It is early January, 2017, and you are a member of the board of directors of Soledad

Question:

It is early January, 2017, and you are a member of the board of directors of Soledad National Ban-corp, located in Soledad, California. The board is meeting to decide if there is enough positive evi-dence to reverse the deferred income tax valuation allowance that the Company has had since it went public at the end of 2008.

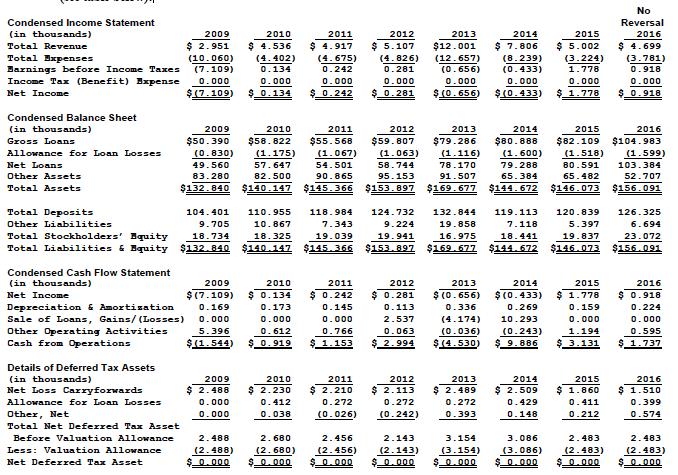

From 2009 through 2015, Soledad had a full valuation allowance on its deferred income tax assets (see table below):

At the time of the establishment of the full valuation allowance in 2009, management concluded that it was more likely than not that the full deferred tax asset would not be realized. Management con-sidered all positive and negative evidence regarding the ultimate ability to fully realize the deferred tax asset, including past operating results and the forecast of future taxable income. The valuation allowance was primarily recorded and maintained because the Company is a continuing cumulative loss company, i.e. the Company’s cumulative combined Earnings before Income Taxes beginning in 2009 through 2016 are a negative $4.845 million. However, the cumulative Earnings before Income Taxes from 2013 through 2016 are now a positive $1.607 million.

Highlights for the quarter ended December 31, 2016 include:

- A. Ninth consecutive profitable quarter

- B. Net loan growth of $4.9 million, or 5.0% versus linked-quarter

- C. Strong asset quality; no nonperforming assets

- D. Return on Assets and Return on Equity of 5.5% and 37.4%, respectively

- E. Martin P. May, President and CEO, commented: “We continued to grow our loan and deposit portfo-lios organically and our capital ratios significantly exceed all regulatory guidelines for a well-capitalized bank. The Company expects to record income tax expense in future quarters assuming the Company continues to generate pre-tax earnings.”

In addition, the Company’s share price had performed well during 2016. From a low of $4.80 a share in early February 2016, it reached a high of $7.60 a share in late December 2016 (see chart below):

Nevertheless, as a board member, your fiduciary duty is to recommend actions that are in the best interests of the Company’s shareholders. Without the reversal, the Company’s net deferred income tax asset would remain at $0 and its net income would be $918 thousand. If Soledad reverses the full1 deferred income tax asset valuation allowance the net deferred income tax asset change as will the Company’s net income for the year ended December 31, 2016. If the market believes the reversal is a signal that the Company has “turned the corner”, its growth prospects would be enhanced as would its share price. On the other hand, if the Company’s future performance does not live up to the ex-pectations suggested by the valuation allowance reversal in 2016, with hindsight, investors might accuse Soledad of “cooking its books” for 2016 and reduce its share price.

The CFO has asked for your help in deciding if the evidence is greater than 50% that the Company will realize the $2.483 million in benefits from its deferred income tax assets.

Questions:

1. Record (bookkeep) Soledad’s initiating its valuation allowance for fiscal year 2009.

2. Record (bookkeep) the impact of Soledad’s proposed full reversal of its valuation allowance in fiscal 2016. What will be the impact on Soledad’s 2016 income statement, balance sheet and cash flows for book accounting purposes? for tax accounting purposes? Please show any calculations to support your answer.

3. As a board member, list any positive evidence that you believe supports Soledad’s reversal of its valuation allowance in 2016.

4. As a board member, list any negative evidence that you believe supports Soledad’s not reversing its valuation allowance in 2016.

5. As a board member, based on your consideration of the evidence, what would you recommend to the CFO? Is the evidence sufficient or not sufficient to show a greater than 50% probability that the deferred income tax benefits will be realized in the future? Briefly explain.

Expert Answer:

Q1 To balance out its deferred tax assets the company needs record a valuation allowance of 2483 million Net income will be 918 thousand with a net deferred tax asset of 0 Q2 Fiscal 2016 would have a ... View the full answer