Question: (Issue, Rule, Analysis and Conclusion (IRAC)) Issue: What is the question that the court had to decide (such as, are certain particular expenses deductible, is

(Issue, Rule, Analysis and Conclusion (IRAC)) Issue: What is the question that the court had to decide (such as, are certain particular expenses deductible, is certain income taxable, or whatever is in dispute. Be as precise as possible.

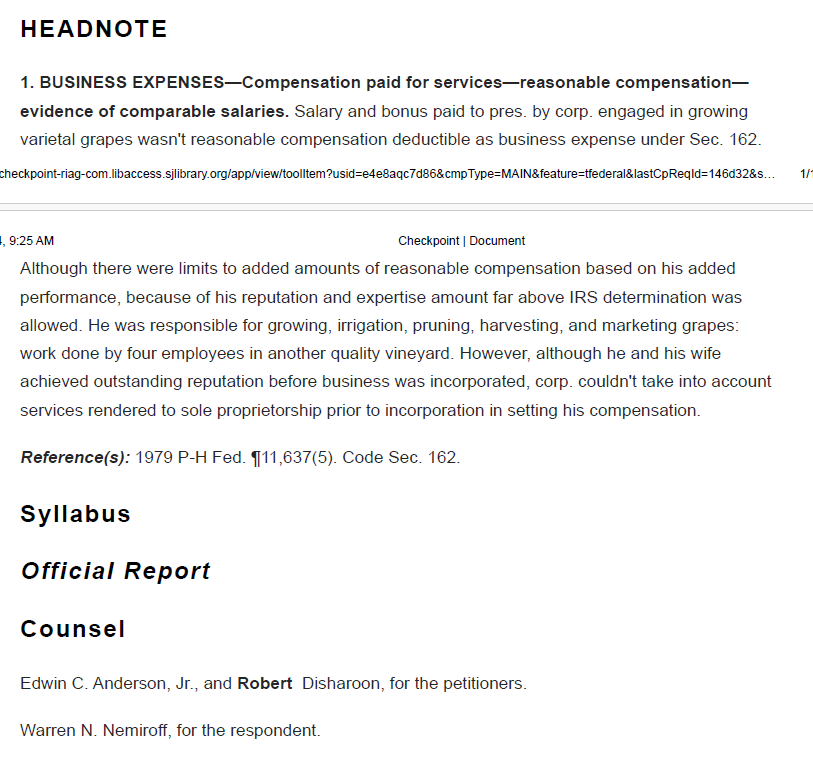

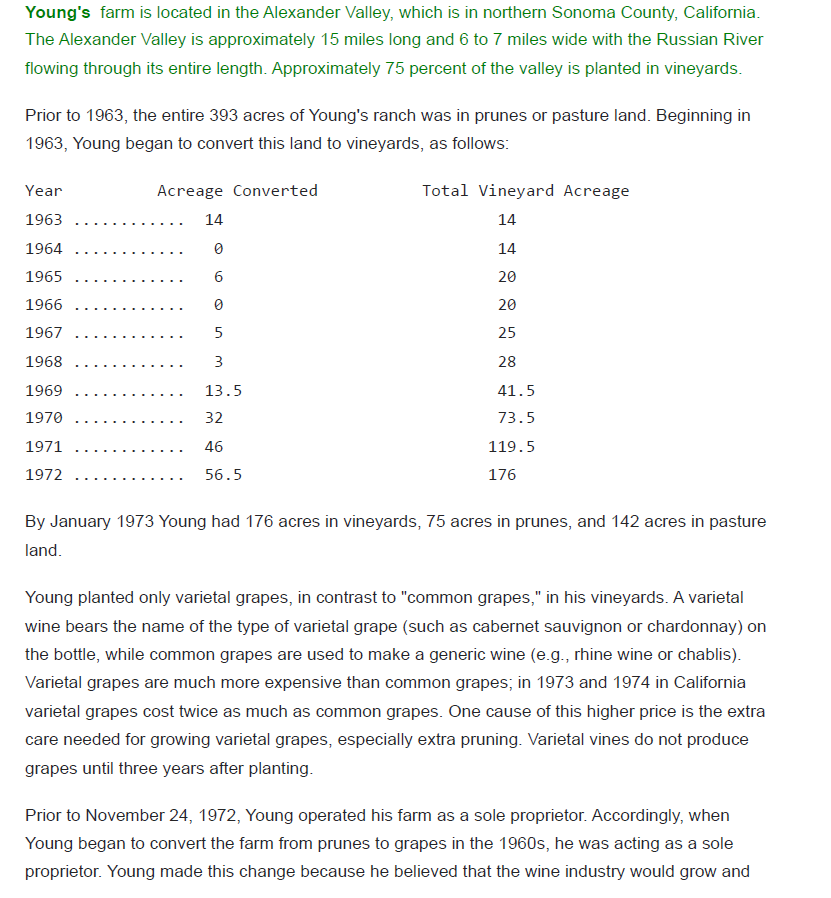

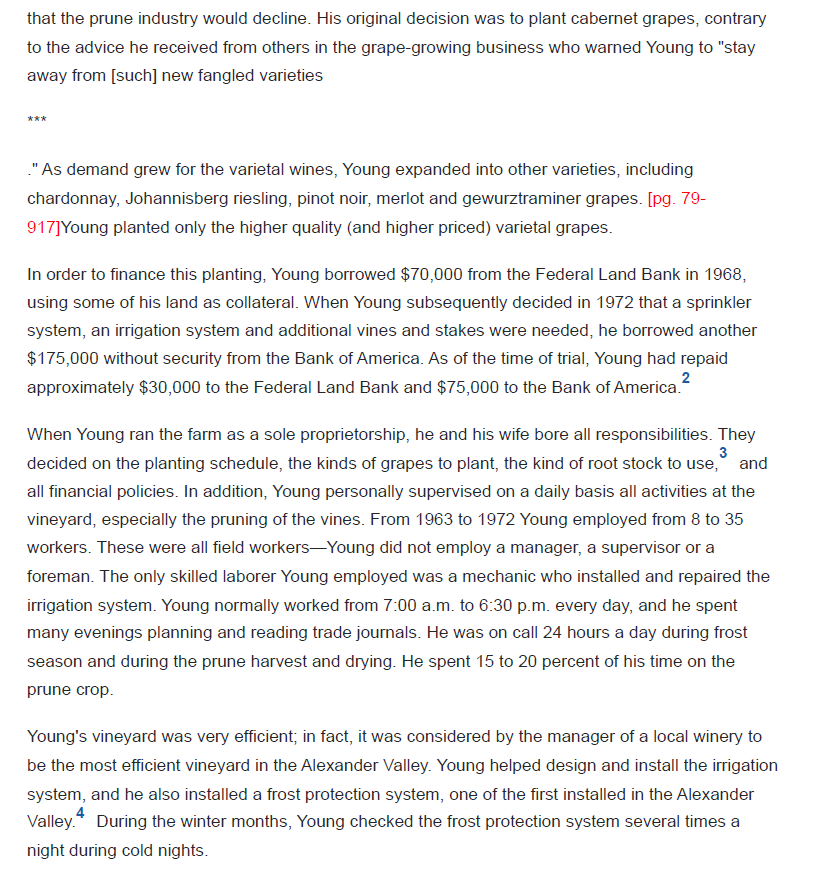

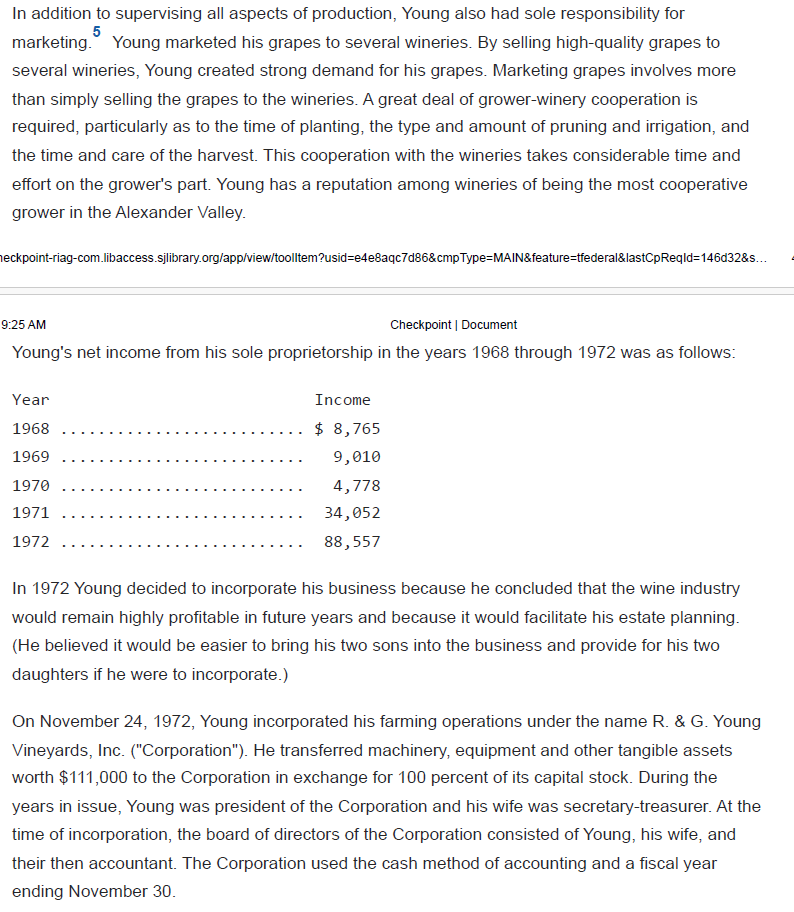

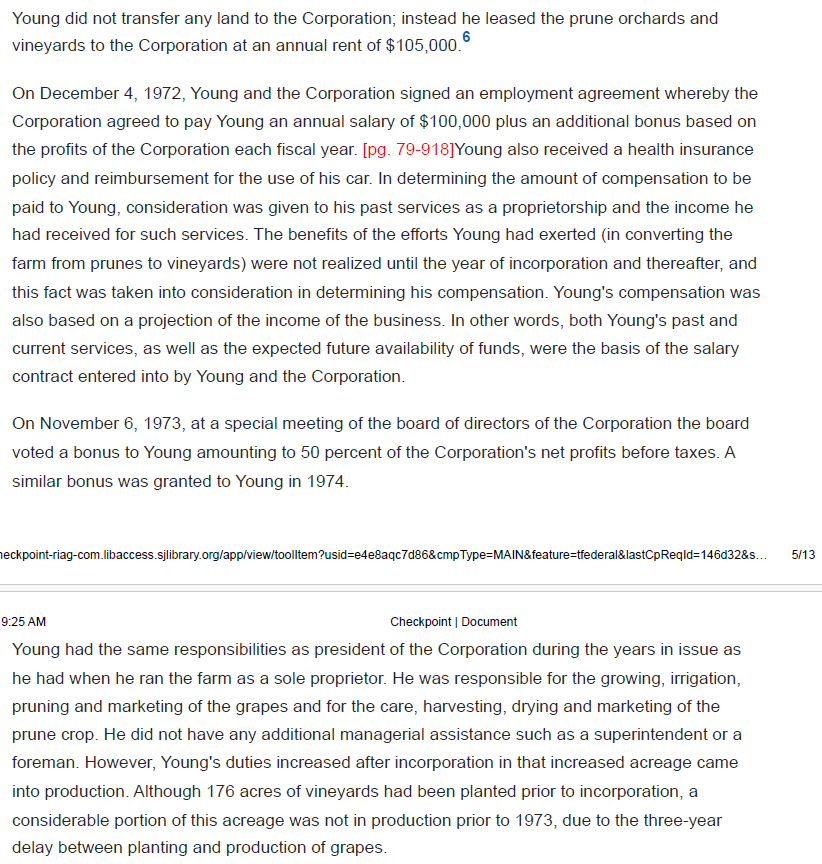

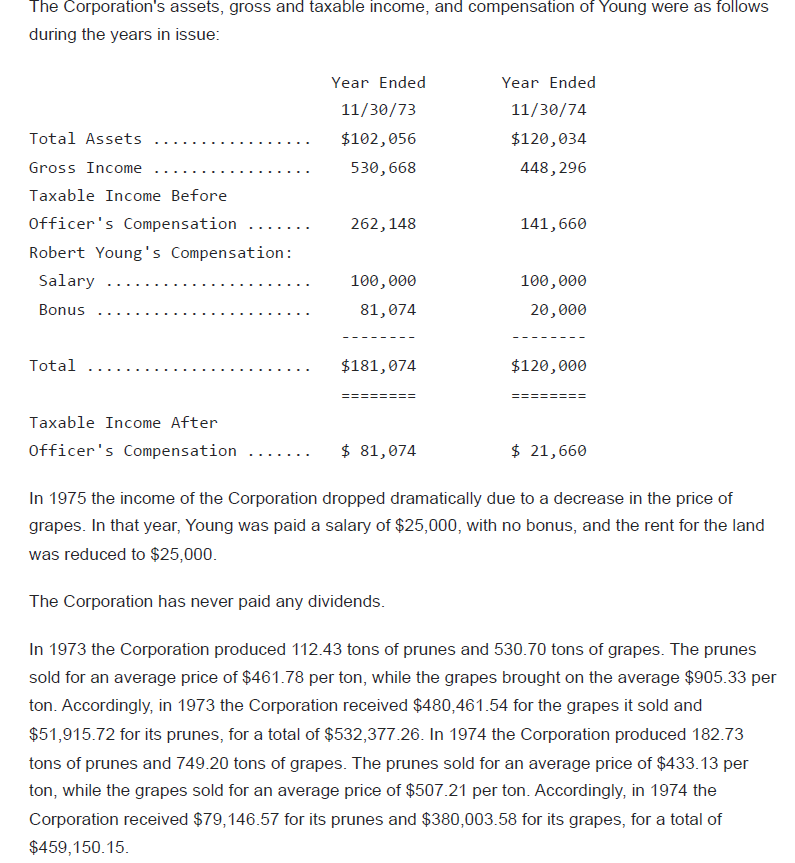

HEADNOTE 1. BUSINESS EXPENSESCompensation paid for servicesreasonable compensation evidence of comparable salaries. Salary and bonus paid to pres. by corp. engaged in growing varietal grapes wasn't reasonable compensation deductible as business expense under Sec. 162. checkpoint-riag-com libaccess sjlibrary org/appiview/toolitem?usid=e4e8aqcTdes&cmp Type=MAIN&feature=tiederal&lasiCpReqld=146d32&s. . 1/ |, 9:25 AM Checkpoint | Document Although there were limits to added amounts of reasonable compensation based on his added performance, because of his reputation and expertise amount far above IRS determination was allowed. He was responsible for growing, irrigation, pruning, harvesting, and marketing grapes: work done by four employees in another quality vineyard. However, although he and his wife achieved outstanding reputation before business was incorporated, corp. couldn't take into account services rendered to sole proprietorship prior to incorporation in setting his compensation. Reference(s): 1979 P-H Fed. 11,637(5). Code Sec. 162. Syllabus Official Report Counsel Edwin C. Anderson, Jr., and Robert Disharoon, for the petitioners. Warren N. Nemiroff, for the respondent. MEMORANDUM FINDINGS OF FACT AND OPINION HALL, Judge: Respondent determined deficiencies in petitioners' income tax as follows: [pg. 79-916] Petitioner Year Ended Deficiency Robert & Gertrude Young . . . . . Dec. 31, 1974 $ 2,828 R. & G. Young Vineyards ..... . Nov. 30, 1973 67, 716 Nov. 30, 1974 37, 532 The sole issue is whether the salary and bonus paid by R. & G. Young Vineyards, Inc. to its president, Robert Young, constituted reasonable compensation deductible as a business expense under section 162.' FINDINGS OF FACT Some of the facts have been stipulated by the parties and are found accordingly. At the time they filed their petitions, petitioners Robert and Gertrude Young were residents of Geyersville, California, and petitioner R. & G. Young Vineyards, Inc. was a California corporation neckpoint-riag-com.libaccess.sjlibrary.org/app/view/toolltem?usid=e4eBaqc7d86&cmpType=MAIN&feature=tfederal&lastCpReqld=146d32&s... 9:25 AM Checkpoint | Document with its principal place of business in Geyserville, California. Robert Young ("Young ") has been in the business of farming in Sonoma County, California, all of his adult life. Young's parents lost their ranch during the Depression. Young and his mother subsequently reacquired the ranch (then 193 acres), and in 1938 Young purchased his mother's interest. In 1953 and 1963 Young acquired two adjacent parcels of land of approximately 100 acres each, which increased the size of the ranch to a total of 393 acres.Young's farm is located in the Alexander Valley, which is in northern Sonoma County, California. The Alexander Valley is approximately 15 miles long and 6 to 7 miles wide with the Russian River flowing through its entire length. Approximately 75 percent of the valley is planted in vineyards. Prior to 1963, the entire 393 acres of Young's ranch was in prunes or pasture land. Beginning in 1963, Young began to convert this land to vineyards, as follows: Year Acreage Converted Total Vineyard Acreage 1963 ............ 14 14 1964 ............ e 14 1965 ............ 6 20 1966 ............ e 20 1967 ............ 5 25 1968 ... ... ..., 3 28 1969 . ... ... ... 13.5 41.5 197 .. ... ... ... 32 73.5 1971 ............ 46 119.5 1972 ............ 56.5 176 By January 1973 Young had 176 acres in vineyards, 75 acres in prunes, and 142 acres in pasture land. Young planted only varietal grapes, in contrast to "common grapes,\" in his vineyards. A varietal wine bears the name of the type of varietal grape (such as cabernet sauvignon or chardonnay) on the bottle, while common grapes are used to make a generic wine (e.g., rhine wine or chablis). Warietal grapes are much more expensive than common grapes; in 1973 and 1974 in California varietal grapes cost twice as much as commeon grapes. One cause of this higher price is the extra care needed for growing varietal grapes, especially extra pruning. Varietal vines do not produce grapes until three years after planting. Prior to November 24, 1972, Young operated his farm as a sole proprietor. Accordingly, when Young began to convert the farm from prunes to grapes in the 1960s, he was acting as a sole proprietor. Young made this change because he believed that the wine industry would grow and that the prune industry would decline. His original decision was to plant cabernet grapes, contrary to the advice he received from others in the grape-growing business who warned Young to "stay away from [such] new fangled varieties " As demand grew for the varietal wines, Young expanded into other varieties, including chardonnay, Johannisberg riesling, pinot noir, merlot and gewurztraminer grapes. [pg. 79- 917Young planted only the higher quality (and higher priced) varietal grapes. In order to finance this planting, Young borrowed $70,000 from the Federal Land Bank in 1968, using some of his land as collateral. When Young subsequently decided in 1972 that a sprinkler system, an irrigation system and additional vines and stakes were needed, he borrowed another $175,000 without security from the Bank of America. As of the time of trial, Young had repaid approximately $30,000 to the Federal Land Bank and $75,000 to the Bank i:':'%reri-::a_2 When Young ran the farm as a sole proprietorship, he and his wife bore all responsibilities. They decided on the planting schedule, the kinds of grapes to plant, the kind of root stock to use,s and all financial policies. In addition, Young personally supervised on a daily basis all activities at the vineyard, especially the pruning of the vines. From 1963 to 1972 Young employed from 8 to 35 workers. These were all field workersYoung did not employ a manager, a supervisor ar a foreman. The only skilled laborer Young employed was a mechanic who installed and repaired the irrigation system. Young normally worked from 7:00 a.m. to 6:30 p.m. every day, and he spent many evenings planning and reading trade journals. He was on call 24 hours a day during frost season and during the prune harvest and drying. He spent 15 to 20 percent of his time on the prune crop. Young's vineyard was very efficient; in fact, it was considered by the manager of a local winery to be the most efficient vineyard in the Alexander Valley. Young helped design and install the irrigation system, and he also installed a frost protection system, one of the first installed in the Alexander Valley.4 During the winter months, Young checked the frost protection system several times a night during cold nights. In addition to supervising all aspects of production, Young also had sole responsibility for markne:ting;]_5 Young marketed his grapes to several wineries. By selling high-quality grapes to several wineries, Young created strong demand for his grapes. Marketing grapes involves more than simply selling the grapes to the wineries. A great deal of grower-winery cooperation is required, particularly as to the time of planting, the type and amount of pruning and irrigation, and the time and care of the harvest. This cooperation with the wineries takes considerable time and effort on the grower's part. Young has a reputation among wineries of being the most cooperative grower in the Alexander Valley. 1eckpoint-riag-com_libaccess sjlibrary. orgfappiview/toolltem ?usid=edelaqcydi6&cmpType=MAIN&feature=tfederal&lasiCpReqld=146d32&s. .. 9:25 AM Checkpoint | Document Young's net income from his sole proprietorship in the years 1968 through 1972 was as follows: Year Income 1968 ... e % 8,765 1969 ... . 9,010 1970 . e 4,778 1971 ... 34,052 1972 . 88,557 In 1972 Young decided to incorporate his business because he concluded that the wine industry would remain highly profitable in future years and because it would facilitate his estate planning. (He believed it would be easier to bring his two sons into the business and provide for his two daughters if he were to incorporate.) On November 24, 1972, Young incorporated his farming operations under the name R. & G. Young Vineyards, Inc. ("Corporation\"). He transferred machinery, equipment and other tangible assets worth $111,000 to the Corporation in exchange for 100 percent of its capital stock. During the years in issue, Young was president of the Corporation and his wife was secretary-treasurer. At the time of incorporation, the board of directors of the Corporation consisted of Young, his wife, and their then accountant. The Corporation used the cash method of accounting and a fiscal year ending November 30. Young did not transfer any land to the Corporation; instead he leased the prune orchards and vineyards to the Corporation at an annual rent of $'I05,[JII]{J_'5 On December 4, 1972, Young and the Corporation signed an employment agreement whereby the Corporation agreed to pay Young an annual salary of $100,000 plus an additional bonus based on the profits of the Corporation each fiscal year. [pg. 79-918]Young also received a health insurance policy and reimbursement for the use of his car. In determining the amount of compensation to be paid to Young, consideration was given to his past services as a proprietorship and the income he had received for such services. The benefits of the efforts Young had exerted (in converting the farm from prunes to vineyards) were not realized until the year of incorporation and thereafter, and this fact was taken into consideration in determining his compensation. Young's compensation was also based on a projection of the income of the business. In other words, both Young's past and current services, as well as the expected future availability of funds, were the basis of the salary contract entered into by Young and the Corporation. On November 6, 1973, at a special meeting of the board of directors of the Corporation the board voted a bonus to Young amounting to 50 percent of the Corporation's net profits before taxes. A similar bonus was granted to Young in 1974. 1eckpoint-riag-com_libaccess. sjlibrary.org/appiview/toolltem fusid=ed eBaqc7d86&cmp Type=MAIN&feature=tlederal&lastCpReqld=146d32&s. .. AM3 925 AM Checkpoint | Document Young had the same responsibilities as president of the Corporation during the years in issue as he had when he ran the farm as a sole proprietor. He was responsible for the growing, irrigation, pruning and marketing of the grapes and for the care, harvesting, drying and marketing of the prune crop. He did not have any additional managerial assistance such as a superintendent ar a foreman. However, Young's duties increased after incorporation in that increased acreage came into production. Although 176 acres of vineyards had been planted prior to incorporation, a considerable portion of this acreage was not in production prior to 1973, due to the three-year delay between planting and production of grapes. The Corporation's assets, gross and taxable income, and compensation of Young were as follows during the years in issue: Year Ended Year Ended 11/30/73 11/30/74 Total Assets ................. $102,856 $120,034 Gross Income ................. 530, 668 448,296 Taxable Income Before Officer's Compensation ....... 262,148 141,668 Robert Young's Compensation: Salary . 100,000 100,000 BONUS v eeeee e e 81,074 20,000 Total ... $181,074 $120,000 Taxable Income After Officer's Compensation ....... % 81,074 % 21,660 In 1975 the income of the Corporation dropped dramatically due to a decrease in the price of grapes. In that year, Young was paid a salary of $25,000, with no bonus, and the rent for the land was reduced to $25,000. The Corporation has never paid any dividends. In 1973 the Corporation produced 112.43 tons of prunes and 530.70 tons of grapes. The prunes sold for an average price of $461.78 per ton, while the grapes brought on the average $905.33 per ton. Accordingly, in 1973 the Corporation received $480,461 .54 for the grapes it sold and $51,915.72 for its prunes, for a total of $532,377.26. In 1974 the Corporation produced 182.73 tons of prunes and 749.20 tons of grapes. The prunes sold for an average price of $433.13 per ton, while the grapes sold for an average price of $507.21 per ton. Accordingly, in 1974 the Corporation received $79,146.57 for its prunes and $380,003.58 for its grapes, for a total of $459,150.15. The Corporation received top prices for its grapes. In 1973 the price range for black grapes was from $415 to $815, with the lower price being paid for common grapes and the higher for varietals. The price range for white grapes in that year was from $310 to $815. In 1974, the price range was from $290 to $685 for black grapes and from $230 to $650 for white grapes. In addition, growers could receive quality bonuses based on the sugar and acid content of the grapes. Some wineries also paid growers bonuses on the basis of the cooperation between the grower and the winery. During the years in issue, the Corporation received bonuses for both quality and cooperation. Young's reputation as a grower was unsurpassed, and this reputation was reflected [pg. 79-919]in the price he received for his grapes. Among growers in the Alexander Valley, Young had the reputation as the person who would "get top price for each variety, every year "and as "the person who in effect bumped the price and got the higher prices to the growers " Simultaneously, he had a reputation as the most cooperative grower from the point of view of the wineries. The manager of Chateau St. Jean described Young's cooperation as "beyond reproach,\" and he considered Young's grapes the best his winery purchased. In fact, Chateau 5t. Jean held Young's grapes in such high regard that it annually bottled wines using exclusively grapes purchased from the Crporation_T On the labels of these bottles, the wines were identified as being produced at "Robert Young Vineyards." Chateau St. Jean has received several gold and silver medals in wine competitions for its Robert Young Vineyards wines. In addition to having an unsurpassed reputation as to the quality of the grapes he produced, Young also had an excellent reputation as to the manner in which he operated his vineyard. A local banker viewed Young as "a leader in the industry." Young was viewed as innovative, an astute businessman, and "his farming practices were recognized as being tops in the county.\" In addition, the quantity and quality of his grapes were well above average. The local banker's assessment was shared by local growers. Mr. Green, who owned a neighbaring vineyard, believed that Young's vineyard could not be run better and that he was "embarrassed\" to have his vineyard compared to Young's. In addition, Mr. Green had more employees working in his vineyard, as well as a vineyard manager, a field superintendent and two foremen. Young performed alone all the duties of these supervisory employees and also had all the owner's decision-making responsibilities. By means of comparison, Mr. Green paid his vineyard manager $51,000 in 1973 and $56,000 in 1974, and the vineyard manager was given a house fo live in. During this same period, Mr. Green sificheckpoint-riag-com _libaccess sjlibrary org/appiview/toolltem ?usid=ed eBaqc7da6&cmp Type=MAIN&feature=tfederal&lastCpReqld=146d328&s . M3 24, %25 AM Checkpoint | Document paid his field superintendent approximately $10,000 to $12,000, and the two crew foremen each earned $3,000 to $4,000 more than the normal field hand. In 1973 and 1974 Mr. Ruddick was the manager of the Mendocino Vineyard Company's vineyards, which comprised approximately 800 acres of vineyards. As such, he was in charge of personnel, housing and all viticultural practices, including irrigation. However, he had no responsibility for selling the vineyards' production. He also supervised the growing of other crops, including 57 acres of pears and 14 acres of prunes. For these services, Mr. Ruddick was paid $12,000 by Mendocino Vineyards Company in 1973 and $20,000 in 1974_In 1973, Mendocino Vineyards Company sold its production from 800 acres for approximately $1,300,000 at an average price of $400 per ton. In 1973 and 1974 Mr. Parducci was the manager and wine master of Parducci Wine Cellars, Inc. Mr. Parducci owned 50 of the 1700 shares of Parducci Wine Cellars, Inc. He had complete control of all growing and winery operations, and personally supervised both the growing of the grapes and the making of the wine. He did not sell grapes to other wineries. During these years, he supervised the growing of grapes on approximately 300 acres of vineyards, of which 150 acres were varietals and the remainder were commaon grapes. He was assisted in this task by two foremen. For these services, he received a salary of $25,000 per year in 1973 and 1974. He also was entitled to a percentage of the profits during those years, but there were no profits for distribution in those years because all profits were being plowed back into development of the winery's facilities. He estimated that 75 percent of his compensation was for his services as a winemaster. In the statutory notices, respondent determined that the salary and bonuses paid by the Corporation to Young were in excess of reasonable compensation. Respondent determined that reasonable compensation for Young's services was $40,000 per year in fiscal 1973 and 1974. Respondent determined that the remainder of the compensation paid to Young by the Corporation 5$141,074 in fiscal 1973 and $80,000 in fiscal 1974constituted a nondeductible dividend distribution and disallowed the Corporation's claimed deductions in those amounts. Respondent determined that $80,000 received by Young in calendar 1974 constituted a dividend distribution to him. Young and his wife concede that, if and to the extent it is found that respondent is correct in his determination that part of Young's purported compensation in [pg. 79-920]calendar 1974 was dividend income, to that extent the maximum tax limitation does not apply. ULTIMATE FINDING OF FACT The amount of reasonable compensation for Young's services during each of the fiscal years 1973 and 1974 was $75,000 per year. OPINION ittps://checkpoint-riag-com.libaccess.sjlibrary.org/app/view/toolltem?usid=e4eBaqc7d86&cmpType=MAIN&feature=tfederal&lastCpReqld=146d32&s... 8/ 0/9/24, 9:25 AM Checkpoint | Document The sole issue for decision is whether the salary and bonus paid by R. & G. Young Vineyards, Inc. ("Corporation") to its president, Robert Young ("Young "), in each of the years in issue constituted reasonable compensation deductible as a business expense. Petitioners contend that the entire compensation paid, $181,074 in fiscal 1973 and $120,000 in fiscal 1974, was reasonable for his present and past services. Respondent, on the other hand, determined that reasonable compensation for Young in each year was $40,000. Section 162(a)(1) allows as a deduction "a reasonable allowance for salaries or other compensation for personal services actually rendered." To be deductible, compensation must be (1) reasonable and (2) for services actually rendered. Section 1.162-7(a), Income Tax Regs.; Nor-Cal Adjusters v. Commissioner, [ 503 F.2d 359, 362 34 AFTR 2d 74-5834] (9th Cir. 1974), affg. a Memorandum Opinion of this Court. The form or method of fixing compensation is not determinative of deductibility. [ Section 1.162-7(b)(2), Income Tax Regs. However, compensation which is a guise for the distribution of dividends to employee-stockholders is not deductible. = Section 1.162-7(b)(1), Income Tax Regs.Whether compensation is reasonable and paid for services rendered is a question of fact, and the burden of proof is on petitioners. Botany Worsted Mills v. United States, @ 278 U 5. 282, 289-290 [E TAFTR 8847] (1929); Charles Schneider & Co_, Inc. v. Commissioner, E 500 F.2d 148, 151 [ % 34 AFTR 2d 74-5422] (8th Cir. 1974), affg. a Memorandum Opinion of this Court, cert. denied 420 U.5.908 (1975); Pacific Grains, Inc. v. Commissioner, 3 399 F2d 603, 605 [@ 22AFTR 2d 5413] (9th Cir. 1968), affg. a Memorandum Opinion of this Court; Pepsi-Cola Bottling Co. of Salina, Inc. v. Commissioner, []61 T.C. 564, 567 (1974), affd. [] 528 F.2d 176 [[=] 37 AFTR 2d 76-369] (10th Cir. 1975). Among the facts considered are (1) the employee's qualifications; (2) the nature, extent and scope of the employee's work; (3) the size and complexities of the business; (4) a comparison of salaries with the gross and net income of the business; (5) prevailing economic conditions; (6) the dividend history of the business; and (7) the compansation paid for comparable services in comparable businesses. Mayson Mfg. Co. v. Commissioner, @ 178 F.2d 115, 119 [@ 38 AFTR 1028] (6th Cir. 1949), revg. a Memorandum Opinion of this Court; Pepsi-Cola Bottling Co. of Salina, Inc. v. Commissioner, supra. No single factor is decisive; rather, we must consider and weigh all the facts and circumstances. Mayson Mfg. Co. v. Commissioner, supra. Compensation paid to major shareholders of a corporation is subject to close scrutiny. Charles Schneider & Co ., Inc. v. Commissioner, supra at 152; Paula Construction Co. v. Commissioner, 2 58 T.C. 1055, 1058 (1972), affd. per curiam 474 F.2d 1345 [E 31 AFTR 2d 73-926] (5th Cir. 1973). During the years in issue, Young was the president of the Corporation and its principal employee. He alone was responsible for the growing, irrigation, pruning, harvesting and marketing of the grapes, and the growing, harvesting, drying and marketing of the prune crop. He did not have any managerial assistance in the form of a superintendent, field managers or foremen. During the years in issue, Young was the president of the Corporation and its principal employee. He alone was responsible for the growing, irrigation, pruning, harvesting and marketing of the grapes, and the growing, harvesting, drying and marketing of the prune crop. He did not have any managerial assistance in the form of a superintendent, field managers or foremen. ficheckpoint-riag-com libaccess sjlibrary. org/appiview/toolltem?usid=ed eBaqc7d86&cmp Type=MAIN&feature=tfederal&lastCpReqld=146d32&s. .. 24 925 AM Checkpoint | Document On brief respondent does not question Young's business acumen or the scope of his duties. In fact, respondent stated: Unquestionably, Robert Young is a man of formidable business skills, which together with his business acumen made him extremely valuable to the corporation. There is no doubting the fact he was ahead of his time in planting varietal grapes *** and that he was in the forefront in use of advanced techniques in antifreezing and imgation. *** There is also no doubt he performed a myriad of services for the corporation and apparently made all management decisions. Monetheless, respondent determined that Young's reasonable compensation was only $40,000 per year. Respondent contends, primarily, that the service performed by Messrs. Ruddick and Parducci were comparable to the services performed by Young, and therefore Young is entitled only to a comparable salary. Mr. Ruddick earned a salary of $12,000 in 1973 and $20,000 in 1974, while Mr. Parducci earned a salary of $25,000 in both years. We conclude that $75,000 represents a reasonable salary for Young in each of [pg. 79-921]the Corporation's fiscal years 1973 and 1974. The services rendered by Mr. Ruddick are not fully comparable to those provided by Young. Mr. Ruddick managed a large vineyard, 800 acres, but on it he grew almost exclusively low-quality common grapes. Mr. Ruddick received only an average price of $400 per ton for the grapes he sold. Mr. Ruddick's grapes were at the very bottom of the price range, while the Corporation's were at the very top. Young had a yield per acre of 4.57 tons while Mr. Ruddick had a yield of only 4.06 tons per acre. Mr. Ruddick did not have either the sales or ownership responsibilities which Young bore. Although Mr. Ruddick managed the vineyards, he did not have to engage in any of the long- term planning which took a fair portion of Young's time and efforts. All of these distinctions between the requirements of Young's and Mr. Ruddick's responsibilities are important, but we believe the most important difference is reflected in the prices received for the grapes they sold. The production of high-quality grapes is a difficult and time-consuming task. Young devoted considerable amounts of time to the care of his grapes, especially the pruning, irrigation and harvesting of the crop. All these efforts led to an extraordinary yield. Just as the quality of the wines which came from these grapes cannot be equated, we similarly believe that the efforts of Young and Mr. Ruddick cannot be equated. Likewise, we do not find Mr. Parducci's compensation entirely comparable. Mr. Parducci received a salary of $25,000 in 1973 and in 1974. In addition, Mr. Parducci was entitled to an unspecified percentage of the profits of the business in both years. As it turned out there were no profits available for distribution because all the profits were reinvested, but this entitlement to an unspecified share of the profits undermines a comparison of Mr. Parducci's $25,000 salary to checkpoint-riag-com.libaccess.sjlibrary.org/app/view/toolitem?usid=e4eBaqc7d86&cmp Type=MAIN&feature=tfederal&lastCpReqld=146d32&... 9:25 AM Checkpoint | Document Young's compensation. In addition, Mr. Parducci was assisted by two foremen. Finally, although we do not have a price comparison for the grapes Mr. Parducci grew, we know that approximately half of his vineyard was planted in common grapes. As with Mr. Ruddick, Mr. Parducci's efforts in growing these common grapes cannot be equated to the care Young gave to his high-quality varietal vineyard.We doubt that any northern California vineyard is completely comparable to Young's, considering his reputation for quality, efficiency and cooperation with the wineries. Nevertheless, if a comparison is to be made, we believe that a comparison to Mr. Green's vineyard is most applicable. Mr. Green employed a vineyard manager, a field superintendent and two crew foremen, at combined salaries of from approximately $68,000 to $?5,DJD,3 plus the vineyard manager had the use of a house. All four men performed, together, essentially the tasks which Young performed alone. However, they did not have all the decision-making responsibility which Young bore, particularly the responsibility for long-range planning. Although Mr. Green's vineyard was a quality vineyard, it does not have as fine a reputation for guality and efficiency as Young has developed for his vineyard. In setting Young's compensation for the years in issue the corporation took into account not only services currently being rendered to the corporation but also services rendered to the sole proprietorship prior to the incorporation of the business. We agree with respondent that the corporation is not entitled to a deduction for compensation for services rendered to a preexisting sole proprietorship. U.S. Asiatic Co. v. Commissioner, [=)30 T.C. 1373 (1958), supports respondent's contention. In U.5_ Asiatic, Mr. Hartman, who was to become the sole shareholder of the taxpayer, engaged in trade with Japan in 1947 as a member of a partnership with two other individuals. Beginning in December 1947, Hartman conducted business only under his own name, but he continued to work with and through the offices of his former partners. He entered several profitable trading transactions while operating on his own. Finally, in May 1948, Hartman incorporated his business under the name U.5. Asiatic Co. Two days after incorporation, the corporation paid him a salary for the period October 1947 through March 1948, and it reimbursed his expenses for that period. In disallowing these deductions, we held that there is no warrant whatever for [the corporation's] attempt to accrue and deduct, as expenses of carrying on its own business after incorporation, salary to Hartman for preceding periods when he could not possibly have been either [pg. 79-922]an officer or employee of the corporation, and business expenses which had been incurred and paid by Hartman during said preceding periods when he was operating either as a joint venturer or as a sole proprietor. In Bianchi v. Commissioner, =|66 T.C. 324 (1976), affd. without opinion 553 F.2d 93 [=) 39 AFTR2d 77-894] (2d Cir. 1977), we noted that generally the separateness of different entities must be respected. Following U.S. Asiatic we held that compensation for the pre-incorporation period does not constitute "compensation\" within the meaning of =) section 1.404(a)-1(b), Income Tax Regs. But see R. J. Nicoll Co. v. Commissioner, =| 53 T.C. 37 (1972), in which we held that compensation paid by a successor-corporation was reasonable for current services and for services rendered by the shareholder-employee in prior years to the corporate-employer's predecessor on the grounds that the taxpayer was the direct beneficiary of the prior undercompensated services of the shareholder-employee. Here we cannot say that Young was undercompensated for his services rendered to the sole proprietorship since he received all the net income the business produced. But in any event, the value of any services rendered in establishing the vineyard (as well as capital invested therein) was recovered by way of rent charged the corporation for the vineyards, and by way of capital contribution to the corporation in exchange for stock. It cannot also be recovered by means of compensation. Since the record shows that some substantial portion of Young's salary was paid for past services to the predecessor proprietorship, it is clear that considerably less than all the compensation paid could be deductible. In reaching our conclusion as to reasonable compensation, we are also bound to take into consideration the very high percentage of taxable income before compensation which was paid out nominally as compensation. Mayson Mfg. Co. v. Commissioner, supra. In fiscal 1973, Young's compensation was 69 percent of pre-compensation income; in fiscal 1974 it was 85 percent. Such high percentages of income paid to a sole shareholder call for particular scrutiny. In addition, we have considered the fact that the annual bonus to Young, the sole shareholder, was decided upon late in the year and was based on profit, further circumstances suggestive of an attempt to disguise dividends as compensation. Finally, although we are persuaded that Young was an outstanding producer, and was worth considerably more than the other individuals whose compensation during 1973 and 1974 were in the record, there are limits to the added amounts which are reasonable compensation for Young's added performance. We think these limits were significantly exceeded here. Taking all of the favorable and unfavorable factors into consideration, together with the entire record in the case, and using our own best judgment, we have found as a fact that 575,000 per year constituted the limit of reasonable compensation in both fiscal 1973 and 1974

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Law Questions!