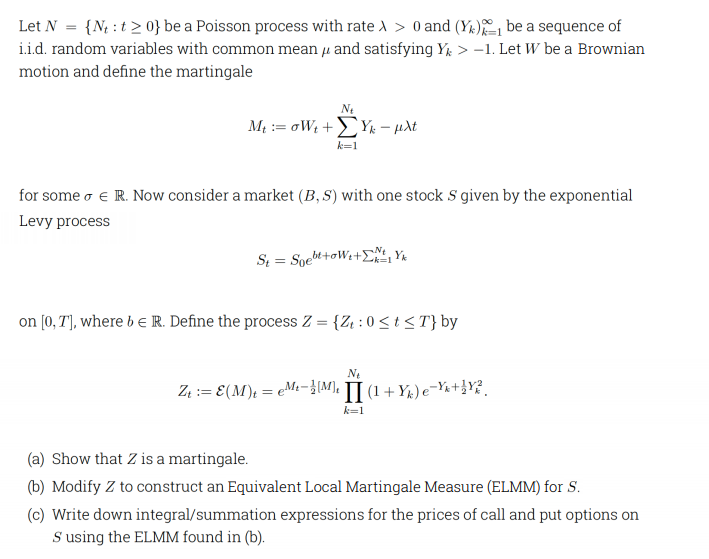

Question: Jump-Diffusion Models: Let N-{N, : t > 0} be a Poisson process with rate > 0 and (%)ei be a sequence of ii.d. random variables

Jump-Diffusion Models:

Let N-{N, : t > 0} be a Poisson process with rate > 0 and (%)ei be a sequence of ii.d. random variables with common mean u and satisfying Y1. Let W be a Brownian motion and define the martingale Nt ! for some e R. Now consider a market (B, S) with one stock S given by the exponential Levy process on [0, T], where b e R. Define the process Z = {4: 0 0} be a Poisson process with rate > 0 and (%)ei be a sequence of ii.d. random variables with common mean u and satisfying Y1. Let W be a Brownian motion and define the martingale Nt ! for some e R. Now consider a market (B, S) with one stock S given by the exponential Levy process on [0, T], where b e R. Define the process Z = {4: 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts