. 11 12 13 14 15 Part Three Record the July 31st journal entry to recognize one month's worth of earned revenue on this PIT (Down Payment) Revenue over Tinte Expected Value Stand Alone Con Ready 5 Part Three Record the July 31st journal entry to recognize one month's worth of earned revenue on this 16 one-year contract. 17 18 19 20 21 Part Four On December 31st, Klitschko had a meeting with J-Mart's management and both parties agreed that the chances that theft loss would decrease by 15% during the contract's life were slim. Upon review of the J-Mart's numbers, Klitschko's accounting staff determined that the probability the would be receiving the bonus had decreased to 10%. Use this 22 information to revise Klitschko Theft Prevention's expected contract value. Expected 23 Scenario Possible Price Probability Consideration Theft loss decreases by 24 15% Theft loss does not decrease by 25 15% 26 New Expected Contract Value 27 Part Five Assume that Klitschko's accounting staff has recorded the necessary entries to recognize revenues on this contract through November 30th, then record Klitschko's December 1st journal entry to adjust the amount of revenue recognized over the last five months on the )- 28 Mart contract based upon the revised estimate. 29 New Expected Bonus Value PIT (Down Payment) Revenue over Time Expected Value Stand Alone Ready Consigt A B Expected 3 Scenario Possible Price Probability Consideration Theft loss decreases by 24 15% Theft loss does not decrease by 25 15% 26 New Expected Contract Value 27 Part Five Assume that Klitschko's accounting staff has recorded the necessary entries to recognize revenues on this contract through November 30th, then record Klitschko's December 1st journal entry to adjust the amount of revenue recognized over the last five months on the J- 28 Mart contract based upon the revised estimate. 29 New Expected Bonus Value 30 Monthly Bonus Recognition 31 Amount of Bonus Recognized (new) 32 Adjustment to Bonus Receivable 33 34 35 36 37 Part Six 38 Record the December 31st journal entry to recognize December's performance on the J-Mart 39 40 41 42 43 PIT (Down Payment) Revenue over Time Expected Value Stand Alone Ready Consignment A B C D 1 Question Three Klitschko Theft Prevention entered into a one-year contract with J-Mart to provide security at their retail stores. At the time the contract was signed, J-Mart paid the full $288,000 contract amount in advance. This contract contained a clause that stated that Klitschko would receive an $72,000 bonus if J-Mart loss from theft decreased by 15% during the year. Klitschko believed that their was a 75% chance of J-Mart's theft loss declining by that amount. Klitschko's accounting staff recorded the revenues from this contract using the 2 expected value method. 3 Part One 4 Determine the expected consideration using the expected value method. Expected Scenario Possible Price Probability 5 Consideration Theft loss decreases by 6 15% Theft loss does not decrease by 7 15% Expected value at contract's signing 9 Part Two Record the July 1st journal entry for the receipt of the $288,000 contract amount in advance 10 on Klitschko's books. 11 12 13 14 15 Part Three Record the July 31st journal entry to recognize one month's worth of earned revenue on this PIT (Down Payment) Revenue over Tinte Expected Value Stand Alone Con Ready 5 Part Three Record the July 31st journal entry to recognize one month's worth of earned revenue on this 16 one-year contract. 17 18 19 20 21 Part Four On December 31st, Klitschko had a meeting with J-Mart's management and both parties agreed that the chances that theft loss would decrease by 15% during the contract's life were slim. Upon review of the J-Mart's numbers, Klitschko's accounting staff determined that the probability the would be receiving the bonus had decreased to 10%. Use this 22 information to revise Klitschko Theft Prevention's expected contract value. Expected 23 Scenario Possible Price Probability Consideration Theft loss decreases by 24 15% Theft loss does not decrease by 25 15% 26 New Expected Contract Value 27 Part Five Assume that Klitschko's accounting staff has recorded the necessary entries to recognize revenues on this contract through November 30th, then record Klitschko's December 1st journal entry to adjust the amount of revenue recognized over the last five months on the )- 28 Mart contract based upon the revised estimate. 29 New Expected Bonus Value PIT (Down Payment) Revenue over Time Expected Value Stand Alone Ready Consigt A B Expected 3 Scenario Possible Price Probability Consideration Theft loss decreases by 24 15% Theft loss does not decrease by 25 15% 26 New Expected Contract Value 27 Part Five Assume that Klitschko's accounting staff has recorded the necessary entries to recognize revenues on this contract through November 30th, then record Klitschko's December 1st journal entry to adjust the amount of revenue recognized over the last five months on the J- 28 Mart contract based upon the revised estimate. 29 New Expected Bonus Value 30 Monthly Bonus Recognition 31 Amount of Bonus Recognized (new) 32 Adjustment to Bonus Receivable 33 34 35 36 37 Part Six 38 Record the December 31st journal entry to recognize December's performance on the J-Mart 39 40 41 42 43 PIT (Down Payment) Revenue over Time Expected Value Stand Alone Ready Consignment

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts