It is January 15, 2022, and you just finished a meeting with the tax partner of your

Question:

It is January 15, 2022, and you just finished a meeting with the tax partner of your CPA firm, Lin & Robson Associates LLP and new clients Jeff and Caroline Samson. The Samsons live in Winnipeg, Manitoba, and have 2 children in elementary school.

Jeff (age 36) and his wife Caroline (age 35) wholly own Jet Traders Ltd. (Jets). They each own 50% of the common shares of the corporation which they incorporated whine in university in 2005. The shares were issued on incorporation for $1,000, $500 paid by each of Jeff and Caroline. The Company is located in Winnipeg, Manitoba and operates a large distribution business that sells sports memorabilia to stores in Ontario and Manitoba. The company owns a building in Winnipeg which houses the company's head office and warehouse space. The company also owns a warehouse in Ontario which is currently rented to a 3rd party for$36,500 a year.

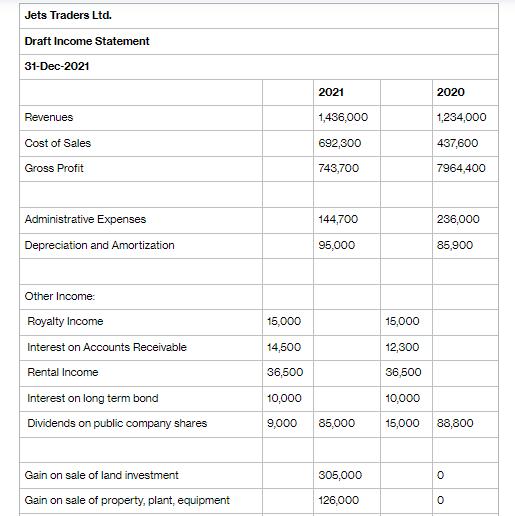

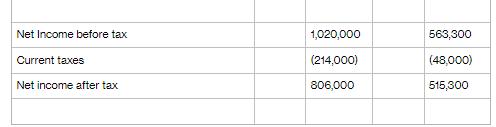

In the meeting, Jeff provided the draft income statement for the corporation's fiscal year ended December 31, 2021. Jeff would like to know when his corporate and HST returns and payments are due. He also is not sure what information the firm needs to prepare the returns and would like some guidance. The tax partner has asked you to analyze the information Jeff has provided and asked for a draft memorandum for the tax file including a preliminary list of the Schedule I and Division C adjustments that will impact the corporate return and a list of additional information that should be requested.

Jeff indicated that he and Caroline, received salaries of $100,000 and $50,000 respectively from their companies or the year. Their only sources of income for 2021 are the salaries and dividends from Jets and another company Sports Freaks Inc. (SFI) discussed below.

In the meeting, Jeff asked about a real estate sale that occurred in 2021. The sale involved 3 acres of land purchased in 2018 that was adjacent to the Jets Winnipeg warehouse. The land included an abandoned house that was occupied by the previous owner before his death. Jeff who was friends with the executor of the previous owner's estate bought the property thinking at the time that he might want to expand the Winnipeg warehouse space. Over the past couple of years, Jet was able to optimize its excess warehouse space in both Manitoba and Ontario. As a result, the company now has excess warehouse space in both Manitoba and Ontario. Jets paid $150,000 (a bargain price) for the property in 2018 including legal and land transfer and sold it this year for $455,000 net of the real estate commission and legal fees. Jeff is wondering about the tax treatment of this disposition and has asked if there is an additional information you will need from him. As well, the partner asked that you identify any HST/GST considerations associated with the sale.

The royalty income on the income statement relates to a license that Jets owns for the use of Winnipeg sports team logos. Printing companies in Winnipeg and the surrounding area pay royalties to Jets for the use of logos on sports t-shirts and other types of clothing. Sometimes, Jets purchases products from customers of these printing companies for its distribution business.

Jeff owns 100% of a small sports retailer, SFI operating out of IG Field at the University of Manitoba. Jeff provided the 2020 tax return for SFI and the company had $50,000 of taxable income for its December 31, 2020 taxation year end. SFI has never had any passive income. The tax partner has asked you to consider how much small business deduction will be available to Jets and SFI for 2021 and 2022.

During the year, Jet sold some properties in 2021. Jeff provided the following cost and selling price information. You were able to obtain the UCC balance information from the 2020 tax return for Jets that he provided:

The warehouse equipment was acquired in 2017 ad was used in the distribution business. The franchise was acquired in 2019 and was a retail franchise Jets owned in Winnipeg.

Jeff would like to better understand the tax treatment of each type of income earned by Jets and the type of tax rate that will apply. He would also like to understand the impact of the dividends paid to Jeff and Caroline (note in the additional information below) on the corporate tax liability for the Jets. He would like to know what tax rate will apply to the dividends received by each of them in 2021 and how much after-tax cash they have available for personal use from the 2021 dividend payments. The tax partner has asked you to consider if the dividends could have been better planned for 2021 to reduce the marginal tax rate and resulting personal tax. (Ignore TOSI for purposes of this analysis).

The corporation uses ASPE for financial reporting purposes and the taxes payable method of accounting for income taxes. Jeff knows that the tax provision booked in the financial statements needs to be adjusted. The tax partner has asked you to determine the financial reporting entries that would be needed assuming dividends are likely to be paid in the future. Once the tax returns are prepared, the entries can be adjusted for the tax liability determined. For now, the partner has asked you to use $270,000 as the total federal and provincial tax payable (before installment) for the corporation for 2021 as an estimate.

Additional information provided by Jeff or found in the 2020 corporate return:

Jets made a donation to a registered charity of $12,500 during the year.

Four quarterly non-eligible dividends of $45,000 were declared at the end of each calendar quarter of 2021 and paid within two weeks of their declaration. The last quarterly dividend of 2021 was paid in January 2022 and a non-eligible dividend of $30,000 declared in the last quarter of 2020 was paid in January 2021.

The combined taxable capital of Jets and SFI for tax purposes was $9,000,000 at December 31, 2020.

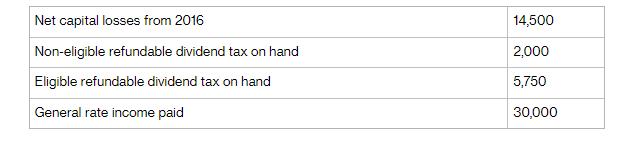

The balance in tax accounts on January 1, 2021, were:

REQUIRED

Assess the situation.

Identify the issues.

Analyze the issues.

Advise/recommend using tax memo.

Expert Answer:

Tax Memorandum Date January 15 2022 To Tax Partner Lin Robson Associates LLP From shadrack Kiprono Tax Analyst remember to replace witg your name Subj... View the full answer