Jay Pritchett Estate Planning for a Modern Family 175 Points Jay and Gloria Pritchett Case Jay...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

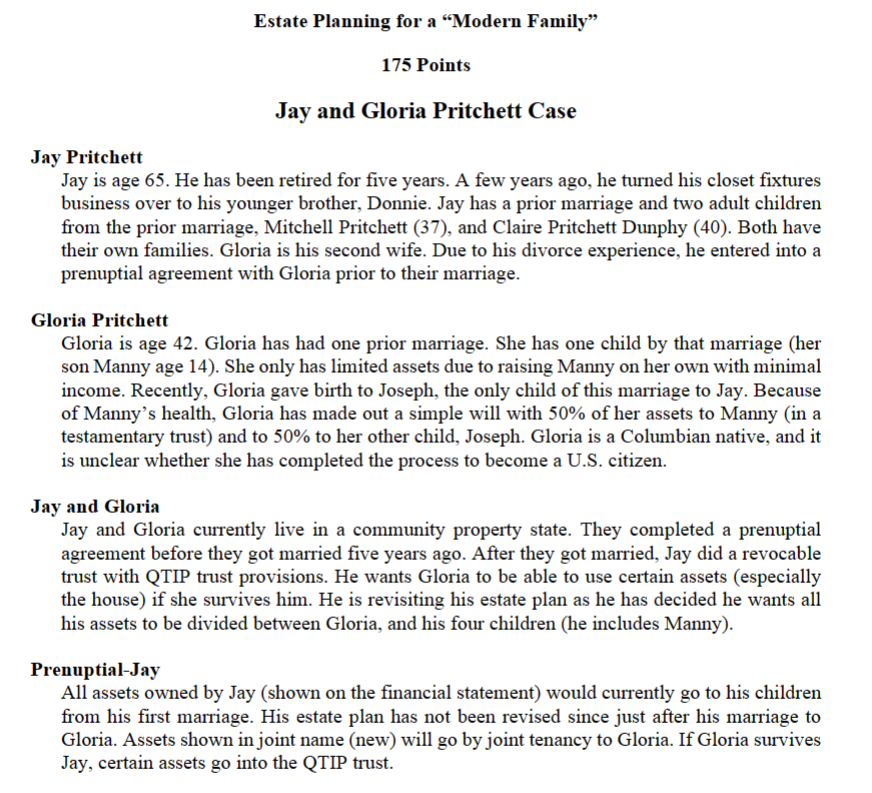

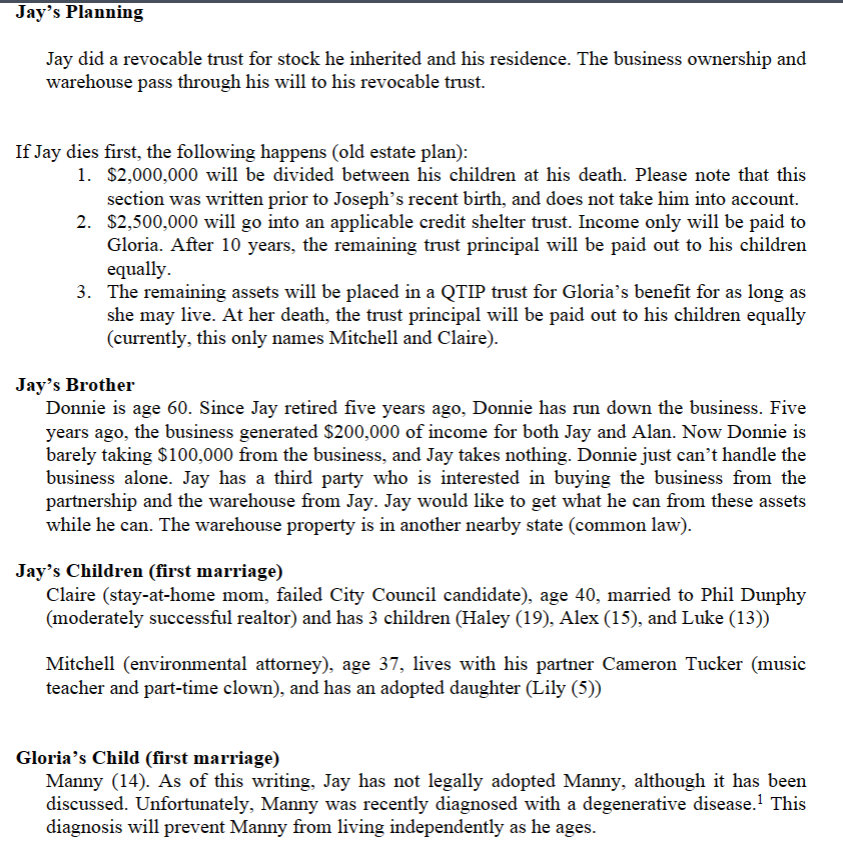

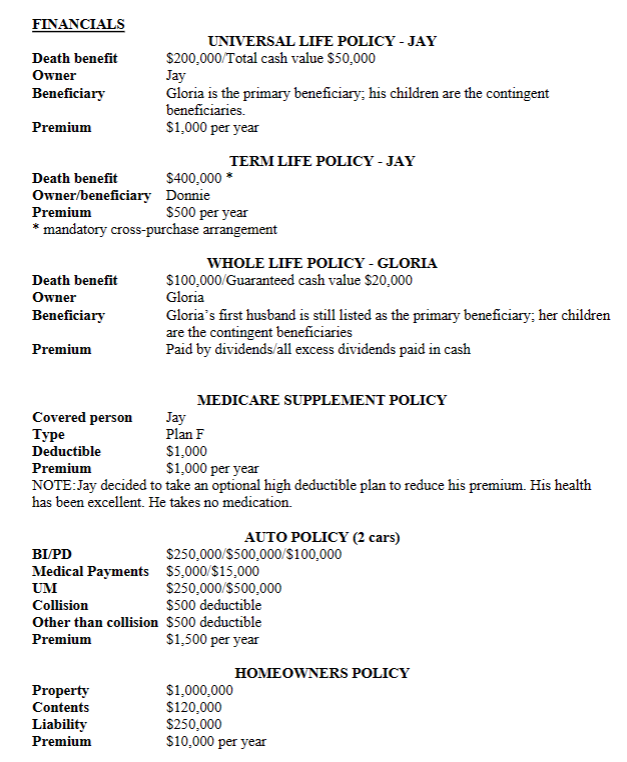

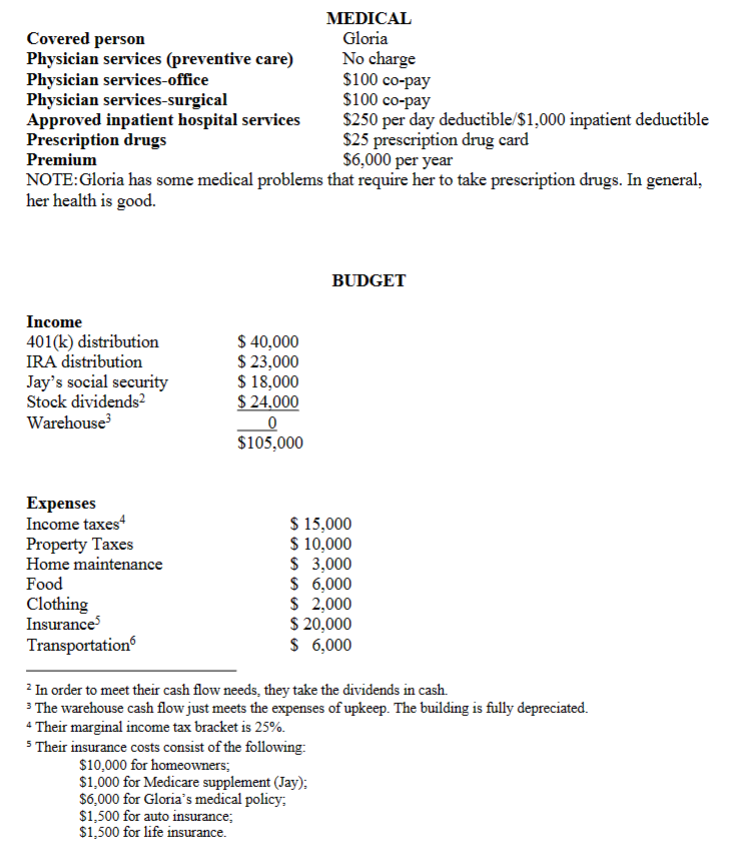

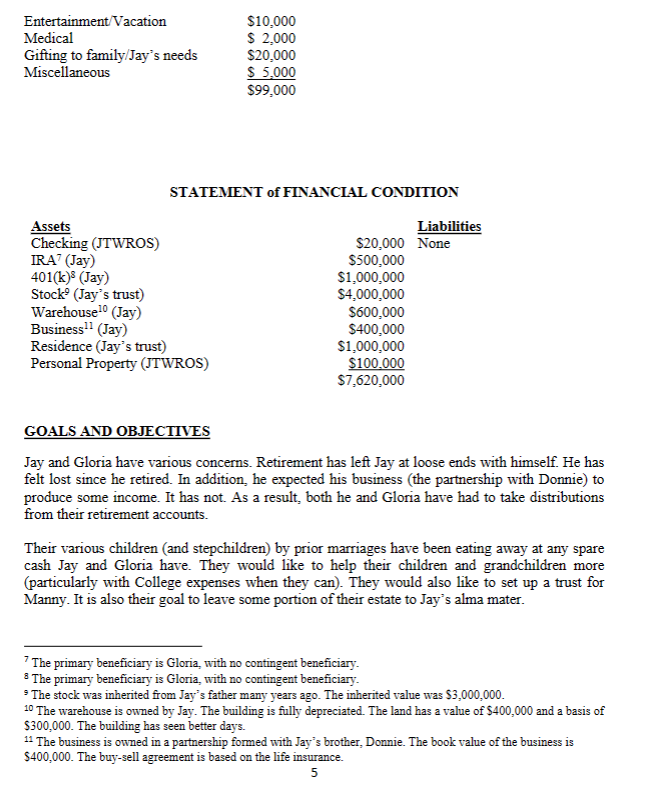

Jay Pritchett Estate Planning for a "Modern Family" 175 Points Jay and Gloria Pritchett Case Jay is age 65. He has been retired for five years. A few years ago, he turned his closet fixtures business over to his younger brother, Donnie. Jay has a prior marriage and two adult children from the prior marriage, Mitchell Pritchett (37), and Claire Pritchett Dunphy (40). Both have their own families. Gloria is his second wife. Due to his divorce experience, he entered into a prenuptial agreement with Gloria prior to their marriage. Gloria Pritchett Gloria is age 42. Gloria has had one prior marriage. She has one child by that marriage (her son Manny age 14). She only has limited assets due to raising Manny on her own with minimal income. Recently, Gloria gave birth to Joseph, the only child of this marriage to Jay. Because of Manny's health, Gloria has made out a simple will with 50% of her assets to Manny (in a testamentary trust) and to 50% to her other child, Joseph. Gloria is a Columbian native, and it is unclear whether she has completed the process to become a U.S. citizen. Jay and Gloria Jay and Gloria currently live in a community property state. They completed a prenuptial agreement before they got married five years ago. After they got married, Jay did a revocable trust with QTIP trust provisions. He wants Gloria to be able to use certain assets (especially the house) if she survives him. He is revisiting his estate plan as he has decided he wants all his assets to be divided between Gloria, and his four children (he includes Manny). Prenuptial-Jay All assets owned by Jay (shown on the financial statement) would currently go to his children from his first marriage. His estate plan has not been revised since just after his marriage to Gloria. Assets shown in joint name (new) will go by joint tenancy to Gloria. If Gloria survives Jay, certain assets go into the QTIP trust. Jay's Planning Jay did a revocable trust for stock he inherited and his residence. The business ownership and warehouse pass through his will to his revocable trust. If Jay dies first, the following happens (old estate plan): 1. $2,000,000 will be divided between his children at his death. Please note that this section was written prior to Joseph's recent birth, and does not take him into account. 2. $2,500,000 will go into an applicable credit shelter trust. Income only will be paid to Gloria. After 10 years, the remaining trust principal will be paid out to his children equally. 3. The remaining assets will be placed in a QTIP trust for Gloria's benefit for as long as she may live. At her death, the trust principal will be paid out to his children equally (currently, this only names Mitchell and Claire). Jay's Brother Donnie is age 60. Since Jay retired five years ago, Donnie has run down the business. Five years ago, the business generated $200,000 of income for both Jay and Alan. Now Donnie is barely taking $100,000 from the business, and Jay takes nothing. Donnie just can't handle the business alone. Jay has a third party who is interested in buying the business from the partnership and the warehouse from Jay. Jay would like to get what he can from these assets while he can. The warehouse property is in another nearby state (common law). Jay's Children (first marriage) Claire (stay-at-home mom, failed City Council candidate), age 40, married to Phil Dunphy (moderately successful realtor) and has 3 children (Haley (19), Alex (15), and Luke (13)) Mitchell (environmental attorney), age 37, lives with his partner Cameron Tucker (music teacher and part-time clown), and has an adopted daughter (Lily (5)) Gloria's Child (first marriage) Manny (14). As of this writing, Jay has not legally adopted Manny, although it has been discussed. Unfortunately, Manny was recently diagnosed with a degenerative disease. This diagnosis will prevent Manny from living independently as he ages. FINANCIALS Death benefit Owner Beneficiary Premium UNIVERSAL LIFE POLICY - JAY $200,000/Total cash value $50,000 Jay Gloria is the primary beneficiary; his children are the contingent beneficiaries. $1,000 per year Death benefit Premium TERM LIFE POLICY-JAY $400,000 * $500 per year Owner/beneficiary Donnie * mandatory cross-purchase arrangement Death benefit Owner Beneficiary Premium WHOLE LIFE POLICY - GLORIA $100,000/Guaranteed cash value $20,000 Gloria Gloria's first husband is still listed as the primary beneficiary; her children are the contingent beneficiaries Paid by dividends/all excess dividends paid in cash MEDICARE SUPPLEMENT POLICY Covered person Jay Plan F $1,000 Deductible Premium $1,000 per year NOTE:Jay decided to take an optional high deductible plan to reduce his premium. His health has been excellent. He takes no medication. AUTO POLICY (2 cars) BI/PD $250,000/$500,000/$100,000 Medical Payments $5,000/$15,000 UM Collision $250,000/$500,000 $500 deductible Other than collision $500 deductible Premium $1,500 per year HOMEOWNERS POLICY Property $1,000,000 Contents $120,000 Liability $250,000 Premium $10,000 per year Covered person Physician services (preventive care) Physician services-office Physician services-surgical Approved inpatient hospital services Prescription drugs Premium MEDICAL Gloria No charge $100 co-pay $100 co-pay $250 per day deductible/$1,000 inpatient deductible $25 prescription drug card $6,000 per year NOTE: Gloria has some medical problems that require her to take prescription drugs. In general, her health is good. Income 401(k) distribution IRA distribution Jay's social security Stock dividends Warehouse Expenses Income taxes4 $ 40,000 $23,000 $ 18,000 $ 24,000 0 $105,000 BUDGET $ 15,000 Property Taxes $ 10,000 Home maintenance $ 3,000 Food $ 6,000 Clothing $ 2,000 Insurance $ 20,000 Transportation $ 6,000 2 In order to meet their cash flow needs, they take the dividends in cash. 3 The warehouse cash flow just meets the expenses of upkeep. The building is fully depreciated. 4 Their marginal income tax bracket is 25%. 5 Their insurance costs consist of the following: $10,000 for homeowners; $1,000 for Medicare supplement (Jay); $6,000 for Gloria's medical policy; $1,500 for auto insurance; $1,500 for life insurance. Entertainment/Vacation Medical Gifting to family/Jay's needs Miscellaneous $10,000 $ 2,000 $20,000 $ 5,000 $99.000 STATEMENT of FINANCIAL CONDITION Assets Liabilities Checking (JTWROS) $20,000 None IRA7 (Jay) $500,000 401(k) (Jay) $1,000,000 Stock (Jay's trust) $4,000,000 Warehouse 10 (Jay) $600,000 Business (Jay) $400,000 Residence (Jay's trust) $1,000,000 Personal Property (JTWROS) $100.000 $7,620,000 GOALS AND OBJECTIVES Jay and Gloria have various concerns. Retirement has left Jay at loose ends with himself. He has felt lost since he retired. In addition, he expected his business (the partnership with Donnie) to produce some income. It has not. As a result, both he and Gloria have had to take distributions from their retirement accounts. Their various children (and stepchildren) by prior marriages have been eating away at any spare cash Jay and Gloria have. They would like to help their children and grandchildren more (particularly with College expenses when they can). They would also like to set up a trust for Manny. It is also their goal to leave some portion of their estate to Jay's alma mater. 7 The primary beneficiary is Gloria, with no contingent beneficiary. 8 The primary beneficiary is Gloria, with no contingent beneficiary. The stock was inherited from Jay's father many years ago. The inherited value was $3,000,000. 10 The warehouse is owned by Jay. The building is fully depreciated. The land has a value of $400,000 and a basis of $300,000. The building has seen better days. 11 The business is owned in a partnership formed with Jay's brother, Donnie. The book value of the business is $400,000. The buy-sell agreement is based on the life insurance. 5 FPLN 460 - Financial Planning Jay's estate planning and community property issues have left Gloria concerned. All she has in the event of Jay's death under the status quo are life insurance proceeds and the QTIP trust assets, as she has no independent income. Jay has been talking to various financial planners who have been suggesting family limited partnerships, charitable giving, and other gifting arrangements. Gloria feels left out in the planning and asset distributions. Jay and Gloria are both in good health. Their marriage appears to be working out. Financial arrangements and finances seem to be the biggest problem between them. Action items: 1. Calculate the total of the assets that will pass through Jay's Probate Estate if he dies first. 2. Calculate the total of the assets that will be included in Jay's Gross Estate if he dies first. 3. Based on Jay and Gloria's financial information and family status, provide your recommendations that will accommodate their specific estate plan goals. Provide your rationale and the economic benefits of your recommended estate planning vehicles. Take into consideration the cost of implementing the estate planning vehicles. Your analysis should also include a review of the family's assets and expenses, and how your estate planning recommendations will impact their current budget and expenses. Do not forget that either spouse may predecease the other. Jay Pritchett Estate Planning for a "Modern Family" 175 Points Jay and Gloria Pritchett Case Jay is age 65. He has been retired for five years. A few years ago, he turned his closet fixtures business over to his younger brother, Donnie. Jay has a prior marriage and two adult children from the prior marriage, Mitchell Pritchett (37), and Claire Pritchett Dunphy (40). Both have their own families. Gloria is his second wife. Due to his divorce experience, he entered into a prenuptial agreement with Gloria prior to their marriage. Gloria Pritchett Gloria is age 42. Gloria has had one prior marriage. She has one child by that marriage (her son Manny age 14). She only has limited assets due to raising Manny on her own with minimal income. Recently, Gloria gave birth to Joseph, the only child of this marriage to Jay. Because of Manny's health, Gloria has made out a simple will with 50% of her assets to Manny (in a testamentary trust) and to 50% to her other child, Joseph. Gloria is a Columbian native, and it is unclear whether she has completed the process to become a U.S. citizen. Jay and Gloria Jay and Gloria currently live in a community property state. They completed a prenuptial agreement before they got married five years ago. After they got married, Jay did a revocable trust with QTIP trust provisions. He wants Gloria to be able to use certain assets (especially the house) if she survives him. He is revisiting his estate plan as he has decided he wants all his assets to be divided between Gloria, and his four children (he includes Manny). Prenuptial-Jay All assets owned by Jay (shown on the financial statement) would currently go to his children from his first marriage. His estate plan has not been revised since just after his marriage to Gloria. Assets shown in joint name (new) will go by joint tenancy to Gloria. If Gloria survives Jay, certain assets go into the QTIP trust. Jay's Planning Jay did a revocable trust for stock he inherited and his residence. The business ownership and warehouse pass through his will to his revocable trust. If Jay dies first, the following happens (old estate plan): 1. $2,000,000 will be divided between his children at his death. Please note that this section was written prior to Joseph's recent birth, and does not take him into account. 2. $2,500,000 will go into an applicable credit shelter trust. Income only will be paid to Gloria. After 10 years, the remaining trust principal will be paid out to his children equally. 3. The remaining assets will be placed in a QTIP trust for Gloria's benefit for as long as she may live. At her death, the trust principal will be paid out to his children equally (currently, this only names Mitchell and Claire). Jay's Brother Donnie is age 60. Since Jay retired five years ago, Donnie has run down the business. Five years ago, the business generated $200,000 of income for both Jay and Alan. Now Donnie is barely taking $100,000 from the business, and Jay takes nothing. Donnie just can't handle the business alone. Jay has a third party who is interested in buying the business from the partnership and the warehouse from Jay. Jay would like to get what he can from these assets while he can. The warehouse property is in another nearby state (common law). Jay's Children (first marriage) Claire (stay-at-home mom, failed City Council candidate), age 40, married to Phil Dunphy (moderately successful realtor) and has 3 children (Haley (19), Alex (15), and Luke (13)) Mitchell (environmental attorney), age 37, lives with his partner Cameron Tucker (music teacher and part-time clown), and has an adopted daughter (Lily (5)) Gloria's Child (first marriage) Manny (14). As of this writing, Jay has not legally adopted Manny, although it has been discussed. Unfortunately, Manny was recently diagnosed with a degenerative disease. This diagnosis will prevent Manny from living independently as he ages. FINANCIALS Death benefit Owner Beneficiary Premium UNIVERSAL LIFE POLICY - JAY $200,000/Total cash value $50,000 Jay Gloria is the primary beneficiary; his children are the contingent beneficiaries. $1,000 per year Death benefit Premium TERM LIFE POLICY-JAY $400,000 * $500 per year Owner/beneficiary Donnie * mandatory cross-purchase arrangement Death benefit Owner Beneficiary Premium WHOLE LIFE POLICY - GLORIA $100,000/Guaranteed cash value $20,000 Gloria Gloria's first husband is still listed as the primary beneficiary; her children are the contingent beneficiaries Paid by dividends/all excess dividends paid in cash MEDICARE SUPPLEMENT POLICY Covered person Jay Plan F $1,000 Deductible Premium $1,000 per year NOTE:Jay decided to take an optional high deductible plan to reduce his premium. His health has been excellent. He takes no medication. AUTO POLICY (2 cars) BI/PD $250,000/$500,000/$100,000 Medical Payments $5,000/$15,000 UM Collision $250,000/$500,000 $500 deductible Other than collision $500 deductible Premium $1,500 per year HOMEOWNERS POLICY Property $1,000,000 Contents $120,000 Liability $250,000 Premium $10,000 per year Covered person Physician services (preventive care) Physician services-office Physician services-surgical Approved inpatient hospital services Prescription drugs Premium MEDICAL Gloria No charge $100 co-pay $100 co-pay $250 per day deductible/$1,000 inpatient deductible $25 prescription drug card $6,000 per year NOTE: Gloria has some medical problems that require her to take prescription drugs. In general, her health is good. Income 401(k) distribution IRA distribution Jay's social security Stock dividends Warehouse Expenses Income taxes4 $ 40,000 $23,000 $ 18,000 $ 24,000 0 $105,000 BUDGET $ 15,000 Property Taxes $ 10,000 Home maintenance $ 3,000 Food $ 6,000 Clothing $ 2,000 Insurance $ 20,000 Transportation $ 6,000 2 In order to meet their cash flow needs, they take the dividends in cash. 3 The warehouse cash flow just meets the expenses of upkeep. The building is fully depreciated. 4 Their marginal income tax bracket is 25%. 5 Their insurance costs consist of the following: $10,000 for homeowners; $1,000 for Medicare supplement (Jay); $6,000 for Gloria's medical policy; $1,500 for auto insurance; $1,500 for life insurance. Entertainment/Vacation Medical Gifting to family/Jay's needs Miscellaneous $10,000 $ 2,000 $20,000 $ 5,000 $99.000 STATEMENT of FINANCIAL CONDITION Assets Liabilities Checking (JTWROS) $20,000 None IRA7 (Jay) $500,000 401(k) (Jay) $1,000,000 Stock (Jay's trust) $4,000,000 Warehouse 10 (Jay) $600,000 Business (Jay) $400,000 Residence (Jay's trust) $1,000,000 Personal Property (JTWROS) $100.000 $7,620,000 GOALS AND OBJECTIVES Jay and Gloria have various concerns. Retirement has left Jay at loose ends with himself. He has felt lost since he retired. In addition, he expected his business (the partnership with Donnie) to produce some income. It has not. As a result, both he and Gloria have had to take distributions from their retirement accounts. Their various children (and stepchildren) by prior marriages have been eating away at any spare cash Jay and Gloria have. They would like to help their children and grandchildren more (particularly with College expenses when they can). They would also like to set up a trust for Manny. It is also their goal to leave some portion of their estate to Jay's alma mater. 7 The primary beneficiary is Gloria, with no contingent beneficiary. 8 The primary beneficiary is Gloria, with no contingent beneficiary. The stock was inherited from Jay's father many years ago. The inherited value was $3,000,000. 10 The warehouse is owned by Jay. The building is fully depreciated. The land has a value of $400,000 and a basis of $300,000. The building has seen better days. 11 The business is owned in a partnership formed with Jay's brother, Donnie. The book value of the business is $400,000. The buy-sell agreement is based on the life insurance. 5 FPLN 460 - Financial Planning Jay's estate planning and community property issues have left Gloria concerned. All she has in the event of Jay's death under the status quo are life insurance proceeds and the QTIP trust assets, as she has no independent income. Jay has been talking to various financial planners who have been suggesting family limited partnerships, charitable giving, and other gifting arrangements. Gloria feels left out in the planning and asset distributions. Jay and Gloria are both in good health. Their marriage appears to be working out. Financial arrangements and finances seem to be the biggest problem between them. Action items: 1. Calculate the total of the assets that will pass through Jay's Probate Estate if he dies first. 2. Calculate the total of the assets that will be included in Jay's Gross Estate if he dies first. 3. Based on Jay and Gloria's financial information and family status, provide your recommendations that will accommodate their specific estate plan goals. Provide your rationale and the economic benefits of your recommended estate planning vehicles. Take into consideration the cost of implementing the estate planning vehicles. Your analysis should also include a review of the family's assets and expenses, and how your estate planning recommendations will impact their current budget and expenses. Do not forget that either spouse may predecease the other.

Expert Answer:

Related Book For

International Marketing And Export Management

ISBN: 9781292016924

8th Edition

Authors: Gerald Albaum , Alexander Josiassen , Edwin Duerr

Posted Date:

Students also viewed these finance questions

-

The Crazy Eddie fraud may appear smaller and gentler than the massive billion-dollar frauds exposed in recent times, such as Bernie Madoffs Ponzi scheme, frauds in the subprime mortgage market, the...

-

This assignment requires you to complete the 2022 tax reporting for a fictional woman named Anna Smith. Question 1 T1 - step 4 - line 66 This is Anna's taxable income Answer: Question 2 T1 - step...

-

As we continue our discussions regarding revenue's associated with public sector, this will help reinforce some of the ideas regarding taxes on goods and services. Through the next week, save your...

-

A major university hires a famous Texas millionaire to manage its endowment. The millionaire decides to follow this plan each year: Spend 25% of all funds above $100 million on university...

-

Discuss the key features of antisocial personality disorder. b.Discuss the key features of borderline personality disorder. c.Discuss the key features of histrionic personality disorder. d.Discuss...

-

The time to prepare a slide for high-throughput genomics is a Poisson process with a mean of two hours per slide. What is the probability that 10 slides require more than 25 hours to prepare?

-

After the tangible assets have been adjusted to current market prices, the capital accounts of Brandon Newman and Latrell Osbourne have balances of $75,000 and $125,000, respectively. Juan Rivas is...

-

Kilbourne Appliances produces two models of beverage coolers for homes and offices, the KA-15 and the KA-24. Data on operations and costs for March follow. Units produced Machine-hours Direct...

-

Charlene is evaluating a capital budgeting project that should last for 4 years. The project requires $775,000 of equipment and is eligible for 100% bonus depreciation. She is unsure whether...

-

Assume that i, t, x, y, and z are C++ int variables. Refer to the table below for the variables being used and their associated registers. Variable Register 1 1 2 # i = 3 i $to Write the...

-

1) Consider the relation A, with key and functional dependencies shown below. I. What Normal form is A in right now? Why? II. III. What actions would you take to normalize A to the next higher normal...

-

3) Skylar and Skyler are roommates with identical incomes (and similar names). They have $150 to spend on cellphone data (X) and economics books (Y). Their current cellphone provider, Spotty Mobile,...

-

8. Flash memory has some of the properties of ROM (it retains its contents with the power off), and some of the properties of RAM (you can read or write to it). However most types of FLASH memory are...

-

K The table below contains the total cost (in $) for four average-priced tickets, two beers, four soft drinks, four hot dogs, two game programs, two adult-sized caps, and one parking space for 30...

-

From an ethical perspective how do you evaluate the attitude and actions taken by Union Carbide in the aftermath of the tragedy in Bhopal?

-

A stock has had returns of 8 percent, 26 percent, 14 percent, 17 percent, 31 percent, and 1 percent over the last six years. What are the arithmetic and geometric average returns for the stock?

-

What role does the HAL play in the platform?

-

If your logic analyzer is capable of on-the-fly disassembly, use it to display bus activity in the form of instructions, rather than simply 1s and 0s.

-

Draw UML state diagrams for device 1 and device 2 in a four-cycle handshake.

Study smarter with the SolutionInn App