Question: Internal Assessment: Financial Performance and Future Financial Capacity(FIND REFERENCES BELOW) Please help, make an overall assessment of the financial performance of the organization and indicate

Internal Assessment: Financial Performance and Future Financial Capacity(FIND REFERENCES BELOW)

Please help, make an overall assessment of the financial performance of the organization and indicate the financial strength and future financial capacity of the firm to carry out possible future initiatives/strategies (Future financial capacity refers to the amount of capital (money) the company can raise to invest in the next five years). Keep in mind the future orientation of the assessment rather than living in the past.

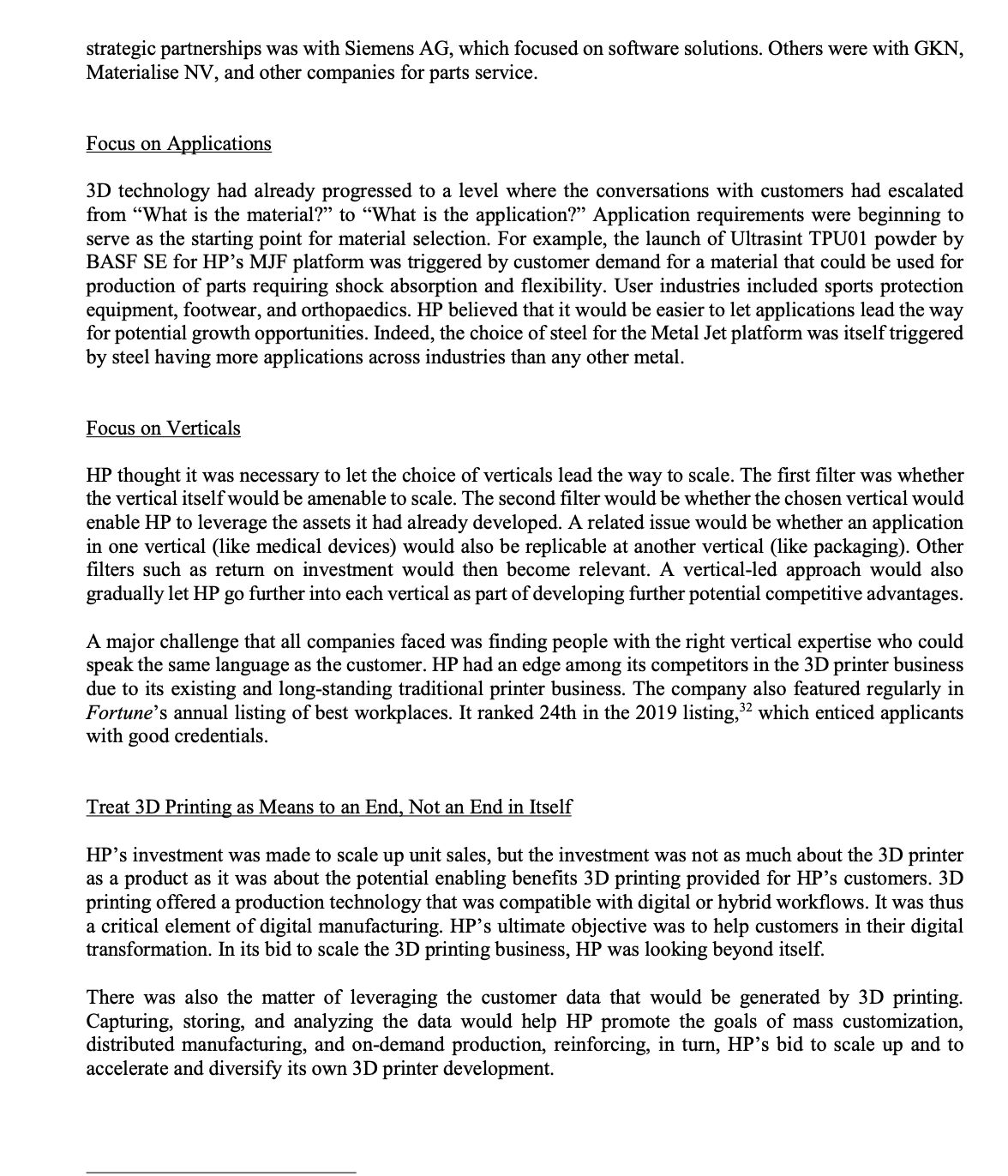

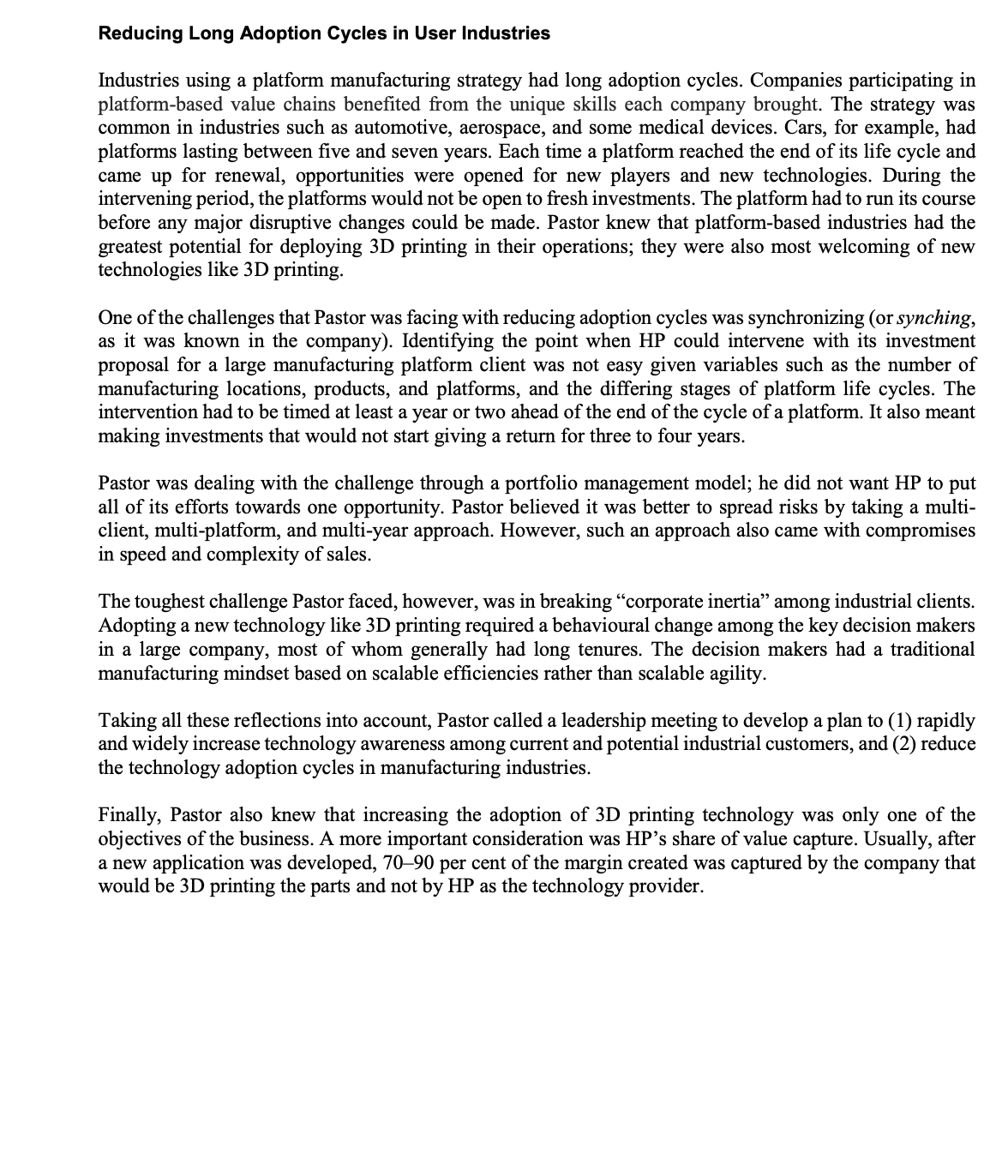

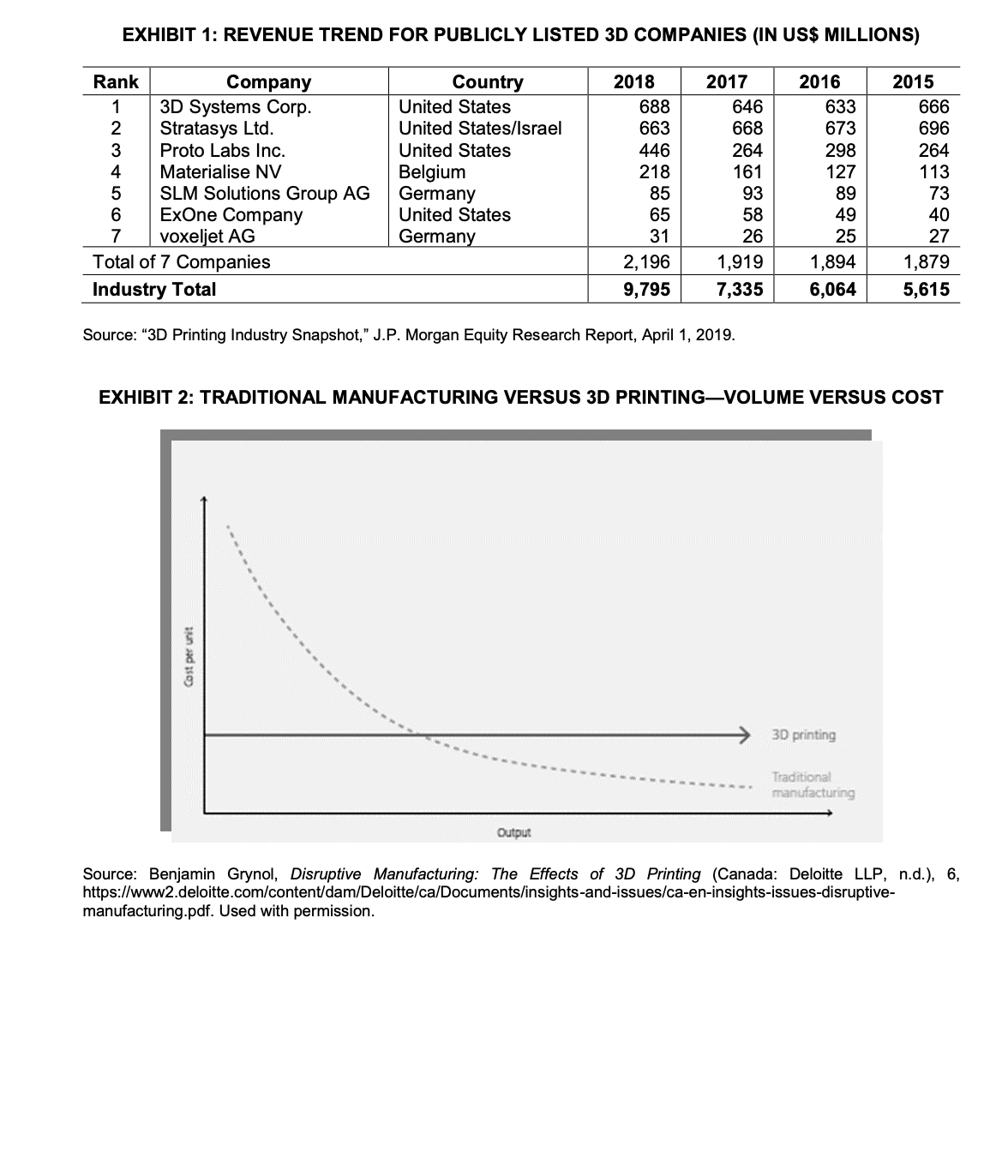

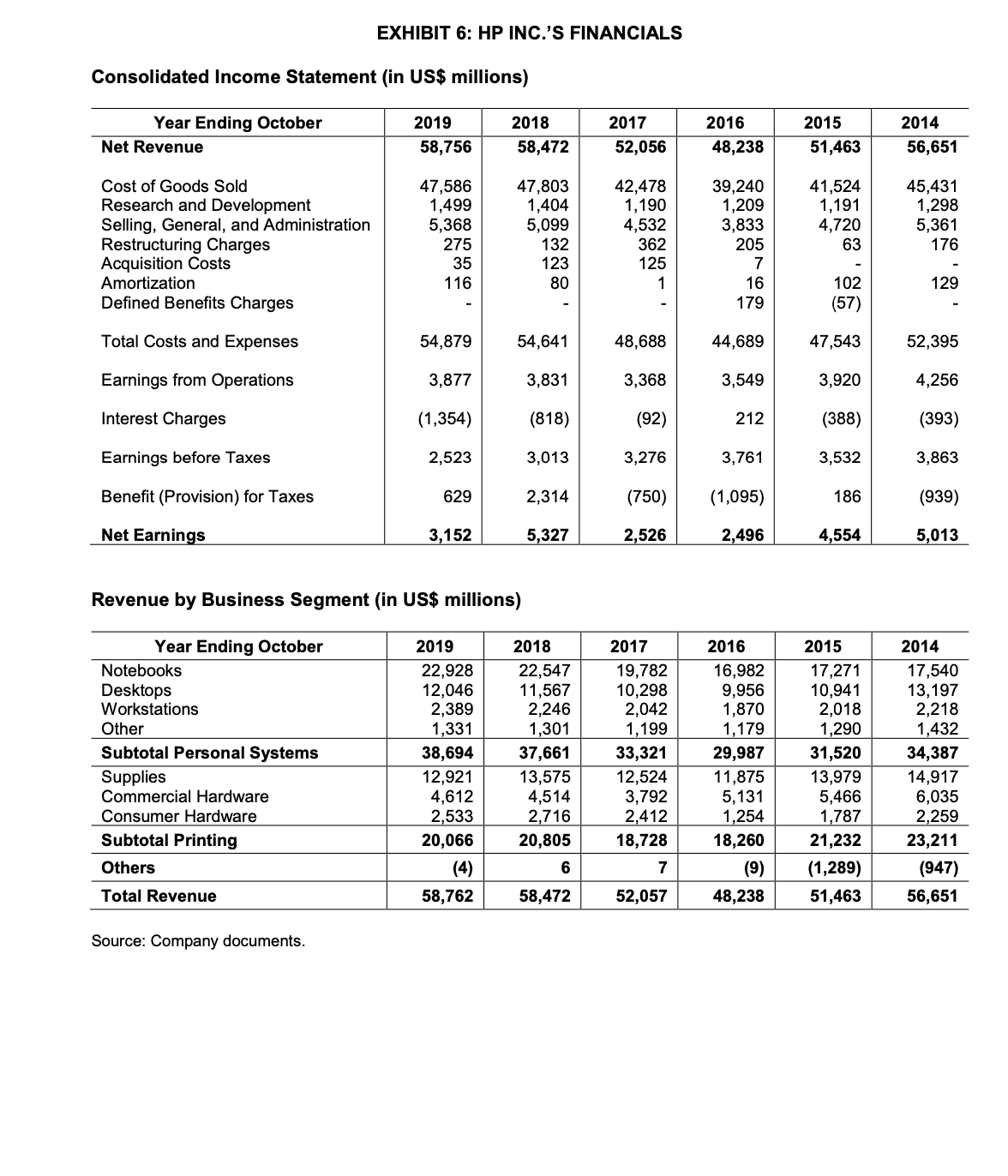

In April 2020, Ramon Pastor, interim president of HP Inc. (HP)'s three-dimensional (3D) printing and digital manufacturing business, took a moment to reect on the rise of the company's 3D Printing and Digital Manufacturing Center of Excellence, located in Barcelona, Spain. Pastor was a 28-year technology veteran at HP who had been promoted to his current position in September 2019. His new mandate was to spearhead I-IP's efforts to transform the manufacturing ecosystems of the company's industrial customers by encouraging them to deploy I-[P's 3D printer systems. There was a strong belief in the industry that 3D printing had reached a tipping point: from a niche position for three decades, when its applications had been conned to low-volume prototyping and specialty uses, 3D printing was about to move into high-volume industrial applications. However, 3D technologies were still evolving, albeit rapidly and much more clearly, on the path to becoming an alternative to conventional manufacturing. HP was a US multinational that operated in the global information technology sector; in 2019, it ranked 55th in the Fortune 500 list.1 HP had only formally entered the 3D printing business three years earlier as a manufacturer of 3D printers. It was currently moving from low-volume production to mid-volume production of an ever-growing range of 3D printers. HP was also aiming to become the leader in the 3D printing industry, particularly drawing on its own Multi Jet Fusion (MJF) technology. MJF was signicantly faster and cheaper than the 3D printers that were currently available in the market. As Pastor contemplated how to move forward, he identied three questions that needed answering: (1) How should HP promote technology awareness among current and potential industrial customers, large and small? (2) How should HP scale up its production of 3D printers? (3) How could HP promote reductions in technology adoption cycles, which were long in manufacturing industries? 3D PRINTING INDUSTRY: BACKGROUND 3D printing was a key technology in the analogue-to-digital disruption happening in manufacturing sectors worldwide. By transforming the design and production of goods, facilitating their mass customization, and enabling their creation closer to the points of consumption, 3D printing was changing the economics of the global manufacturing industry, valued at US$12 trillion.2 3D printing was also part of a paradigm shift in which producers were yielding power to consumers. As of the end of 2018, the 3D printing industry had reached approximately $9.8 billion in revenues worldwide and was projected to reach $40.8 billion by 2024 (see Exhibit 1).3 The top four players Stratasys Ltd., 3D Systems Corporation, Proto Labs Inc., and Materialise NVtogether held 20 per cent of the market share in 2018. HP was a new entrant. Movement in the 3D industry was progressive. Prototype applications progressed to manufacturing applications even while the 3D technologies were improving in productivity, quality, and economics to become an alternative for real production runs. MJ'F, I-lP's innovation, was designed to move I-IP's 3D printersand lead the larger 3D printing industry itselffrom prototyping applications to industrial applications. Assembly Manufacturing versus 3D Printing 3D printing brought a major disruption to the manufacturing industry: while assembly lines were geared for economies of scale and built around volume and labour efciencies, 3D printing was geared for economies of scope, built around small batches of customized units, often even single units\" The advantage of 3D printing was that a small number of goods could be produced at incremental cost without having to reach the scale efciencies that were required in traditional production line manufacturing processes. Traditional manufacturing was good for producing large quantities of products continuously while 3D printing aligned a company's scaling capacity more closely to the quickly shifting or increasingly individualistic needs of markets. 3D printing also lowered the barriers to market entry, not only by reducing the minimum efcient scale of production but also by enabling production to be localized to the points of consumption, making internationalization easier, particularly during times of increasing global trade wars. 3D printing could reorient the manufacturing footprint towards local facilities feeding off local raw materials. Considering that 2 per cent of the world's gross domestic product was known to be in transit just on United Parcel Service (UPS) Inc.'s transportation vehicles alone at any point in time} 3D printing unlocked huge efciency gains and completely new business models. It also reduced the need to outsource production to low-cost economies.6 While assembly-based manufacturing ensured progressive reduction in unit costs as production volumes rose, 3D printing ensured lower costs from the rst unit of output (see Exhibit 2).7 How the Printer Worked An MJF 3D printer operated like a two-dimensional (2D) inkjet printer, but instead of paper, the 3D printer used a plastic material in powder form, which was laid down in successive layers. And instead of ink, a 3D printer used a combination of uids to form the dimensions, layer by layer, under the inuence of infrared radiation.8 The starting point for both printers was computer-fed instructions; for a 3D printer, the instructions began with the creation of a computer-aided design of the object to be created. The digital blueprint was then transferred to the 3D printer. An important component of a 3D printer was the print bar, which was identical to a scanning bar in an inkjet printer. As the bar moved back and forth, 30,000 nozzles sprayed a print platform at 350 million drops of uid per second.9 The object was constructed in layers from the base up, inrsing a new layer of material on the old layer in an additive process. Fabricating an object layer by layer ensured a design of greater intricacy and facilitated customization. While large-scale industrial applications for 3D printing were imminent, companies were also working on meeting consumer applications. Printing spare parts was an example of what was to come. For instance, a consumer who required a spare part for a vacuum cleaner of any brandone that had broken down at home and had also been discontinued by the manufacturercould go online, nd the part from a database of geometries, download the digital data, and print the spare part on a 3D printer at a kiosk in a mall. A major limitation of 3D printing was that it was slow to produce large volumes or large-sized products. In addition, the quality of the product, produced from an entry-level 3D printer in particular, was still inferior to the quality of that produced with traditional parts from assembly-based manufacturing methods. However, the limitations were bound to be overcome in the near future, considering the exponential progress being made in 3D printing technologies. Many companies were working on the technologies. HP, for example, held 2,285 patents related to 3D printing (see Exhibit 3). As a country, the United States held the largest market share in 3D printing worldwide, at 38.1 per cent (see Exhibit 4). In 2019, US researchers filed the most 3D-related patents 44,1'?7in a single year, with China second at 18,838 (see Exhibit 5). Several advanced technologies were under different stages of discovery, ne-tuning, and implementation. They included material jetting, material extrusion, binder jetting, directed energy deposition, powder bed fusion, and photo-polymerization. Each technology was unique in the technical requirements of material variety, speed, and quality of nish. Benets The benets of 3D printing occurred throughout the value chain. In pre-production, for example, 3D printing reduced the need for tooling, which was considered a high-cost activity. In production, 3D printing reduced the number of sub-assemblies, thereby accelerating time to market and reducing supplier-based complexities. From an inventory perspective, 3D printing reduced the cost of logistics, which had a cascading effect on the value chain. It enabled manufacturers to match demand one to one, and by ensuring manufacturing on demand, 3D printing reduced the need to store certain parts over years. 3D printing also helped to eliminate scrap and waste, and it simplied the supply chain.10 The disruptive power of 3D printing was that it led to disintermediation in the traditional manufacturing value chain. Disintermediation was already happening in the world of dentistry, where direct, digitally enabled connections between consumers and the companies that made dental products such as braces reduced the role of dentists. Business Models There were two distinct business models in the 3D printing industry: a low-cost online business model and a technology expert business model.11 Companies following the low-cost online model provided access to easy-to-use printers at low cost. Their value proposition was convenience. The companies preferred to do business online with web shops, although some companies also used the retailer channel. Since they put little effort into innovation, the companies rarely offered specic software to operate the printers. The segment was mainly focusing on the consumer market, anticipating when the demand for consumer applications would increase as the 3D industry became more broadly available.12 Companies following the technology expert model provided value in expertise, innovation, and quality. Their focus was exible printers that were supported with specic software and training. They used retailers and direct sales as primary distribution channels. Some companies operated physical stores where they also sold consumables.\" New business models were surfacing in the 3D printing ecosystem. An example was a service bureau that enabled entrepreneursstart-ups, small-scale, and medium-scaleto access digital manufacturing methods to either prototype or manufacture new products. Service bureaus were lowering the barriers for entry into business in addition to providing greater degrees of manufacturing speed and exibility.14 HP: COMPANY BACKGROUND HP was a US multinational that operated in the global information technology sector. It was part of an enterprise that was established by Stanford graduates Bill Hewlett and David Packard in 1939 in a one-car garage in Palo Alto, California. The garage had since become a landmark in the city and ofcially commemorated as the \"Birthplace of Silicon Valley.\" Producing a line of electronic test equipment in its early years, what was then the Hewlett-Packard Company went on over the next few decades to become a leading manufacturer of personal computers (PCs). The company's management style, known as the HP Way, was adopted by many businesses worldwide. The HP Way was based on self-nanced growth, differentiated products, respect for employees, commitment to innovation, and good corporate citizenship.15 For the year ending October 2019, HP had revenues of $58.?5 billion and net earnings of $3.1 billion (see Exhibit 6). Employing 56,000 people worldwide, I-IP focused on two core business segments: personal systems and printing. The personal systems segment offered commercial and consumer desktop and notebook PCs in addition to related accessories, software, support, and services. The printing segment provided consumer and commercial printer hardware, supplies, solutions and services, and scanners. Every year, the company delivered 100 million products to 120 countries around the world; it shipped one printer and 1.? PCs every second out of its warehouses. As of June 2019, HP's share of global PC shipments stood at 23.6 per cent16 and its share of global printer shipments at 26.6 per cent.\" The company distributed its products through partners such as retailers, who sold the products to the public through the retailers' physical or Internet stores; resellers, who sold to targeted customer groups with the resellers' value-added products or services; distribution partners, who supplied the products to resellers; and system integrators, who provided various levels of services downstream FORAY INTO 3D PRINTING In October 2013, as a strategic response to \"industry declines in some of our businesses,\"18 I-IP's executive team decided to leverage its established leadership in 2D printing and enter the 3D printing market. A year later, HP announced that it would produce a 3D printer that would be 10 times faster and 50 per cent cheaper than any existing system in the market. An increase in the company's research and development (R&D) expenses evidenced the early-stage investment HP made in the new business segment: from $1,191 million in 2015, the R&D expenses increased to $1,209 million in 2016. The company had said at the time that the 2 per cent increase in R&D outlay was \"primarily due to incremental investments in A3 printers and 3D printing.\"19 An A3 printer could handle large printing projects with multiple page sizes. It cost more than an A4 printer, which could only handle regular letter-sized (A4) documents. HP introduced MJF, its rst additive manufacturing technology, in December 2016. The knowledge drew on I-IP's expertise in microuidics and the precise deposition of inks employed in its industry-leading 2D printing technology?\" Designed for producing plastic parts, MJF deployed a powder bed process that was more in common with inkjet printing than with the point-by-point laser-based powder fusion systems prevalent in 3D printing at the time. MJF technology was critical for eventually achieving the desired quality of parts, cost reductions, and speed. The long-term plan was to target large-scale manufacturing environments, help enterprises accelerate their product design and production, create more exible manufacturing and supply chains for the enterprises, and generally enhance efciencies across the manufacturing lifecycle. HP sought to provide end-to-end solutions that would help customers increase innovation, accelerate time to market, reduce costs, and eliminate waste.21 MJF devices initially included two models: the 3200 and the 4200. The models differed in their print speeds and layer thicknesses. Targeting different application segments, the units were priced at around $270,000 each HP on HP During product development, HP learned that 60 plastic parts that formed the innards of an MJF platform could be printed by a 3D printer. The nding set in motion an internal initiative called \"HP on HP.\"22 The company went deep on the technology by increasing the number of 3D-printable parts to more than 140; it also went wide by implementing the technology across the broader HP businesses and their supply chains. It helped that HP had \"one of the biggest plastic supply chains in the world.\"23 Around 30 per cent of the output of the HP on HP project comprised tools, jigs, xtures, guides, and grippers. In September 2018, HP produced a new version of its 3D printer, known as the MJF 5200. Priced at $399,000, the new printer incorporated learnings from the 4200 series by providing built-in redundancies, better sensors, wider material compatibility, and machine learning algorithms for preventive maintenance. The new series offered 30 per cent reduction in running costs, 40 per cent higher speeds, and 50 per cent lower cost per printed part. The MJF 5200 was more than a linear evolution; it was suited for mass production rather than prototyping. The launch of the MJF 5200 and the announcement of Metal Jet, a new technology for printing metal parts, coincided with HP looking outward to develop an ecosystem of partnerships. The company tied up with GKN Powder Metallurgy (GKN), a German rm and the largest producer of metal powder parts in the world. GKN was known for its depth in automotive and industrial value chains. HP also tied up with Parmatech Corporation, an American rm that held some of the rst patents around metal injection moulding and was known for its expertise in the medical devices value chains. HP had already tied up with Siemens AG for software support. In June 2019, HP inaugurated its 3D Printing and Digital Manufacturing Center of Excellence in Sant Cugat, just outside Barcelona in Spain (see Exhibit '7). The new 150,000-square-foot facility, housing about 100 industrial 3D printers, was home to the company's several R&D spaces for both the polymer MJF and the Metal Jet platforms, as well as the materials science labs. The centre also hosted co-development environments for working with partners and customers. Said to be the largest of its kind in the world, the centre brought together specialists of 60 nationalities in systems engineering, data intelligence, software, materials science, design, and digital manufacturing applications. Its objective was to not only drive HP's goal of disrupting mainstream manufacturing but also to take 3D printing to mass manufacturing. Evidence of HP's efforts with the latter was that while all of HP's global customers together produced 10 million parts on HP's 3D-printers in 2018, one customer alonethe Smile Direct Club, an American orthodontic products rmhad a plan to produce 20 million parts just in 2019.24 Business Model HP estimated the total addressable market for 3D printing to be about $500 billion over time.25 However, given that the total revenue of the top seven companies in the 3D printing industry was $7.3 billion in 2018, only 1.4 per cent of the projected market was being tapped. The market was clearly still in its infancy and HP was itself at the beginning of its desired revenue generation curve. According to an estimate, the company's 2018 revenue from 3D printing was $250 million.26 It would be several years before 3D printing would become a separate line item in HP's reporting of revenues by segment to shareholders. The traditional printer and PC segments of the company had a device-driven and one-time purchase model. An exception was the recurring purchases of ink in the company's printer business. In contrast, the 3D printing business was being monetized as a platform-driven model whereby HP would play a collaborative role in the 3D printing ecosystem. As an equipment manufacturer, HP had the opportunity to capture greater nancial value and, at the same time, likely greater strategic exibility. Nonetheless, HP seemed to be determined that, going forward, contractual arrangements and partnerships rather than device sales would be critical performance milestones in the company's 3D printing business.\" HP was exploring different business models in monetizing not only the hardware but also the software and services related to 3D printing. That led to 3D-as-a-Service (3DaaS) as a possible revenue stream. 3DaaS would have a strong component of service and support as part of the business model. It would provide \"automatic replenishment of HP 3D supplies, simplied tracking of billing and usage, and reliable remote and on-site support services.\" The company viewed the 3DaaS model as \"ideal for customers looking to accelerate product life cycles with optimized in-house rapid prototyping and nal part production.\"28 The company's 3D printers were generating data about everything going on in their ecosystem, leading to a long-term opportunity to provide services around the intelligence HP was gathering from the printers. The launch of the 5200 series had demonstrated that HP was indeed in the data business: each print job produced 4 terabytes (TB) of data that could be analyzed and used in advancing the business model.\" ISSUES In contrast to its peers, the technology at HP had progressed beyond prototyping, rapid tooling, trinkets, and toys; the technology was geared to meet a diverse mass market. However, the overall market appeared to be heavily fragmented and in different stages of readiness. Promoting Technology Awareness among Potential Users HP's entry into 3D printing in 2016 had been perceived by the existing players in 3D printing not as a competitive but as an enabling move that would benet overall industry development.30 By April 2020, the ongoing COVlD-l9 pandemic had proven itself a catalyst for additive manufacturing. The ght against the pandemic was generating use-cases of 3D printing in the production of components for the manufacture of ventilators and respirators, which were in exponential demand by health care providers. The medical devices industry was known for strict standards and was also known, for that reason, to be slow to change. But the pandemic seemed to have given all key players momentum in readiness to accept new and innovative ways of production. After the pandemic, however, Pastor would still be facing the larger issue of lack of demand om customers for integrating 3D printing into their supply chainsan issue that owed directly from lack of awareness. There were two things, he believed, that had to be in place for the awareness to set in: the \"push factor,\" as Pastor saw it, represented by the agility and exibility that 3D printing could add to manufactming, and the \"pull factor,\" represented by the efciency and resilience that 3D printing brought to supplydemand matching. Economic benets would be primary for a potential customer. Using 3D printing to create a part at a lower cost than could be achieved with conventional manufacturing would be a straight win. It was only after selling 3D printing solutions based on these economic benets that potential client conversations about even greater benetssuch as lighter weights for parts, assembly consolidation, and design freedom would happen. An investment of $400,000 in a 3D printer was a major expense for even large companies. Currently, HP was using different routes to promote technology awareness among potential users. One example was the 3DaaS service, wherein a customer would not need to buy the printer but only pay for usage. This monthly payment provided the ability to produce up to a maximum level of parts (usually determined as the total weight of the parts) and included the needed materials, uids, and services to produce them, with no commitment on permeance of the service. Such a subscription model would not necessarily help I-IP scale its own printer production as much as desired, but it would allow potential buyers to try the new technology, become familiar with it, and accelerate adoption with designers and engineers. For illustrative purposes, usage up to 1,000 grams of parts could be considered to cost approximately $1,500 per month. Another route to advance technology awareness was the active promotion of the concept of 3D hubs. A 3D hub was a physical place outside HP where customers could see how a production line used 3D printing. The hub was both technology-agnostic and brand-agnostic in the sense that it featured not just HP but all 3D printer vendors. Some hubs were also designed as training facilities especially for small and medium-sized businesses. Hubs existed in certain states of the United States and in other countries, such as Germany and Spain, but the view was that more hubs were needed at the regional level to promote the use of Industry 4.0 technologies.\" Scaling Up Manufacturing HP was taking four routes to scale up manufacturing of 3D printers. Focus on Core Competence HP was strategically prioritizing 3D printer manufacturing and sales as much as possible. The 3DaaS model came with an entire suite of additional services, from design to assembly of printed and non-printed parts. However, rather than independently providing end-to-end 3D printing solutions to its customers, HP was developing relationships with leading companies with expertise in each of those specialities. The strategy was based on the belief that the 3D printing business would be easier to scale if HP were to stick to core activities and leave the rest to partners for whom 3D printing adj acencies were core functions. One of those strategic partnerships was with Siemens AG, which focused on software solutions. Others were with GKN, Materialise NV, and other companies for parts service. Focus on Applications 3D technology had already progressed to a level where the conversations with customers had escalated from \"What is the material?\" to \"What is the application?\" Application requirements were beginning to serve as the starting point for material selection. For example, the launch of Ultrasint TPUOl powder by BASF SE for HP's MJF platform was triggered by customer demand for a material that could be used for production of parts requiring shock absorption and exibility. User industries included sports protection equipment, footwear, and orthopaedics. HP believed that it would be easier to let applications lead the way for potential growth opportunities. Indeed, the choice of steel for the Metal Jet platform was itself triggered by steel having more applications across industries than any other metal. Focus on Verticals HP thought it was necessary to let the choice of verticals lead the way to scale. The rst lter was whether the vertical itself would be amenable to scale. The second lter would be whether the chosen vertical would enable HP to leverage the assets it had already developed. A related issue would be whether an application in one vertical (like medical devices) would also be replicable at another vertical (like packaging). Other lters such as return on investment would then become relevant. A vertical-led approach would also gradually let HP go further into each vertical as part of developing further potential competitive advantages. A major challenge that all companies faced was nding people with the right vertical expertise who could speak the same language as the customer. HP had an edge among its competitors in the 3D printer business due to its existing and long-standing traditional printer business. The company also featured regularly in Fortune's annual listing of best workplaces. It ranked 24th in the 2019 listing,32 which enticed applicants with good credentials. Treat 3D Printing as Means to an End, Not an End in Itself HP's investment was made to scale up unit sales, but the investment was not as much about the 3D printer as a product as it was about the potential enabling benets 3D printing provided for HP's customers. 3D printing offered a production technology that was compatible with digital or hybrid workows. It was thus a critical element of digital manufacturing. HP's ultimate objective was to help customers in their digital transformation. In its bid to scale the 3D printing business, HP was looking beyond itself. There was also the matter of leveraging the customer data that would be generated by 3D printing. Capturing, storing, and analyzing the data would help HP promote the goals of mass customization, distributed manufacturing, and on-demand production, reinforcing, in turn, HP's bid to scale up and to accelerate and diversify its own 3D printer development. Reducing Long Adoption Cycles in User Industries Industries using a platform manufacturing strategy had long adoption cycles. Companies participating in platform-based value chains beneted from the unique skills each company brought. The strategy was common in industries such as automotive, aerospace, and some medical devices. Cars, for example, had platforms lasting between ve and seven years. Each time a platform reached the end of its life cycle and came up for renewal, opportunities were opened for new players and new technologies. During the intervening period, the platforms would not be open to fresh investments. The platform had to run its course before any major disruptive changes could be made. Pastor knew that platform-based industries had the greatest potential for deploying 3D printing in their operations; they were also most welcoming of new technologies like 3D printing. One of the challenges that Pastor was facing with reducing adoption cycles was synchronizing (or synchz'ng, as it was lmown in the company). Identifying the point when I-IP could intervene with its investment proposal for a large manufacturing platform client was not easy given variables such as the number of manufacturing locations, products, and platforms, and the differing stages of platform life cycles. The intervention had to be timed at least a year or two ahead of the end of the cycle of a platform. It also meant making investments that would not start giving a return for three to four years. Pastor was dealing with the challenge through a portfolio management model; he did not want HP to put all of its efforts towards one opportunity. Pastor believed it was better to spread risks by taking a multi- client, multi-platform, and multi-year approach. However, such an approach also came with compromises in speed and complexity of sales. The toughest challenge Pastor faced, however, was in breaking \"corporate inertia\" among industrial clients. Adopting a new technology like 3D printing required a behavioural change among the key decision makers in a large company, most of whom generally had long tenures. The decision makers had a traditional manufacturing mindset based on scalable efciencies rather than scalable agility. Taking all these reections into account, Pastor called a leadership meeting to develop a plan to (1) rapidly and widely increase technology awareness among current and potential industrial customers, and (2) reduce the technology adoption cycles in manufacturing industries. Finally, Pastor also knew that increasing the adoption of 3D printing technology was only one of the objectives of the business. A more important consideration was HP's share of value capture. Usually, after a new application was developed, 7090 per cent of the margin created was captured by the company that would be 3D printing the parts and not by HP as the technology provider. EXHIBIT 1: REVENUE TREND FOR PUBLICLY LISTED 3D COMPANIES (IN US$ MILLIONS) Rank Company Country 2018 2017 2016 2015 3D Systems Corp United States 588 646 633 666 Stratasys Ltd United States/Israel 663 668 673 696 Proto Labs Inc. United States 446 264 298 264 NO UA W N- Materialise NV Belgium 218 161 127 113 SLM Solutions Group AG Germany 85 93 89 73 ExOne Company United States 65 58 49 40 voxeljet AG Germany 31 26 25 27 Total of 7 Companies 2, 196 1,919 1,894 1,879 Industry Total 9,795 7,335 6,064 5,615 Source: "3D Printing Industry Snapshot," J.P. Morgan Equity Research Report, April 1, 2019. EXHIBIT 2: TRADITIONAL MANUFACTURING VERSUS 3D PRINTING-VOLUME VERSUS COST Cost per unit 3D printing Traditional manufacturing Output Source: Benjamin Grynol, Disruptive Manufacturing: The Effects of 3D Printing (Canada: Deloitte LLP, n.d.), 6, https://www2.deloitte.com/content/dam/Deloitte/ca/Documents/insights-and-issues/ca-en-insights-issues-disruptive- manufacturing.pdf. Used with permission.EXHIBIT 3: LEADING HOLDERS OF 3D PRINTING PATENTS Company Country No. of 3D Patents General Electric Company United States 2,516 HP Inc. United States 2,285 United Technologies Corp. United States 1,855 Siemens AG Germany 1,529 3M Company United States 1, 145 3D Systems Corp United States 1,055 Harvard University United States 984 Boeing Co. United Kingdom 933 Stratasys Inc. United States/Israel 769 Xerox Corp. United States 679 Source: "Leading Countries for 3D Printing Patent Applications 2019," Statista, accessed October 19, 2020. EXHIBIT 4: 3D PATENT APPLICATIONS FILED IN 2019, BY COUNTRY Country Number of Applications Filed United States 44,177 China 18,838 Europe 15,049 Germany 10, 199 Great Britain 8,719 Spain 6,744 Austria 6,586 Switzerland 6,579 Sweden 6,557 Denmark 6,456 Portugal 6,383 Source: "Leading Countries for 3D Printing Patent Applications 2019," Statista, accessed October 19, 2020. EXHIBIT 5: MARKET SHARE OF 3D PRINTING, JULY 2018, BY COUNTRY Country Market Share (%) United States 38.1 United Kingdom 15.7 Netherlands 6.7 Germany 6.3 Canada 5.7 Australia 5.7 Singapore 3.9 France 2.5 Italy 1.4 India 1.4 Total 37.4 Source: "3D Printing & Additive Manufacturing Worldwide," Statista, accessed October 19, 2020.EXHIBIT 6: HP INC.'S FINANCIALS Consolidated Income Statement (in US$ millions) Year Ending October 2019 2018 2017 2016 2015 2014 Net Revenue 58,756 58,472 52,056 48,238 51,463 56,651 Cost of Goods Sold 47,586 47,803 42,478 39,240 41,524 45,431 Research and Development 1,499 1,404 1,190 1,209 1, 191 1,298 Selling, General, and Administration 5,368 5,099 4,532 3,833 4,720 5,361 Restructuring Charges 275 132 362 205 63 176 Acquisition Costs 35 123 125 Amortization 116 80 16 102 129 Defined Benefits Charges 179 (57) Total Costs and Expenses 54,879 54,641 48.688 44,689 47,543 52,395 Earnings from Operations 3,877 3,831 3,368 3,549 3,920 4,256 Interest Charges (1,354) (818) (92) 212 388) (393) Earnings before Taxes 2,523 3,013 3,276 3,761 3,532 3,863 Benefit (Provision) for Taxes 629 2,314 (750) (1,095) 186 (939) Net Earnings 3,152 5,327 2,526 2,496 4,554 5,013 Revenue by Business Segment (in US$ millions) Year Ending October 2019 2018 2017 2016 2015 2014 Notebooks 22,928 22,547 19,782 16,982 17,271 17,540 Desktops 12,046 11,567 10,298 9,956 10,941 13, 197 Workstations 2,389 2,246 2,042 1,870 2,018 2,218 Other 1,331 1,301 1, 199 1,179 1,290 1,432 Subtotal Personal Systems 38,694 37,661 33,321 29,987 31,520 34,387 Supplies 12,921 13,575 12,524 11,875 13,979 14,917 Commercial Hardware 4,612 4,514 3,792 5,131 5,466 6,035 Consumer Hardware 2,533 2,716 2,412 1,254 1,787 2,259 Subtotal Printing 20,066 20,805 18,728 18,260 21,232 23,211 Others (4) (9) (1,289) (947) Total Revenue 58,762 58,472 52,057 48,238 51,463 56,651 Source: Company documents

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!