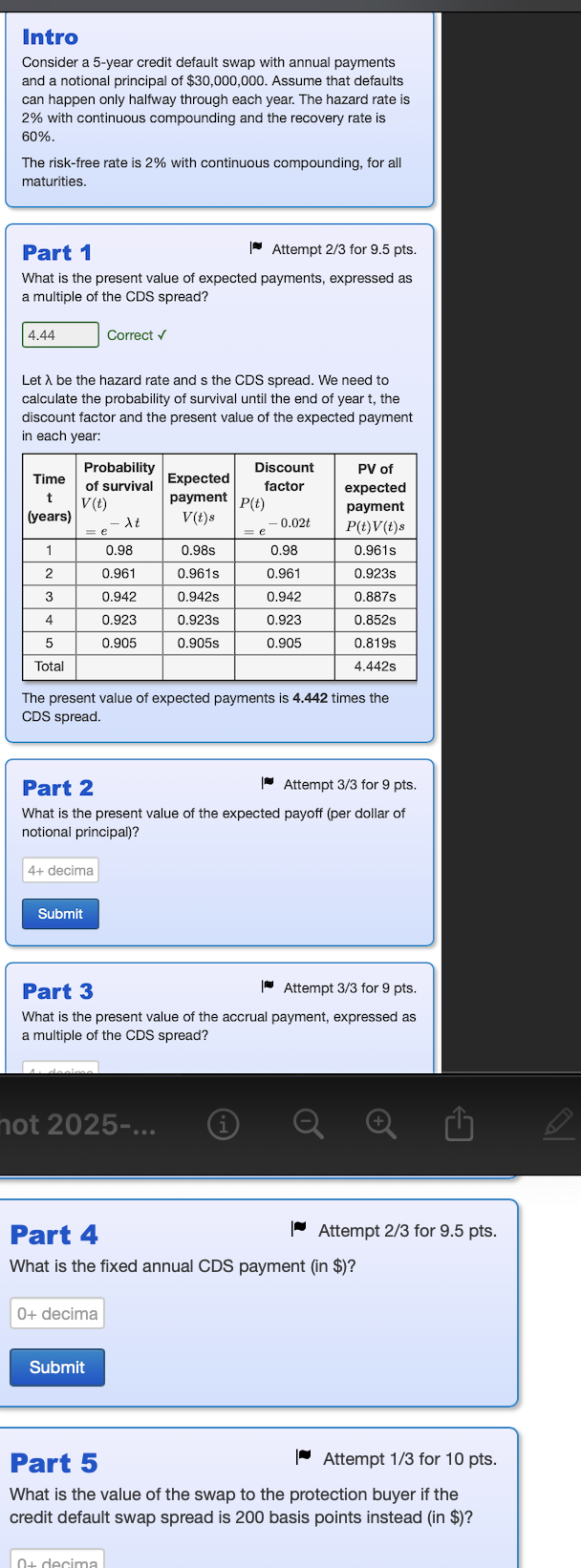

Question: Intro Consider a 5 - year credit default swap with annual payments and a notional principal of ( $ 3 0 , 0

Intro

Consider a year credit default swap with annual payments and a notional principal of $ Assume that defaults can happen only halfway through each year. The hazard rate is with continuous compounding and the recovery rate is

The riskfree rate is with continuous compounding, for all maturities.

Part

Attempt for pts

What is the present value of expected payments, expressed as a multiple of the CDS spread? Correct checkmark

Let lambda be the hazard rate and s the CDS spread. We need to calculate the probability of survival until the end of year t the discount factor and the present value of the expected payment in each year:Time t yearsProbability of survival Vtelambda tExpected payment Vt s Discount factor Pte tPV of expected payment Pt Vt s

The present value of expected payments is times the CDS spread.

Part

Attempt for pts

What is the present value of the expected payoff per dollar of notional principal

What is the present value of the accrual payment, expressed as a multiple of the CDS spread?

Part

Attempt for pts

What is the fixed annual CDS payment in $

What is the value of the swap to the protection buyer if the credit default swap spread is basis points instead in $

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock