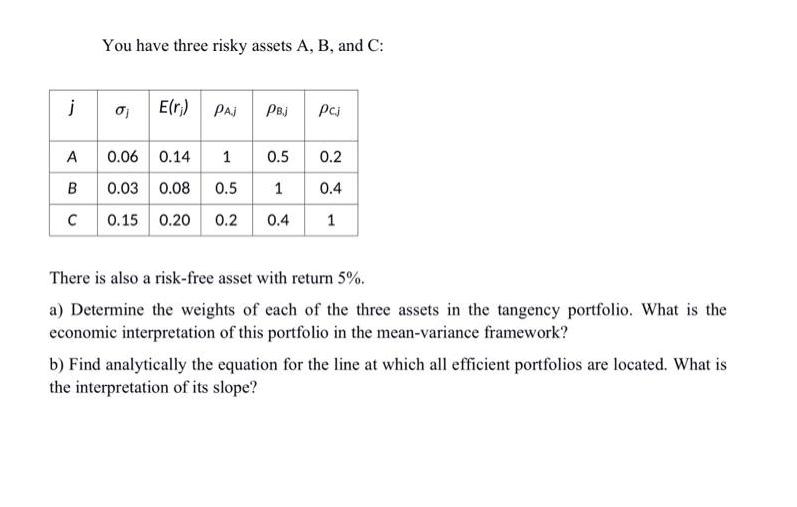

Question: j A B You have three risky assets A, B, and C: 01 E(r;) PAJ PB.j Pcj 0.06 0.14 1 0.5 0.2 0.03 0.08

j A B You have three risky assets A, B, and C: 01 E(r;) PAJ PB.j Pcj 0.06 0.14 1 0.5 0.2 0.03 0.08 0.5 1 0.4 0.15 0.20 0.2 0.4 1 There is also a risk-free asset with return 5%. a) Determine the weights of each of the three assets in the tangency portfolio. What is the economic interpretation of this portfolio in the mean-variance framework? b) Find analytically the equation for the line at which all efficient portfolios are located. What is the interpretation of its slope?

Step by Step Solution

3.52 Rating (165 Votes )

There are 3 Steps involved in it

ANSWER To find the weights of each asset ... View full answer

Get step-by-step solutions from verified subject matter experts