Question: Joint cost allocation; sell or process further In a joint process, Wear Art produces precut fabrics for three products: dresses, jackets, and blouses. Joint

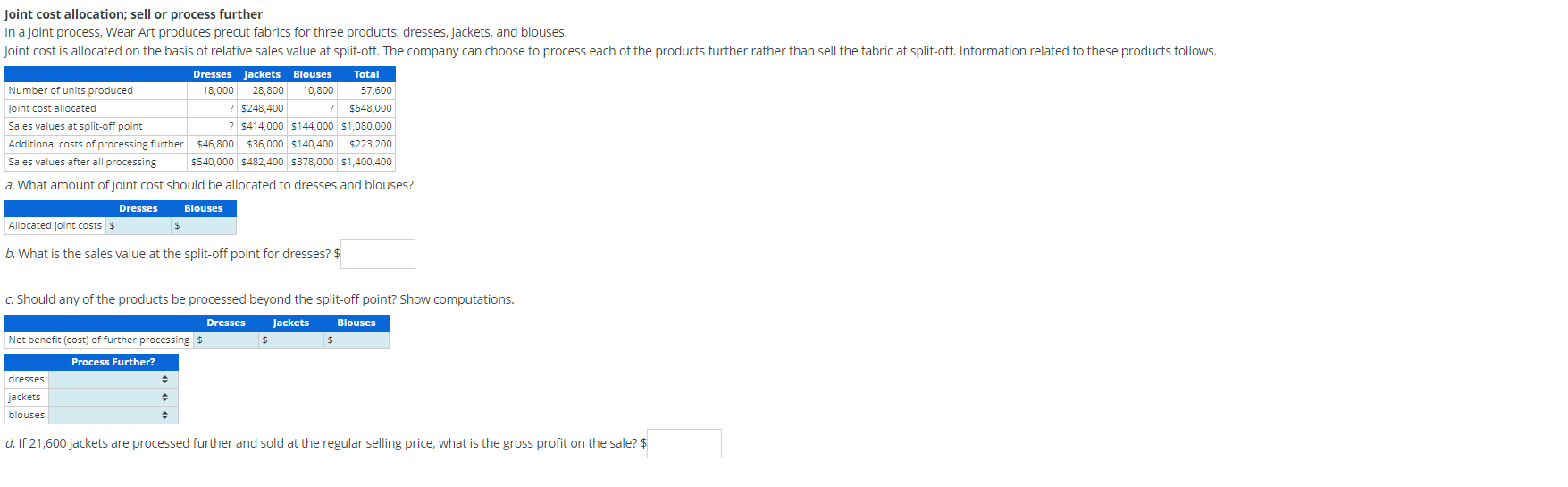

Joint cost allocation; sell or process further In a joint process, Wear Art produces precut fabrics for three products: dresses, jackets, and blouses. Joint cost is allocated on the basis of relative sales value at split-off. The company can choose to process each of the products further rather than sell the fabric at split-off. Information related to these products follows. Dresses Jackets Number of units produced Joint cost allocated Sales values at split-off point Additional costs of processing further Sales values after all processing Blouses Total 18,000 28,800 10,800 ? $248,400 57,600 ? $648,000 ? $414,000 $144,000 $1,080,000 $46,800 $36,000 $140,400 $223,200 $540,000 $482,400 $378,000 $1,400,400 a. What amount of joint cost should be allocated to dresses and blouses? Allocated joint costs $ Dresses Blouses $ b. What is the sales value at the split-off point for dresses? $ c. Should any of the products be processed beyond the split-off point? Show computations. Net benefit (cost) of further processing $ Dresses Jackets Blouses $ $ Process Further? dresses jackets blouses d. If 21,600 jackets are processed further and sold at the regular selling price, what is the gross profit on the sale? $

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts