Is Apple's explanation for why it adopted the new rules retrospectively clear (exhibit 1)? is it valid?

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

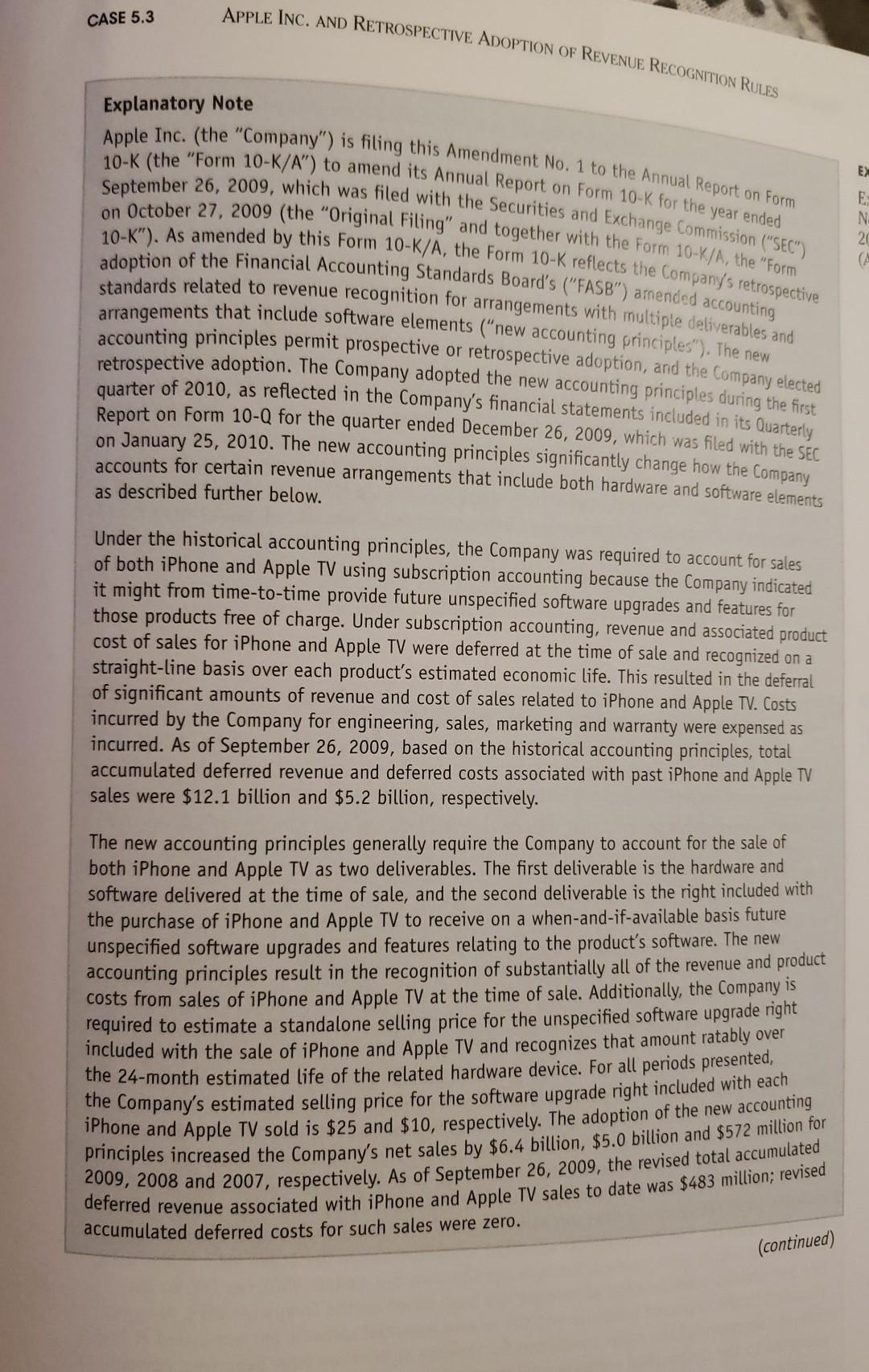

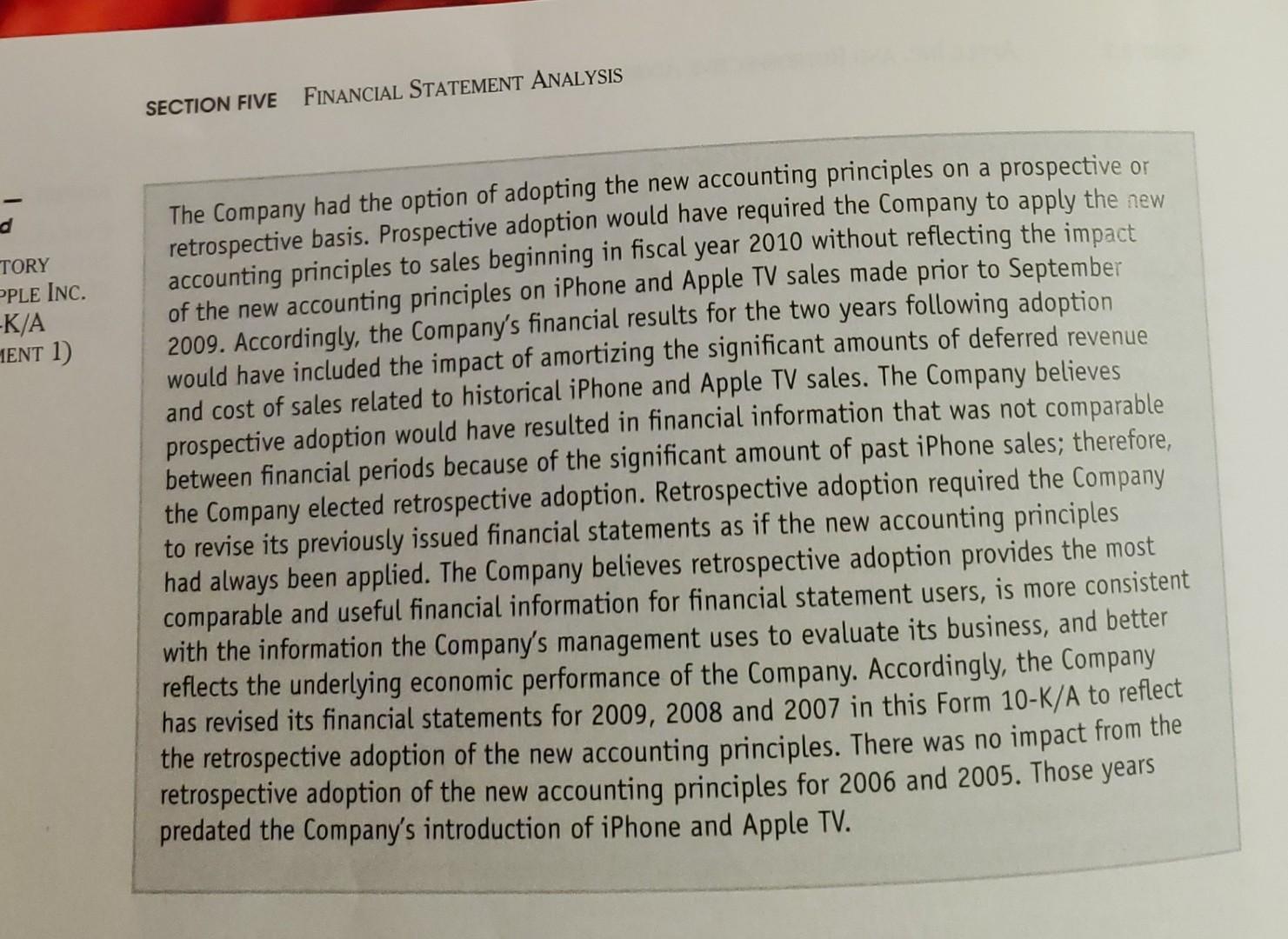

arrangements that include software elements ("new accounting principles"). The new standards related to revenue recognition for arrangements with multiple deliverables and adoption of the Financial Accounting Standards Board's ("FASB") amended accounting 10-K"). As amended by this Form 10-K/A, the Form 10-K reflects the Company's retrospective on October 27, 2009 (the "Original Filing" and together with the Form 10-K/A, the "Form 10-K (the "Form 10-K/A") to amend its Annual Report on Form 10-K for the year ended September 26, 2009, which was filed with the Securities and Exchange Commission ("SEC") Apple Inc. (the "Company") is filing this Amendment No. 1 to the Annual Report on Form APPLE INC. AND RETROSPECTIVE ADOPTION OF REVENUE RECOGNITION RULES CASE 5.3 Explanatory Note E E: No (A accounting principles permit prospective or retrospective adoption, and the Company elected retrospective adoption. The Company adopted the new accounting principles during the first quarter of 2010, as reflected in the Company's financial statements included in its Ouarterly Report on Form 10-Q for the quarter ended December 26, 2009, which was filed with the SEC on January 25, 2010. The new accounting principles significantly change how the Company accounts for certain revenue arrangements that include both hardware and software elements as described further below. Under the historical accounting principles, the Company was required to account for sales of both iPhone and Apple TV using subscription accounting because the Company indicated it might from time-to-time provide future unspecified software upgrades and features for those products free of charge. Under subscription accounting, revenue and associated product cost of sales for iPhone and Apple TV were deferred at the time of sale and recognized on a straight-line basis over each product's estimated economic life. This resulted in the deferral of significant amounts of revenue and cost of sales related to iPhone and Apple TV. Costs incurred by the Company for engineering, sales, marketing and warranty were expensed as incurred. As of September 26, 2009, based on the historical accounting principles, total accumulated deferred revenue and deferred costs associated with past iPhone and Apple TV sales were $12.1 billion and $5.2 billion, respectively. The new accounting principles generally require the Company to account for the sale of both iPhone and Apple TV as two deliverables. The first deliverable is the hardware and software delivered at the time of sale, and the second deliverable is the right included with the purchase of iPhone and Apple TV to receive on a when-and-if-available basis future unspecified software upgrades and features relating to the product's software. The new accounting principles result in the recognition of substantially all of the revenue and product costs from sales of iPhone and Apple TV at the time of sale. Additionally, the Company is required to estimate a standalone selling price for the unspecified software upgrade right included with the sale of iPhone and Apple TV and recognizes that amount ratably over the 24-month estimated life of the related hardware device. For all periods presented, the Company's estimated selling price for the software upgrade right included with each TPhone and Apple TV sold is $25 and $10, respectively. The adoption of the new accounting principles increased the Company's net sales by $6.4 billion, $5.0 billion and $572 million for de, 2008 and 2007, respectively. As of September 26, 2009, the revised total accumulated dererred revenue associated with iPhone and Apple TV sales to date was $483 million; revised accumulated deferred costs for such sales were zero. (continued) arrangements that include software elements ("new accounting principles"). The new standards related to revenue recognition for arrangements with multiple deliverables and adoption of the Financial Accounting Standards Board's ("FASB") amended accounting 10-K"). As amended by this Form 10-K/A, the Form 10-K reflects the Company's retrospective on October 27, 2009 (the "Original Filing" and together with the Form 10-K/A, the "Form 10-K (the "Form 10-K/A") to amend its Annual Report on Form 10-K for the year ended September 26, 2009, which was filed with the Securities and Exchange Commission ("SEC") Apple Inc. (the "Company") is filing this Amendment No. 1 to the Annual Report on Form APPLE INC. AND RETROSPECTIVE ADOPTION OF REVENUE RECOGNITION RULES CASE 5.3 Explanatory Note E E: No (A accounting principles permit prospective or retrospective adoption, and the Company elected retrospective adoption. The Company adopted the new accounting principles during the first quarter of 2010, as reflected in the Company's financial statements included in its Ouarterly Report on Form 10-Q for the quarter ended December 26, 2009, which was filed with the SEC on January 25, 2010. The new accounting principles significantly change how the Company accounts for certain revenue arrangements that include both hardware and software elements as described further below. Under the historical accounting principles, the Company was required to account for sales of both iPhone and Apple TV using subscription accounting because the Company indicated it might from time-to-time provide future unspecified software upgrades and features for those products free of charge. Under subscription accounting, revenue and associated product cost of sales for iPhone and Apple TV were deferred at the time of sale and recognized on a straight-line basis over each product's estimated economic life. This resulted in the deferral of significant amounts of revenue and cost of sales related to iPhone and Apple TV. Costs incurred by the Company for engineering, sales, marketing and warranty were expensed as incurred. As of September 26, 2009, based on the historical accounting principles, total accumulated deferred revenue and deferred costs associated with past iPhone and Apple TV sales were $12.1 billion and $5.2 billion, respectively. The new accounting principles generally require the Company to account for the sale of both iPhone and Apple TV as two deliverables. The first deliverable is the hardware and software delivered at the time of sale, and the second deliverable is the right included with the purchase of iPhone and Apple TV to receive on a when-and-if-available basis future unspecified software upgrades and features relating to the product's software. The new accounting principles result in the recognition of substantially all of the revenue and product costs from sales of iPhone and Apple TV at the time of sale. Additionally, the Company is required to estimate a standalone selling price for the unspecified software upgrade right included with the sale of iPhone and Apple TV and recognizes that amount ratably over the 24-month estimated life of the related hardware device. For all periods presented, the Company's estimated selling price for the software upgrade right included with each TPhone and Apple TV sold is $25 and $10, respectively. The adoption of the new accounting principles increased the Company's net sales by $6.4 billion, $5.0 billion and $572 million for de, 2008 and 2007, respectively. As of September 26, 2009, the revised total accumulated dererred revenue associated with iPhone and Apple TV sales to date was $483 million; revised accumulated deferred costs for such sales were zero. (continued)

Expert Answer:

Answer rating: 100% (QA)

It was totally good and valid for Apple to begin to account for its iPhone sales under the new rules ... View the full answer

Related Book For

Posted Date:

Students also viewed these economics questions

-

1. Offer three reasons with full explanation for why it is important for companies to keep a fair portion of their overall asset balance in liquid assets. 2. What are some considerations for...

-

1. Offer three reasons with full explanation for why it is important for companies to keep a fair portion of their overall asset balance in liquid assets. 2. What are some considerations for...

-

Provide an explanation for why it is possible that average SATs that are declining might be consistent with the assertion that more people are prepared for college than ever before?

-

The accounting records for The Skate Shed, Inc., reflected the following amounts at the end of January 2018: Prepare The Skate Shed?s multistep income statement for the fiscal year ended January 31,...

-

Use what you know about Starbucks and apply the VRIO/VRIN approach to evaluate Starbucks, as you know it. Use the five forces model to evaluate Starbucks. Is the five forces model different from the...

-

The T accounts for Dividends Payable, Common Stock, Paid-in Capital in Excess of Par Value, and Retained Earnings for Mario Corporation at the end of 2013 follow. Compute the amounts to be included...

-

Information taken from Applied Technology's comparative balance sheet is provided in the Working Papers. Your instructor will guide you through the following problem. 1. Calculate the following...

-

Calculate the contribution to total performance from currency, country, and stock selection for the manager in the example below. All exchange rates are expressed as units of foreign currency that...

-

Poverty rates are normally distributed across counties in the United States. The US Department of Poverty states that the average poverty rate in counties across America is 16%. You believe that this...

-

Mr. Pawan Garg, a wealthy businessman, has approached you for professional advice on investment. He has a surplus of Rs. 20 lakhs which he wishes to invest in share market. Being risk averse by...

-

A student Jane going for a run follows the path shown in Figure where the distances AB = 100 m and BC = 200 m. Assuming Jane was running at a constant speed of 5.00 m/s, what is Jane's average...

-

Q.9 Unemployment and monetary policy (6 points) A country is at the full-employment (i.e.. zero cyclical unemployment) level. Suppose the central bank tries to reduce unemployment below the natural...

-

Give the domain in interval notation. 2x+7x h(x) = -8-3x Domain:

-

Oakwood Financial Inc. was organized on February 28. Projected selling and administrative expenses for each of the first three months of operations are as follows: March April May $175,000 161,000...

-

Consider mobile integrated health care (MIH) or community paramedic (CP) programs you have read about or are familiar with. Do you think this is a new scope for emergency medical services (EMS)...

-

Dodge company has been a very reliable automobile that has been in the market it has had ups and downs. Has increased its market sales up to 18% Has been a well-known vehicle in the past couple of...

-

3. The Gem (TG) is an organic juice bar located in Philadelphia. TG is particularly famous for its protein-smoothies and currently has two smoothie-makers (each is operated by a single employee)....

-

Imagine a sound wave with a frequency of 1.10 kHz propagating with a speed of 330 m/s. Determine the phase difference in radians between any two points on the wave separated by 10.0 cm.

-

Since its inception, the portion of earnings that have been subject to the Social Security tax has a. Remained roughly intact. b. Increased substantially. c. Decreased slightly. d. Decreased...

-

Using a poverty line of $12,500, under the current system of calculating the poverty rate, which of the following people are not considered to be in poverty and probably ought to be? a. A rural...

-

Explain why an economist would focus on real GDP rather than nominal GDP.

-

As the amount of a variable input is increased, the amount of other fixed inputs being held constant, a point will ultimately be reached beyond which marginal product will decline. This point is...

-

Fixed costs are costs that _________ with the level of output.

-

Average total cost equals _________ divided by the _________ produced.

Study smarter with the SolutionInn App