It is September 17, 2022, and you, CPA, work as the senior tax analyst for OCI...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

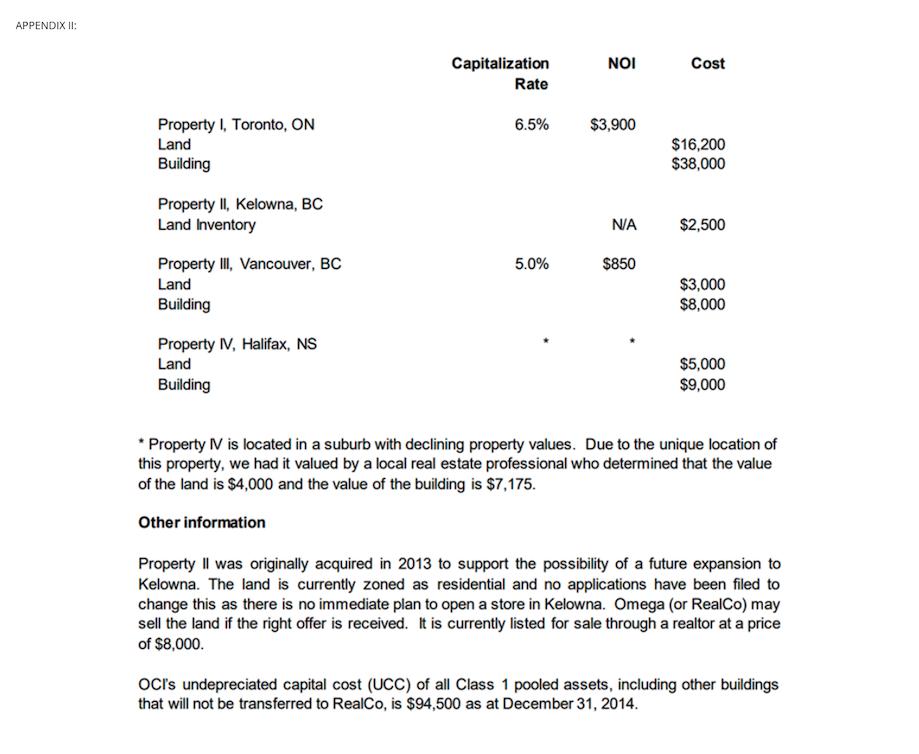

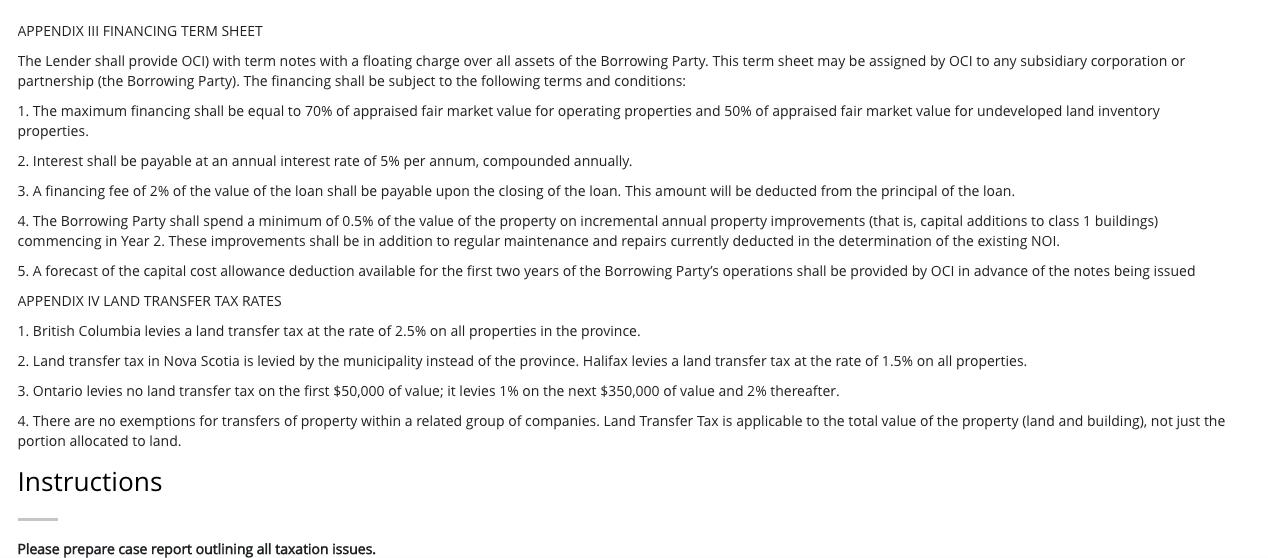

It is September 17, 2022, and you, CPA, work as the senior tax analyst for OCI Inc. (OCI). OCI is an electronics retailer and its shares are traded on the Toronto Stock Exchange. Part of its success has been through partially financing real estate developers during the construction of new strip malls and by owning its own real estate. You have completed a meeting with your boss, Chad Bowie, the vice-president of finance, to discuss the financing of a proposed expansion. OCI requires $45 million in financing to complete this expansion. "We've done all of our financial and tax diligence around the purchase, so we don't need to look at those elements of the project," said Chad. "I need to finalize the financing. I would like to leverage our real estate portfolio but limit the security to the real estate itself. Our bank has indicated the best way to achieve this is to move the real estate into a new wholly-owned corporation ("RealCo"). We could get more financing by leveraging these properties than we could with traditional mortgages. I'd like you to look at a few things for me. I will send you an e-mail shortly with my specific requests." (Appendix I) APPENDIX I E-MAIL FROM CHAD BOWIE From: C Bowie To: CPA Re: Requests for proposed transaction The OCI real estate portfolio has grown in value over a number of years. This type of real estate is usually valued through a capitalization rate method, by capitalizing the property's net operating income (NOI) before tax to determine the fair market value for the total property (land plus building). The NOI of a property consists of the cash income for a property and excludes depreciation. The NOI and capitalization rate for each property are attached (Appendix II). We generally assume that land is worth 30% of the value of the total property. I would like you to address the following: The financing term sheet (Appendix III) bases the financing on the fair market value of the properties moved into RealCo. I need you to determine if the loan will provide us with enough cash to fund our expansion after paying the land transfer tax and financing fees. Land transfer tax rates are in Appendix IV. Are there any assets that will not qualify to be transferred to RealCo without incurring immediate income tax? If so, which one(s) will not qualify and how will we transfer them? I hope at least some of the assets can be transferred to RealCo on a tax-free or tax-deferred basis. If so, please explain what provisions in the Income Tax Act allow for this, and generally how the transaction would be structured. For the assets that can be transferred without incurring immediate income tax, how will the transfer price for tax purposes be determined? What will deadline for filing any elections that may be required? Once you have explained this, please draft any tax elections that may be required with respect to the transfer by calculating the amounts at which the assets will be transferred and the consideration that will be taken back. Include the precise numbers to use on the forms. We will make the acquisition directly through RealCo, so there is no need to discuss how to get the money out of RealCo once the loan is received. The bank has an additional request. I'd like you to prepare the forecast of capital cost allowance deduction available in the first two years in item number 5 of their term sheet. I'd like to have RealCo incorporated on October 1, 2022. To simplify financial reporting, RealCo will have a year-end of December 31. Also hope you can tell me the tax treatment of some specific items I have identified for RealCo (Appendix V) - will they all be treated the same for tax as for accounting? APPENDIX II: Property I, Toronto, ON Land Building Property II, Kelowna, BC Land Inventory Property III, Vancouver, BC Land Building Property IV, Halifax, NS Land Building Capitalization Rate 6.5% 5.0% ΝΟΙ $3,900 N/A $850 Cost $16,200 $38,000 $2,500 $3,000 $8,000 $5,000 $9,000 * Property IV is located in a suburb with declining property values. Due to the unique location of this property, we had it valued by a local real estate professional who determined that the value of the land is $4,000 and the value of the building is $7,175. Other information Property II was originally acquired in 2013 to support the possibility of a future expansion to Kelowna. The land is currently zoned as residential and no applications have been filed to change this as there is no immediate plan to open a store in Kelowna. Omega (or RealCo) may sell the land if the right offer is received. It is currently listed for sale through a realtor at a price of $8,000. OCI's undepreciated capital cost (UCC) of all Class 1 pooled assets, including other buildings that will not be transferred to RealCo, is $94,500 as at December 31, 2014. APPENDIX III FINANCING TERM SHEET The Lender shall provide OCI) with term notes with a floating charge over all assets of the Borrowing Party. This term sheet may be assigned by OCI to any subsidiary corporation or partnership (the Borrowing Party). The financing shall be subject to the following terms and conditions: 1. The maximum financing shall be equal to 70% of appraised fair market value for operating properties and 50% of appraised fair market value for undeveloped land inventory properties. 2. Interest shall be payable at an annual interest rate of 5% per annum, compounded annually. 3. A financing fee of 2% of the value of the loan shall be payable upon the closing of the loan. This amount will be deducted from the principal of the loan. 4. The Borrowing Party shall spend a minimum of 0.5% of the value of the property on incremental annual property improvements (that is, capital additions to class 1 buildings) commencing in Year 2. These improvements shall be in addition to regular maintenance and repairs currently deducted in the determination of the existing NOI. 5. A forecast of the capital cost allowance deduction available for the first two years of the Borrowing Party's operations shall be provided by OCI in advance of the notes being issued APPENDIX IV LAND TRANSFER TAX RATES 1. British Columbia levies a land transfer tax at the rate of 2.5% on all properties in the province. 2. Land transfer tax in Nova Scotia is levied by the municipality instead of the province. Halifax levies a land transfer tax at the rate of 1.5% on all properties. 3. Ontario levies no land transfer tax on the first $50,000 of value; it levies 1% on the next $350,000 of value and 2% thereafter. 4. There are no exemptions for transfers of property within a related group of companies. Land Transfer Tax is applicable to the total value of the property (land and building), not just the portion allocated to land. Instructions Please prepare case report outlining all taxation issues. It is September 17, 2022, and you, CPA, work as the senior tax analyst for OCI Inc. (OCI). OCI is an electronics retailer and its shares are traded on the Toronto Stock Exchange. Part of its success has been through partially financing real estate developers during the construction of new strip malls and by owning its own real estate. You have completed a meeting with your boss, Chad Bowie, the vice-president of finance, to discuss the financing of a proposed expansion. OCI requires $45 million in financing to complete this expansion. "We've done all of our financial and tax diligence around the purchase, so we don't need to look at those elements of the project," said Chad. "I need to finalize the financing. I would like to leverage our real estate portfolio but limit the security to the real estate itself. Our bank has indicated the best way to achieve this is to move the real estate into a new wholly-owned corporation ("RealCo"). We could get more financing by leveraging these properties than we could with traditional mortgages. I'd like you to look at a few things for me. I will send you an e-mail shortly with my specific requests." (Appendix I) APPENDIX I E-MAIL FROM CHAD BOWIE From: C Bowie To: CPA Re: Requests for proposed transaction The OCI real estate portfolio has grown in value over a number of years. This type of real estate is usually valued through a capitalization rate method, by capitalizing the property's net operating income (NOI) before tax to determine the fair market value for the total property (land plus building). The NOI of a property consists of the cash income for a property and excludes depreciation. The NOI and capitalization rate for each property are attached (Appendix II). We generally assume that land is worth 30% of the value of the total property. I would like you to address the following: The financing term sheet (Appendix III) bases the financing on the fair market value of the properties moved into RealCo. I need you to determine if the loan will provide us with enough cash to fund our expansion after paying the land transfer tax and financing fees. Land transfer tax rates are in Appendix IV. Are there any assets that will not qualify to be transferred to RealCo without incurring immediate income tax? If so, which one(s) will not qualify and how will we transfer them? I hope at least some of the assets can be transferred to RealCo on a tax-free or tax-deferred basis. If so, please explain what provisions in the Income Tax Act allow for this, and generally how the transaction would be structured. For the assets that can be transferred without incurring immediate income tax, how will the transfer price for tax purposes be determined? What will deadline for filing any elections that may be required? Once you have explained this, please draft any tax elections that may be required with respect to the transfer by calculating the amounts at which the assets will be transferred and the consideration that will be taken back. Include the precise numbers to use on the forms. We will make the acquisition directly through RealCo, so there is no need to discuss how to get the money out of RealCo once the loan is received. The bank has an additional request. I'd like you to prepare the forecast of capital cost allowance deduction available in the first two years in item number 5 of their term sheet. I'd like to have RealCo incorporated on October 1, 2022. To simplify financial reporting, RealCo will have a year-end of December 31. Also hope you can tell me the tax treatment of some specific items I have identified for RealCo (Appendix V) - will they all be treated the same for tax as for accounting? APPENDIX II: Property I, Toronto, ON Land Building Property II, Kelowna, BC Land Inventory Property III, Vancouver, BC Land Building Property IV, Halifax, NS Land Building Capitalization Rate 6.5% 5.0% ΝΟΙ $3,900 N/A $850 Cost $16,200 $38,000 $2,500 $3,000 $8,000 $5,000 $9,000 * Property IV is located in a suburb with declining property values. Due to the unique location of this property, we had it valued by a local real estate professional who determined that the value of the land is $4,000 and the value of the building is $7,175. Other information Property II was originally acquired in 2013 to support the possibility of a future expansion to Kelowna. The land is currently zoned as residential and no applications have been filed to change this as there is no immediate plan to open a store in Kelowna. Omega (or RealCo) may sell the land if the right offer is received. It is currently listed for sale through a realtor at a price of $8,000. OCI's undepreciated capital cost (UCC) of all Class 1 pooled assets, including other buildings that will not be transferred to RealCo, is $94,500 as at December 31, 2014. APPENDIX III FINANCING TERM SHEET The Lender shall provide OCI) with term notes with a floating charge over all assets of the Borrowing Party. This term sheet may be assigned by OCI to any subsidiary corporation or partnership (the Borrowing Party). The financing shall be subject to the following terms and conditions: 1. The maximum financing shall be equal to 70% of appraised fair market value for operating properties and 50% of appraised fair market value for undeveloped land inventory properties. 2. Interest shall be payable at an annual interest rate of 5% per annum, compounded annually. 3. A financing fee of 2% of the value of the loan shall be payable upon the closing of the loan. This amount will be deducted from the principal of the loan. 4. The Borrowing Party shall spend a minimum of 0.5% of the value of the property on incremental annual property improvements (that is, capital additions to class 1 buildings) commencing in Year 2. These improvements shall be in addition to regular maintenance and repairs currently deducted in the determination of the existing NOI. 5. A forecast of the capital cost allowance deduction available for the first two years of the Borrowing Party's operations shall be provided by OCI in advance of the notes being issued APPENDIX IV LAND TRANSFER TAX RATES 1. British Columbia levies a land transfer tax at the rate of 2.5% on all properties in the province. 2. Land transfer tax in Nova Scotia is levied by the municipality instead of the province. Halifax levies a land transfer tax at the rate of 1.5% on all properties. 3. Ontario levies no land transfer tax on the first $50,000 of value; it levies 1% on the next $350,000 of value and 2% thereafter. 4. There are no exemptions for transfers of property within a related group of companies. Land Transfer Tax is applicable to the total value of the property (land and building), not just the portion allocated to land. Instructions Please prepare case report outlining all taxation issues.

Expert Answer:

Related Book For

Modern Advanced Accounting in Canada

ISBN: 978-1259087554

7th edition

Authors: Hilton Murray, Herauf Darrell

Posted Date:

Students also viewed these accounting questions

-

The price-earnings ratios for all companies whose shares are traded on the Tokyo Stock Exchange follow a normal distribution with a standard deviation of 3.5. A random sample of these companies is...

-

You just returned from a meeting with your bank loan officer, and you were a little taken aback by his comments. You've been doing business with this bank for a number of years, and the officer...

-

A mining company listed on the Toronto Stock Exchange is considering a merger with another company. The CEO thinks that the probability of the deal being acceptable to his shareholders is 0.9. He has...

-

The tasks must you complete as part of building the subledger applications while implementing Oracle Accounting Hub Cloud? Explain.

-

Jims Music Company uses LIFO for inventory, and the companys profits are quite high this year. The cost of the inventory has been steadily rising all year, and Jim is worried about his taxes. His...

-

Describe the three main techniques used to manipulate revenue.

-

By using six factor formula for \(k\), derive the Eqs. (7.93), (7.94) of Section 7.7.1. dkoo dp= k MB dM dB 8 + (7.93) 1+M B M B2

-

Below are comparative balance sheets for the Gilmour Company. Instructions(a) Prepare a comparative balance sheet of Gilmour Company showing the percent each item is of the total assets or total...

-

Making Decisions with Confidence Intervals Assume you work for Kimberly Clark Corporation, the makers of Kleenex. The job you are presently working on requires you to decide how many Kleenexes are to...

-

Liquid reaction A --> 2B is taking place in a steady state packed bed reactor that has total available packing area (A) of 10 m. The density (p) and packing surface (a) of the catalyst per volume are...

-

KeyCite the following case: Parker v. State of Oklahoma, 556 P.2d 1298 (Okla. Crim. App. 1976). A) How many citing references does the case provide? B) Has a Maryland case cited the Parker case? If...

-

2."While proportional representation may seem more democratic, in practice it makes it harder to form majority governments and obscures the connection between voters and representatives. This makes...

-

Use subquery to display all employees, in department location 'BOSTON' with a salary of greater than $1000.

-

United Charities annual fund-raising drive in 2016 raised pledges of $1,200,000 of which $800,000 were collected in 2016 and $200,000 were collected in 2017. United Charities estimates $150,000 of...

-

Give an example of where session management should be used in an online application. Web pages are typically requested distinctly and not as a group or even identified by user. How does this feature...

-

In the space below, draft an email in response. Your email must include the following: - Request for Documents of ownership, e . g . Council rates, water bill - Identify four ( 4 ) key features or...

-

An insurance contract has a straight deductible worth 100BD, additionally it also has a coinsurance agreement which specifies that a 40% coinsurance clause exists on a car valued at 27,799 BD. Based...

-

Which of the following streaming TV devices does not involve use of a remote controller? A) Google Chromecast B) Apple TV C) Amazon Fire TV D) Roku

-

Differentiate between the accounting for a fair value hedge and a cash flow hedge.

-

Financial statements of Par Corp. and its subsidiary Star Inc. on December 31, Year 12, are shown below: Other Information ¢ On January 1, Year 5, the balance sheet of Star showed the following...

-

Planet Publishing Limited (Planet) is a medium-sized, privately owned Canadian company that holds exclusive Canadian distribution rights for the publications of Typset Daily Corporation (TDC). Space...

-

On June 3, 2019, Catherine Shanahan received an unsolicited phone call on her cell phone. When she answered, she heard a prerecorded voice message advertising extended automobile warranties (Service...

-

John Whalen was employed by the City of Binghamton as the director of Parks and Recreation. In his capacity as the director, Whalen was to collect various fees and was entrusted with related funds....

-

On August 14, 2018, Jane Doe asked her boyfriend to call an Uber for her as Does phone had low battery. Does boyfriend was not with her, so she did not know which driver Uber had assigned to pick her...

Study smarter with the SolutionInn App