Question: Investments - Bodie, Kane and Marcus. Correlation between A stdev and market Beta 0.8 correlation between A and B 0 Stocks 1.2 1.83 12% 14%

Investments - Bodie, Kane and Marcus.

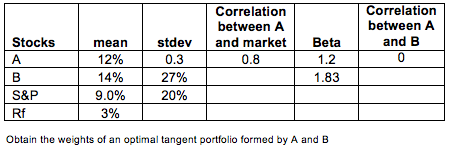

Correlation between A stdev and market Beta 0.8 correlation between A and B 0 Stocks 1.2 1.83 12% 14% 9.0% 396 | 27% 20% S&P Rf | | | Obtain the weights of an optimal tangent portfolio formed by A and B

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock