January 1, 20x3, parent held merchandise acquired from subsidiary for $50,000 during 20x3, subsidiary sold merchandise to

Question:

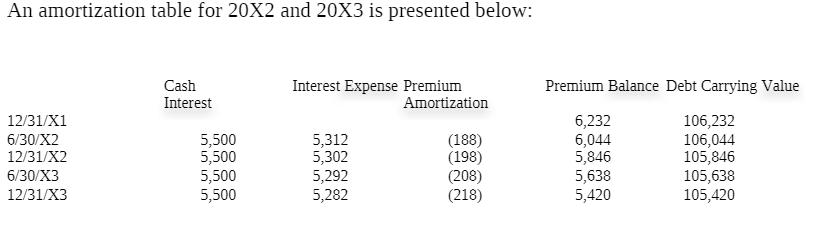

January 1, 20x3, parent held merchandise acquired from subsidiary for $50,000 during 20x3, subsidiary sold merchandise to Parent for $120,000, of which Parent holds $30,000 on December 31, 20X3. Subsidiary's gross profit on sales is 40%. On December 31, 20X3, Parent still owes Subsidiary $5,000 for merchandise. On December 31, 20X1, Parent sold $100,000 par value of 11%, 10-year bonds for $106,232, which resulted in an effective interest rate of 10%. The bonds pay interest semi-annually on June 30 and December 31. Parent uses the effective-interest method of amortization for the premium.

On December 31, 20X2, Subsidiary repurchased $50,000 par value of the bonds, paying a price equal to par. The bonds are still held on December 31, 20X3.

On December 31, 20X2, Subsidiary repurchased $50,000 par value of the bonds, paying a price equal to par. The bonds are still held on December 31, 20X3.

On December 31, 20X3, Parent sold equipment with a cost of $50,000 and accumulated depreciation of $30,000 to Subsidiary for $40,000. Subsidiary will use the equipment beginning in 20X4.

Required:

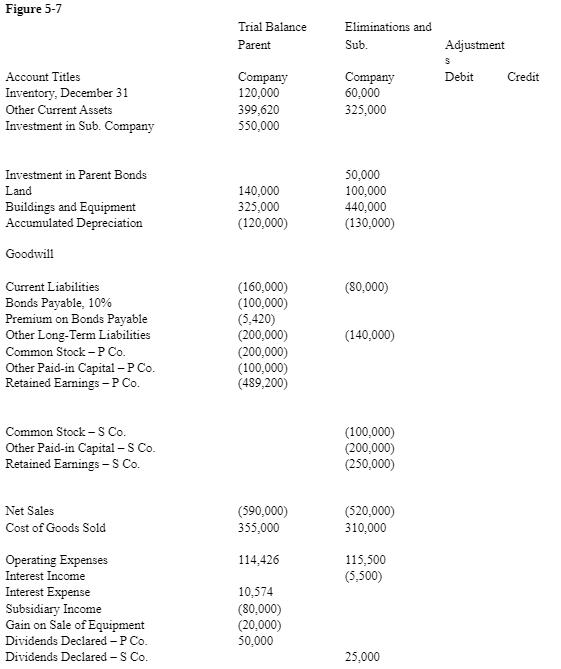

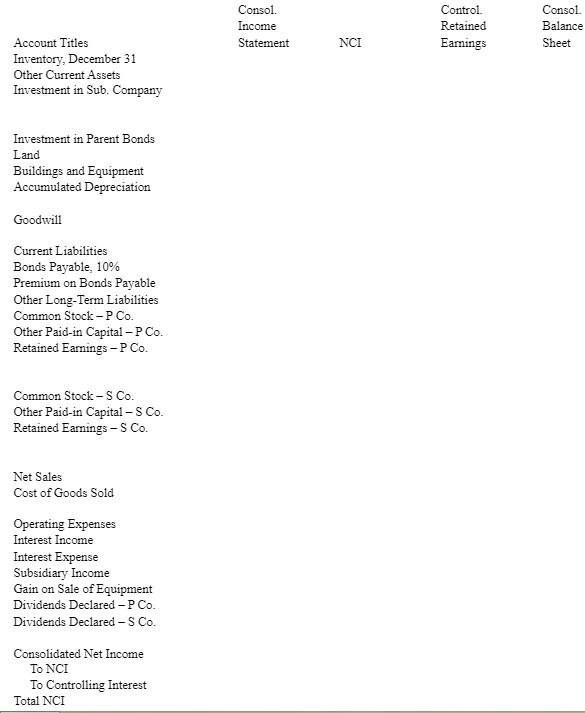

Complete the Figure 5-7 worksheet for consolidated financial statements for the year ended December 31, 20X3. Round all computations to the nearest dollar.

Expert Answer:

Advanced Financial Accounting

ISBN: 978-0132928939

7th edition

Authors: Thomas H. Beechy, V. Umashanker Trivedi, Kenneth E. MacAulay