Question: ints Johnson & Johnson, U.S.Alternative External Borrowing Interest Rates Fixed: 8% Floating: SOFR+55 BP Designing a swap Citicorp, U.S. This is YOU! AppleAlternative External

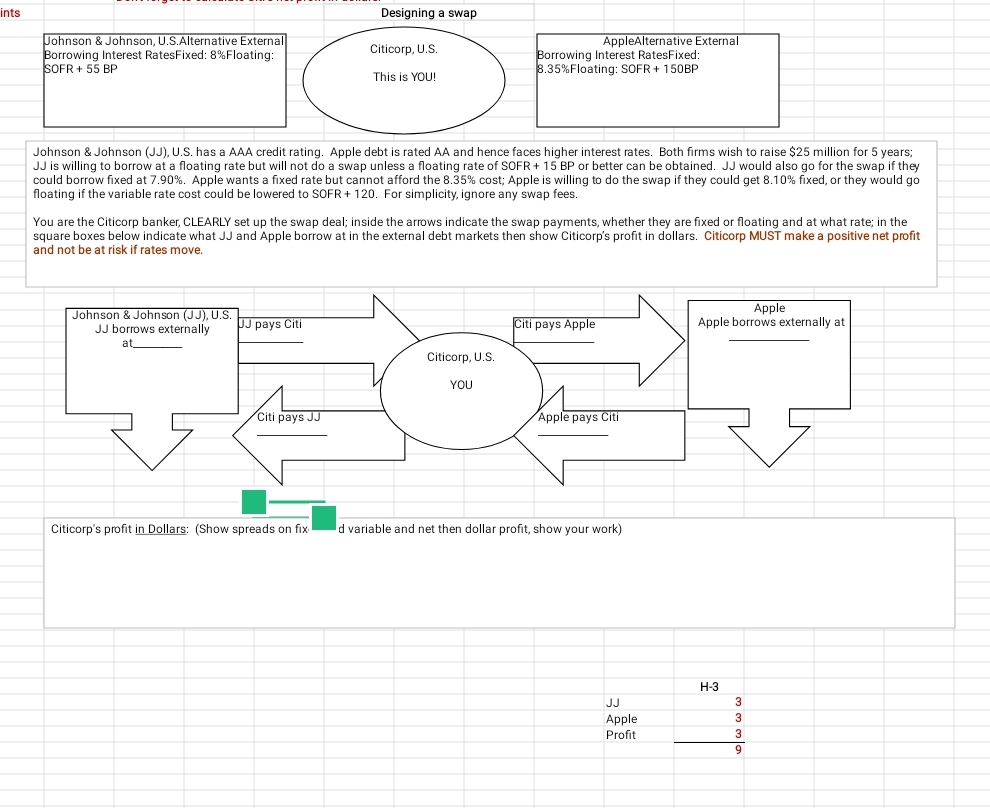

ints Johnson & Johnson, U.S.Alternative External Borrowing Interest Rates Fixed: 8% Floating: SOFR+55 BP Designing a swap Citicorp, U.S. This is YOU! AppleAlternative External Borrowing Interest RatesFixed: 8.35% Floating : SOFR+ 150BP Johnson & Johnson (JJ), U.S. has a AAA credit rating. Apple debt is rated AA and hence faces higher interest rates. Both firms wish to raise $25 million for 5 years; JJ is willing to borrow at a floating rate but will not do a swap unless a floating rate of SOFR+ 15 BP or better can be obtained. JJ would also go for the swap if they could borrow fixed at 7.90%. Apple wants a fixed rate but cannot afford the 8.35% cost; Apple is willing to do the swap if they could get 8.10% fixed, or they would go floating if the variable rate cost could be lowered to SOFR+ 120. For simplicity, ignore any swap fees. You are the Citicorp banker, CLEARLY set up the swap deal; inside the arrows indicate the swap payments, whether they are fixed or floating and at what rate; in the square boxes below indicate what JJ and Apple borrow at in the external debt markets then show Citicorp's profit in dollars. Citicorp MUST make a positive net profit and not be at risk if rates move. Johnson & Johnson (JJ), U.S. Apple JJ borrows externally JJ pays Citi Citi pays Apple Apple borrows externally at at Citicorp, U.S. YOU Citi pays JJ Apple pays Citi Citicorp's profit in Dollars: (Show spreads on fix! d variable and net then dollar profit, show your work) H-3 JJ 3 Apple Profit 3 9 mmm

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts