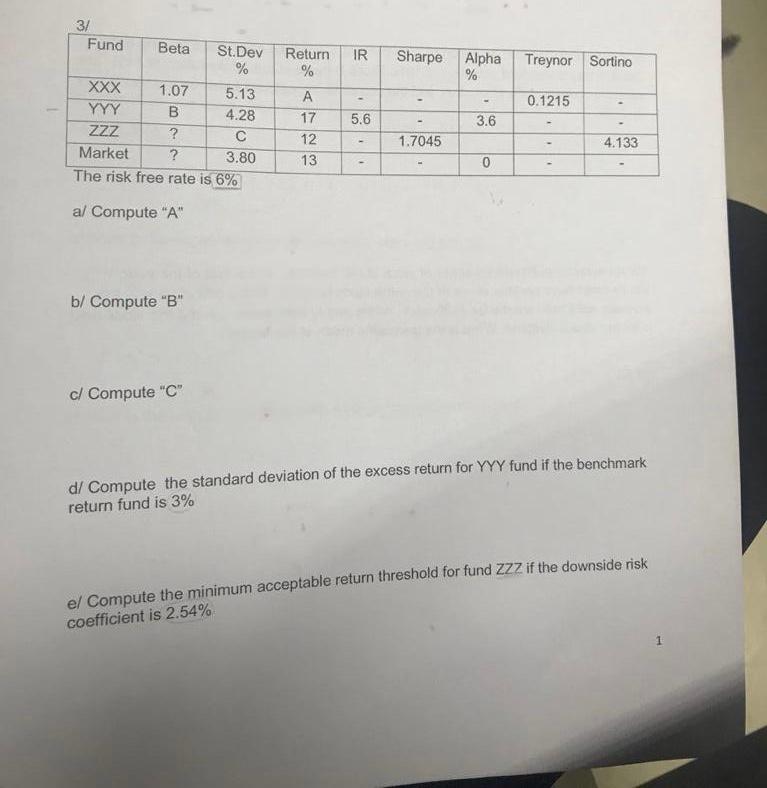

Question: IR Return % Sharpe Alpha % Treynor Sortino 3/ Fund Beta St.Dev % XXX 1.07 5.13 YYY B 4.28 ZZZ ? Market ? 3.80 The

IR Return % Sharpe Alpha % Treynor Sortino 3/ Fund Beta St.Dev % XXX 1.07 5.13 YYY B 4.28 ZZZ ? Market ? 3.80 The risk free rate is 6% 0.1215 5.6 3.6 A 17 12 13 1.7045 4.133 0 al Compute "A" b/ Compute "B" c/ Compute "C" d/ Compute the standard deviation of the excess return for YYY fund if the benchmark return fund is 3% el Compute the minimum acceptable return threshold for fund ZZZ if the downside risk coefficient is 2.54% 1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock