THE CLASSIC PEN COMPANY Jane Dempsey, controller of the Classic Pen Company, was concerned about the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

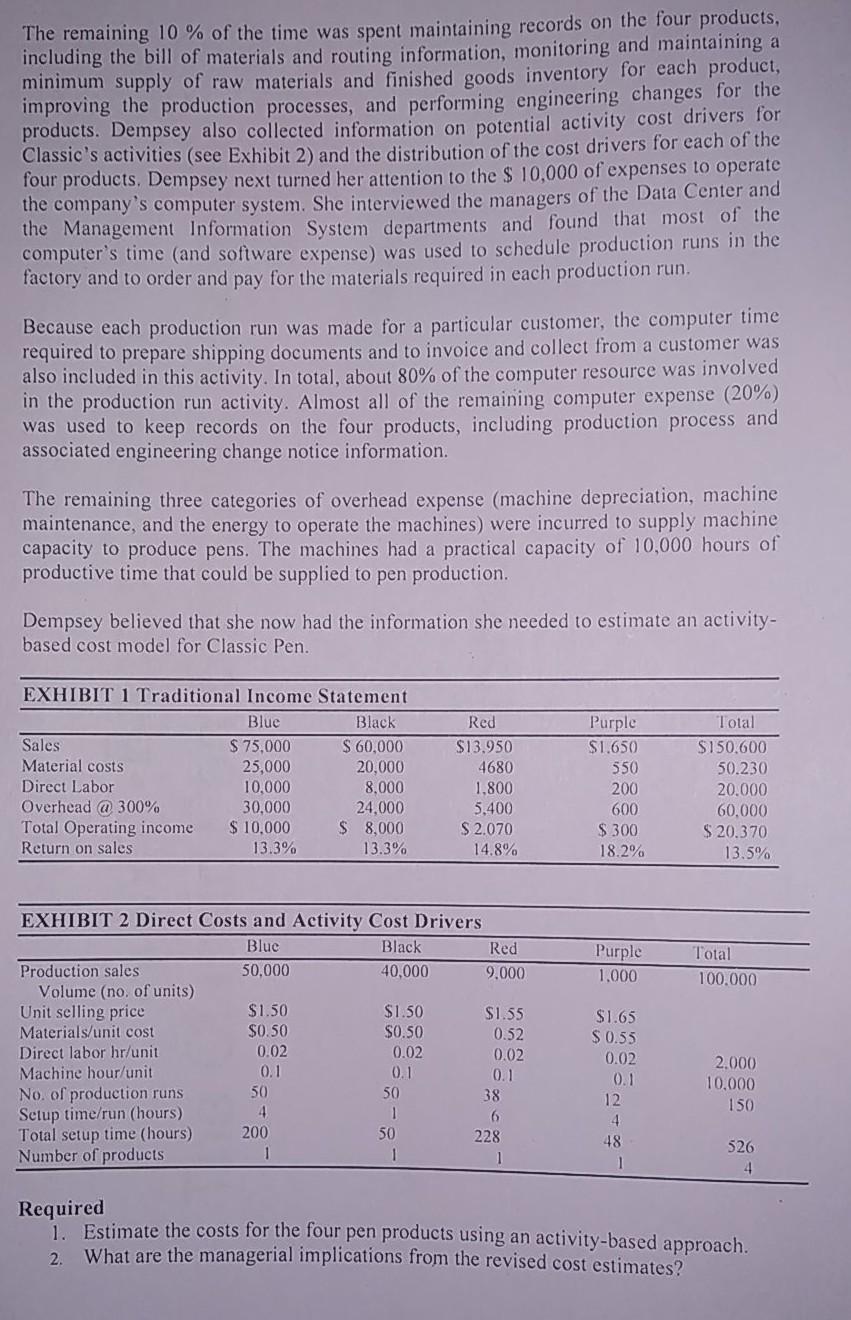

THE CLASSIC PEN COMPANY Jane Dempsey, controller of the Classic Pen Company, was concerned about the recent financial trends in operating results. Classic Pen had been the low-cost producer of traditional BLUE pens and BLACK pens. Profit margins were over 20% of sales. Several years earlier Dennis Selmor, the sales manager, had seen opportunities to expand the business by extending the product line into new products that offered premium selling prices over traditional BLUE and BLACK pens. Five years earlier, RED pens had been introduced; they required the same basic production technology but could be sold at a 3% premium. And last year, PURPLE pens had been introduced because of the 10% premium in selling price they could command. But Dempsey had just seen the financial results (see Exhibit 1) for the most recent fiscal year and was keenly disappointed. The new RED and PURPLE pens do seen more profitable than our BLUE and BLACK pens, but overall profitability is down, and even the new products are not earning the margins we used to see from our traditional products. Perhaps this is the tougher global competition I have been reading about. At least the new line, particularly PURPLE pens, is showing much higher margins. Perhaps we should follow Dennis's advice and introduce even more specially colored pens. Dennis claims that consumers are willing to pay higher prices for these specialty colors. Jeffrey Donald, the manufacturing manager, was also reflecting on the changed environment at Classic Pen: Five years ago, life was a lot simpler. We produced just BLUE and BLACK pens in long production runs, and everything ran smoothly, without much intervention. Difficulties started when the RED pens were introduced and we had to make more change vats, clean out all remnants of the previous color, and then start the production of the red ink. Making black ink was simple; we didn't even have to clean out the residual blue ink from the previous run if we just dumped in enough black ink to cover it up. But for the RED pens, even small traces of the blue or black ink created quality problems. And the ink for the new PURPLE pens also has demanding specifications, but not quite as demanding as for RED pens. vers. This required us to stop production, empty the We seem to be spending a lot more time on purchasing and scheduling activities and just keeping track of where we stand on existing, backlogged, and future orders. The new computer system we got last year helped a lot to reduce the confusion. But I am concerned about rumors I keep hearing that even more new colors may be introduced in the near future. I don't think we have any more capability to handle additional confusion and complexity in our operations. Operations Classic produced pens in a single factory. The major task was preparing and mixing the ink for the different-colored pens. The ink was inserted into the pens in a semi-automated process. A final packing and shipping stage was performed manually. Each product had a bill of materials that identified the quantity and cost of direct materials required for the product. A routing sheet identified the sequence of operations required for each operating step. This information was used to calculate the labor expenses for each of the four products. All of the plant's indirect expenses were aggregated at the plant level and allocated to products on the basis of their direct labor content. Currently, this overhead burden rate was 300 % of direct labor cost. Most people in the plant recalled that not too many years ago the overhead rate was only 200%. Activity-Based Costing Jane Dempsey had recently attended a seminar of her professional organization in which a professor had talked about a new concept, called activity-based costing (ABC). This concept seemed to address many of the problems she had been seeing at Classic. The speaker had even used an example that seemed to capture Classic's situation exactly. The professor had argued that overhead should not be viewed as a cost or a burden to be allocated on top of direct labor. Rather, the organization should focus on activities performed by the indirect and support resource of the organization and try to link the cost of performing these activities directly to the products for which they were performed. Dempsey obtained several books and articles on the subject and soon tried to put into practice the message she had heard and read about. Activity-Based Cost Analysis Dempsey first identified six categories of support expenses that were currently being allocated to pen production: EXPENSE CATEGORY EXPENSE Indirect Labor $ 20,000 Fringe benefits Computer Systems Machinery Maintenance 16,000 10,000 8,000 4,000 Energy 2,000 Total $ 60,000 She determined that the fringe benefits were 40% of labor expenses (both direet and indirect) and would thus represent just a percentage markup to be applied on top of direct and indirect labor charges. Dempsey interviewed department heads in charge of indirect labor and found that three main activities accounted for their work. About half of indirect labor was involved in scheduling or handling production runs. This proportion included scheduling production orders; purchasing, preparing, and releasing materials for the production run; performing a first-item inspection every time the process was changed over and some scrap loss at the beginning of each run until the process settled down. Another 40% of indirect labor was required just for the physical changeover from one color pen to another. The time to change over to BLACK pens was relatively short (about 1 hour) since the previous color did not have to be completely eliminated from the machinery. Other colors required longer changeover times; RED pens required the most extensive changeover to meet the demanding quality specification for this color. The remaining 10 % of the time was spent maintaining records on the four products, including the bill of materials and routing information, monitoring and maintaining a minimum supply of raw materials and finished goods inventory for each product, improving the production processes, and performing engineering changes for the products. Dempsey also collected information on potential activity cost drivers for Classic's activities (see Exhibit 2) and the distribution of the cost drivers for each of the four products. Dempsey next turned her attention to the $ 10,000 of expenses to operate the company's computer system. She interviewed the managers of the Data Center and the Management Information System departments and found that most of the computer's time (and software expense) was used to schedule production runs in the factory and to order and pay for the materials required in each production run. Because each production run was made for a particular customer, the computer time required to prepare shipping documents and to invoice and collect from a customer was also included in this activity. In total, about 80% of the computer resource was involved in the production run activity. Almost all of the remaining computer expense (20%) was used to keep records on the four products, including production process and associated engineering change notice information. The remaining three categories of overhead expense (machine depreciation, machine maintenance, and the energy to operate the machines) were incurred to supply machine capacity to produce pens. The machines had a practical capacity of 10,000 hours of productive time that could be supplied to pen production. Dempsey believed that she now had the information she needed to estimate an activity- based cost model for Classic Pen. EXHIBIT 1 Traditional Income Statement Blue Black Red Purple Total Sales Material costs S 60,000 20,000 $ 75,000 25,000 10,000 30,000 $ 10,000 $13,950 $1.650 $150.600 50.230 20.000 4680 550 Direct Labor 1,800 5,400 $ 2.070 8,000 200 Overhead @ 300% Total Operating income Return on sales 24,000 $ 8,000 13.3% 600 $300 18.2% 60,000 $ 20.370 13.5% 13.3% 14.8% EXHIBIT 2 Direct Costs and Activity Cost Drivers Blue Black Red Purple Total Production sales Volume (no. of units) Unit selling price Materials/unit cost 50,000 40,000 9.000 1,000 100.000 $1.50 $1.50 $0.50 S1.55 S1.65 $0.55 $0.50 0.52 Direct labor hr/unit 0.02 0.02 0.02 0.02 2,000 10.000 0.1 Machine hour/unit No. of production runs Setup time/run (hours) Total setup time (hours) Number of products 0.1 0.1 0.1 50 50 38 12 150 4. 4. 200 50 228 48 526 1 1 4 Required 1. Estimate the costs for the four pen products using an activity-based approach. 2. What are the managerial implications from the revised cost estimates? THE CLASSIC PEN COMPANY Jane Dempsey, controller of the Classic Pen Company, was concerned about the recent financial trends in operating results. Classic Pen had been the low-cost producer of traditional BLUE pens and BLACK pens. Profit margins were over 20% of sales. Several years earlier Dennis Selmor, the sales manager, had seen opportunities to expand the business by extending the product line into new products that offered premium selling prices over traditional BLUE and BLACK pens. Five years earlier, RED pens had been introduced; they required the same basic production technology but could be sold at a 3% premium. And last year, PURPLE pens had been introduced because of the 10% premium in selling price they could command. But Dempsey had just seen the financial results (see Exhibit 1) for the most recent fiscal year and was keenly disappointed. The new RED and PURPLE pens do seen more profitable than our BLUE and BLACK pens, but overall profitability is down, and even the new products are not earning the margins we used to see from our traditional products. Perhaps this is the tougher global competition I have been reading about. At least the new line, particularly PURPLE pens, is showing much higher margins. Perhaps we should follow Dennis's advice and introduce even more specially colored pens. Dennis claims that consumers are willing to pay higher prices for these specialty colors. Jeffrey Donald, the manufacturing manager, was also reflecting on the changed environment at Classic Pen: Five years ago, life was a lot simpler. We produced just BLUE and BLACK pens in long production runs, and everything ran smoothly, without much intervention. Difficulties started when the RED pens were introduced and we had to make more change vats, clean out all remnants of the previous color, and then start the production of the red ink. Making black ink was simple; we didn't even have to clean out the residual blue ink from the previous run if we just dumped in enough black ink to cover it up. But for the RED pens, even small traces of the blue or black ink created quality problems. And the ink for the new PURPLE pens also has demanding specifications, but not quite as demanding as for RED pens. vers. This required us to stop production, empty the We seem to be spending a lot more time on purchasing and scheduling activities and just keeping track of where we stand on existing, backlogged, and future orders. The new computer system we got last year helped a lot to reduce the confusion. But I am concerned about rumors I keep hearing that even more new colors may be introduced in the near future. I don't think we have any more capability to handle additional confusion and complexity in our operations. Operations Classic produced pens in a single factory. The major task was preparing and mixing the ink for the different-colored pens. The ink was inserted into the pens in a semi-automated process. A final packing and shipping stage was performed manually. Each product had a bill of materials that identified the quantity and cost of direct materials required for the product. A routing sheet identified the sequence of operations required for each operating step. This information was used to calculate the labor expenses for each of the four products. All of the plant's indirect expenses were aggregated at the plant level and allocated to products on the basis of their direct labor content. Currently, this overhead burden rate was 300 % of direct labor cost. Most people in the plant recalled that not too many years ago the overhead rate was only 200%. Activity-Based Costing Jane Dempsey had recently attended a seminar of her professional organization in which a professor had talked about a new concept, called activity-based costing (ABC). This concept seemed to address many of the problems she had been seeing at Classic. The speaker had even used an example that seemed to capture Classic's situation exactly. The professor had argued that overhead should not be viewed as a cost or a burden to be allocated on top of direct labor. Rather, the organization should focus on activities performed by the indirect and support resource of the organization and try to link the cost of performing these activities directly to the products for which they were performed. Dempsey obtained several books and articles on the subject and soon tried to put into practice the message she had heard and read about. Activity-Based Cost Analysis Dempsey first identified six categories of support expenses that were currently being allocated to pen production: EXPENSE CATEGORY EXPENSE Indirect Labor $ 20,000 Fringe benefits Computer Systems Machinery Maintenance 16,000 10,000 8,000 4,000 Energy 2,000 Total $ 60,000 She determined that the fringe benefits were 40% of labor expenses (both direet and indirect) and would thus represent just a percentage markup to be applied on top of direct and indirect labor charges. Dempsey interviewed department heads in charge of indirect labor and found that three main activities accounted for their work. About half of indirect labor was involved in scheduling or handling production runs. This proportion included scheduling production orders; purchasing, preparing, and releasing materials for the production run; performing a first-item inspection every time the process was changed over and some scrap loss at the beginning of each run until the process settled down. Another 40% of indirect labor was required just for the physical changeover from one color pen to another. The time to change over to BLACK pens was relatively short (about 1 hour) since the previous color did not have to be completely eliminated from the machinery. Other colors required longer changeover times; RED pens required the most extensive changeover to meet the demanding quality specification for this color. The remaining 10 % of the time was spent maintaining records on the four products, including the bill of materials and routing information, monitoring and maintaining a minimum supply of raw materials and finished goods inventory for each product, improving the production processes, and performing engineering changes for the products. Dempsey also collected information on potential activity cost drivers for Classic's activities (see Exhibit 2) and the distribution of the cost drivers for each of the four products. Dempsey next turned her attention to the $ 10,000 of expenses to operate the company's computer system. She interviewed the managers of the Data Center and the Management Information System departments and found that most of the computer's time (and software expense) was used to schedule production runs in the factory and to order and pay for the materials required in each production run. Because each production run was made for a particular customer, the computer time required to prepare shipping documents and to invoice and collect from a customer was also included in this activity. In total, about 80% of the computer resource was involved in the production run activity. Almost all of the remaining computer expense (20%) was used to keep records on the four products, including production process and associated engineering change notice information. The remaining three categories of overhead expense (machine depreciation, machine maintenance, and the energy to operate the machines) were incurred to supply machine capacity to produce pens. The machines had a practical capacity of 10,000 hours of productive time that could be supplied to pen production. Dempsey believed that she now had the information she needed to estimate an activity- based cost model for Classic Pen. EXHIBIT 1 Traditional Income Statement Blue Black Red Purple Total Sales Material costs S 60,000 20,000 $ 75,000 25,000 10,000 30,000 $ 10,000 $13,950 $1.650 $150.600 50.230 20.000 4680 550 Direct Labor 1,800 5,400 $ 2.070 8,000 200 Overhead @ 300% Total Operating income Return on sales 24,000 $ 8,000 13.3% 600 $300 18.2% 60,000 $ 20.370 13.5% 13.3% 14.8% EXHIBIT 2 Direct Costs and Activity Cost Drivers Blue Black Red Purple Total Production sales Volume (no. of units) Unit selling price Materials/unit cost 50,000 40,000 9.000 1,000 100.000 $1.50 $1.50 $0.50 S1.55 S1.65 $0.55 $0.50 0.52 Direct labor hr/unit 0.02 0.02 0.02 0.02 2,000 10.000 0.1 Machine hour/unit No. of production runs Setup time/run (hours) Total setup time (hours) Number of products 0.1 0.1 0.1 50 50 38 12 150 4. 4. 200 50 228 48 526 1 1 4 Required 1. Estimate the costs for the four pen products using an activity-based approach. 2. What are the managerial implications from the revised cost estimates?

Expert Answer:

Answer rating: 100% (QA)

4 If Classic Pen Company did not switch to ABC costing a It will continue to produce and sell RED and PURPLE at same price as both showing high profit margin under traditional costing and will also tr... View the full answer

Related Book For

Introduction to Financial Accounting

ISBN: 978-0133251036

11th edition

Authors: Charles Horngren, Gary Sundem, John Elliott, Donna Philbrick

Posted Date:

Students also viewed these accounting questions

-

BanhMi2U is a chain of over twenty Vietnamese bread shops in the CBD and around Melbourne. "Banh Mi" is a popular Vietnamese baguette roll stuffed with butter, pate, and a range of fillings (for...

-

Ingrid is planning to expand her business by taking on a new product. She can purchase the new product at a cost of $8. To market this new product, she would need to spend $984 on advertising each...

-

Youre trying to determine whether to expand your business by building a new manufacturing plant. The plant has an installation cost of $12 million, which will be depreciated straight-line to zero...

-

Northland Corporation is a small information-systems consulting firm that specializes in helping companies implement standard sales-management software. The market for Northalndss services is very...

-

A company operated at a profit for the year, but cash flow from operations was negative. Why might this occur? What industry or industries might find this a common occurrence?

-

Not all interest expenses are tax deductible. Home-mortgage payments are interest expenses. Thus, they are not tax deductible. Translate the following arguments into standard-form categorical...

-

A thin, smooth sign is attached to the side of a truck as is indicated in Fig. P9.56. Estimate the friction drag on the sign when the truck is driven at \(55 \mathrm{mph}\). Figure P9.56 5 ft 20 ft...

-

The town of Pleasantville is thinking of building a swimming pool. Building and operating the pool will cost the town $5,000 per day. There are three groups of potential pool users in Pleasantville:...

-

Use logarithmic differentiation to find the derivative of y with respect to the given independent variable. y = (sin 8x)x

-

Hotel DelRay is located at the heart of the city of Brussels, in Belgium. Brussels is a major hub for international politics, a home for several international organizations and diplomats, and a...

-

3. Consider the design data for an axial compressor nestled on machine foundation as shown below. Rocking Design data: Static weight of machinery: 20 tons Rotational speed: 327 rpm Soil density: 18...

-

An alpine glacier is moving downhill at a speed of 10 m per day. Show that the glacier will reach a ranger station 250 m from the glaciers front edge in 25 days.

-

What drives surface currents?

-

What are the six elements of weather?

-

Why are summer days warmer than winter days (on average)?

-

The highest dew point ever recorded was 95F, recorded in Saudi Arabia. Was the air humid or dry at that time? Explain your reasoning.

-

Based on their conversation, Daniel plans to provide Amy with conflict consulting. Select the true statement about conflict consulting. Conflict consulting is a way that an intervener can teach...

-

Cleaning Service Company's Trial Balance on December 31, 2020 is as follows: Account name Debit Credit Cash 700 Supplies Pre-paid insurance Pre-paid office rent Equipment Accumulated depreciation -...

-

URS Corporation is an integrated engineering, construction, and technical services company that operates in nearly 50 countries. According to the company Web site, URS offers program management,...

-

Swahili Imports uses a periodic inventory system. Prepare journal entries for the following summarized transactions for 20X1 (omit explanations). For simplicity, assume the beginning and ending...

-

List five internal control procedures used to safeguard cash.

-

Isothermal compression efficiency can be achieved by running the compressor: (a) At a very high speed (b) At a very slow speed (c) At an average speed (d) At zero speed

-

Derive the expression of work done by the compressor in isothermal compression, adiabatic compression, and polytropic compression.

-

Maximum work is done in compressing air when the compression is: (a) Isothermal compression (b) Adiabatic compression (c) Polytropic compression (d) None of these

Study smarter with the SolutionInn App