Question: just C please 2. (40 points) Assume that today is September 15. You work for a US importing firm that is scheduled to pay Australian

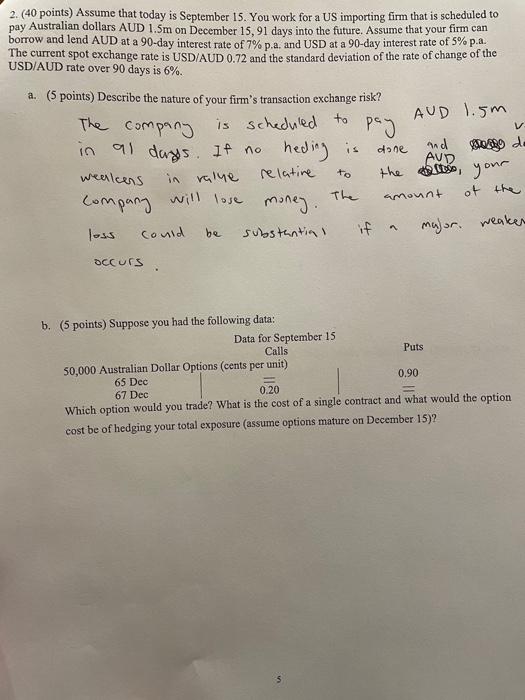

2. (40 points) Assume that today is September 15. You work for a US importing firm that is scheduled to pay Australian dollars AUD 1.5m on December 15, 91 days into the future. Assume that your firm can borrow and lend AUD at a 90-day interest rate of 7%p.a. and USD at a 90-day interest rate of 5% The current spot exchange rate is USD/AUD 0.72 and the standard deviation of the rate of change of the USD/AUD rate over 90 days is 6%. a. (5 points) Describe the nature of your firm's transaction exchange risk? AUD 1.5m The company is scheduled to pay in al days. If no neding is AVD wealers in ralne relative the to your The amount of the company will lose money . weaker loss could major. substantin I V and done solo de to be occurs b. (5 points) Suppose you had the following data: Data for September 15 Calls Puts 50,000 Australian Dollar Options (cents per unit) 65 Dec 0.90 67 Dec 0.20 Which option would you trade? What is the cost of a single contract and what would the option cost be of hedging your total exposure (assume options mature on December 15)? c. (5 points) What is the maximum US dollar cost you'll experience in December

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts