Question: it is all one question just multiple parts one options contract so 100 shares Name: 1. Suppose that you take the following European option positions.

it is all one question just multiple parts

one options contract so 100 shares

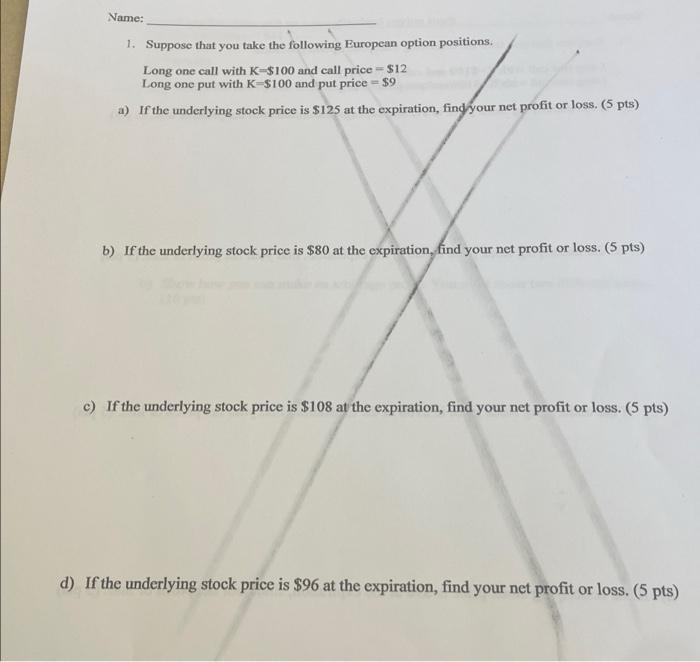

Name: 1. Suppose that you take the following European option positions. Long one call with K-$100 and call price = $12 Long one put with K-$100 and put price - $9 a) If the underlying stock price is $125 at the expiration, find your net profit or loss. (5 pts) b) If the underlying stock price is $80 at the expiration, find your net profit or loss. (5 pts) c) If the underlying stock price is $108 at the expiration, find your net profit or loss. (5 pts) d) If the underlying stock price is $96 at the expiration, find your net profit or loss. (5 pts)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock