Question: Issue date: First coupon date: Maturity date: Settlement date: Last coupon date: Next coupon date: Coupon rate: Yield to maturity: 3/15/12 9/15/12 3/15/42 6/1/16 3/15/16

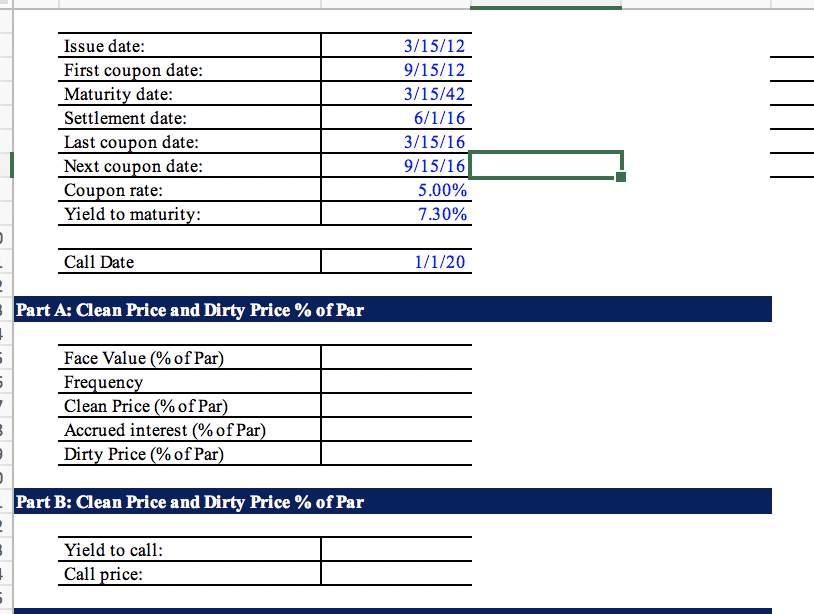

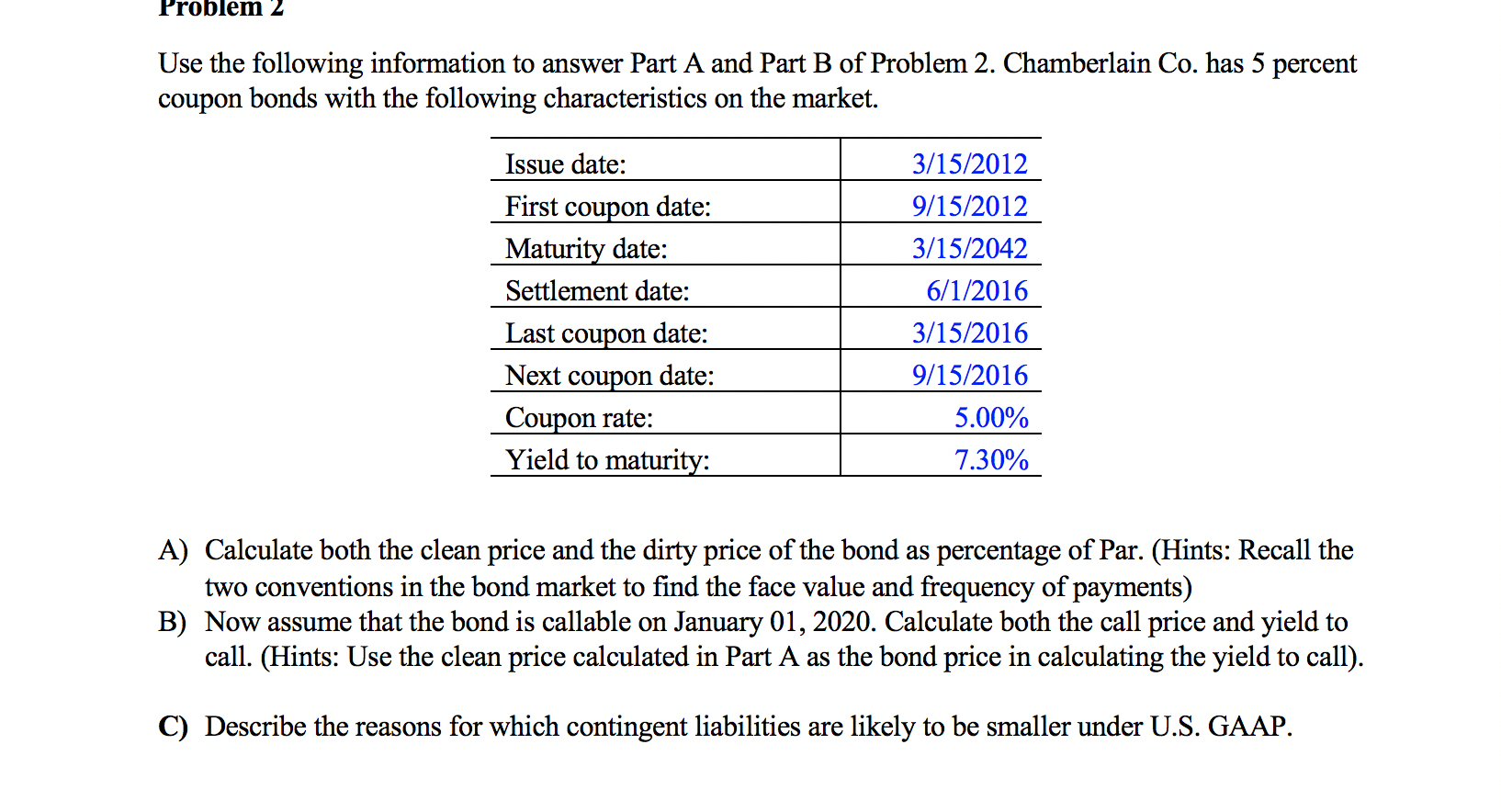

Issue date: First coupon date: Maturity date: Settlement date: Last coupon date: Next coupon date: Coupon rate: Yield to maturity: 3/15/12 9/15/12 3/15/42 6/1/16 3/15/16 9/15/16 5.00% 7.30% Call Date 1/1/20 Part A: Clean Price and Dirty Price % of Par 1 5 5 Face Value (%of Par) Frequency Clean Price (% of Par) Accrued interest (% of Par) Dirty Price (%of Par) 3 Part B: Clean Price and Dirty Price % of Par . Yield to call: Call price: Problem 2 Use the following information to answer Part A and Part B of Problem 2. Chamberlain Co. has 5 percent coupon bonds with the following characteristics on the market. Issue date: First coupon date: Maturity date: Settlement date: Last coupon date: Next coupon date: Coupon rate: Yield to maturity: 3/15/2012 9/15/2012 3/15/2042 6/1/2016 3/15/2016 9/15/2016 5.00% 7.30% A) Calculate both the clean price and the dirty price of the bond as percentage of Par. (Hints: Recall the two conventions in the bond market to find the face value and frequency of payments) B) Now assume that the bond is callable on January 01, 2020. Calculate both the call price and yield to call. (Hints: Use the clean price calculated in Part A as the bond price in calculating the yield to call). C) Describe the reasons for which contingent liabilities are likely to be smaller under U.S. GAAP. Issue date: First coupon date: Maturity date: Settlement date: Last coupon date: Next coupon date: Coupon rate: Yield to maturity: 3/15/12 9/15/12 3/15/42 6/1/16 3/15/16 9/15/16 5.00% 7.30% Call Date 1/1/20 Part A: Clean Price and Dirty Price % of Par 1 5 5 Face Value (%of Par) Frequency Clean Price (% of Par) Accrued interest (% of Par) Dirty Price (%of Par) 3 Part B: Clean Price and Dirty Price % of Par . Yield to call: Call price: Problem 2 Use the following information to answer Part A and Part B of Problem 2. Chamberlain Co. has 5 percent coupon bonds with the following characteristics on the market. Issue date: First coupon date: Maturity date: Settlement date: Last coupon date: Next coupon date: Coupon rate: Yield to maturity: 3/15/2012 9/15/2012 3/15/2042 6/1/2016 3/15/2016 9/15/2016 5.00% 7.30% A) Calculate both the clean price and the dirty price of the bond as percentage of Par. (Hints: Recall the two conventions in the bond market to find the face value and frequency of payments) B) Now assume that the bond is callable on January 01, 2020. Calculate both the call price and yield to call. (Hints: Use the clean price calculated in Part A as the bond price in calculating the yield to call). C) Describe the reasons for which contingent liabilities are likely to be smaller under U.S. GAAP

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts