Question: Just need someone to help me with one question asap. It needs to be done in the same format i show you. The name begins

Just need someone to help me with one question asap. It needs to be done in the same format i show you. The name begins with S so use growth portfolio.

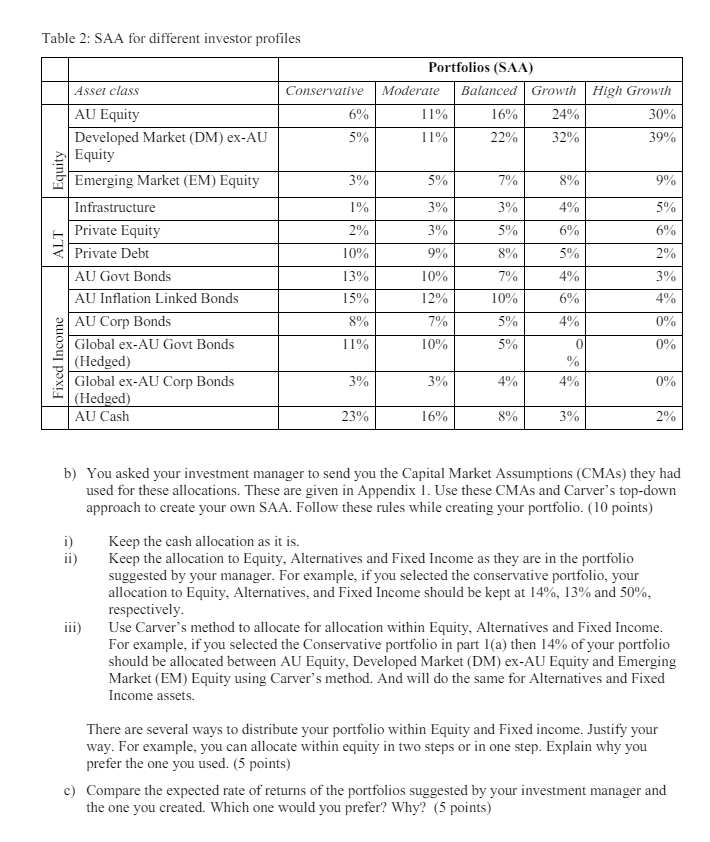

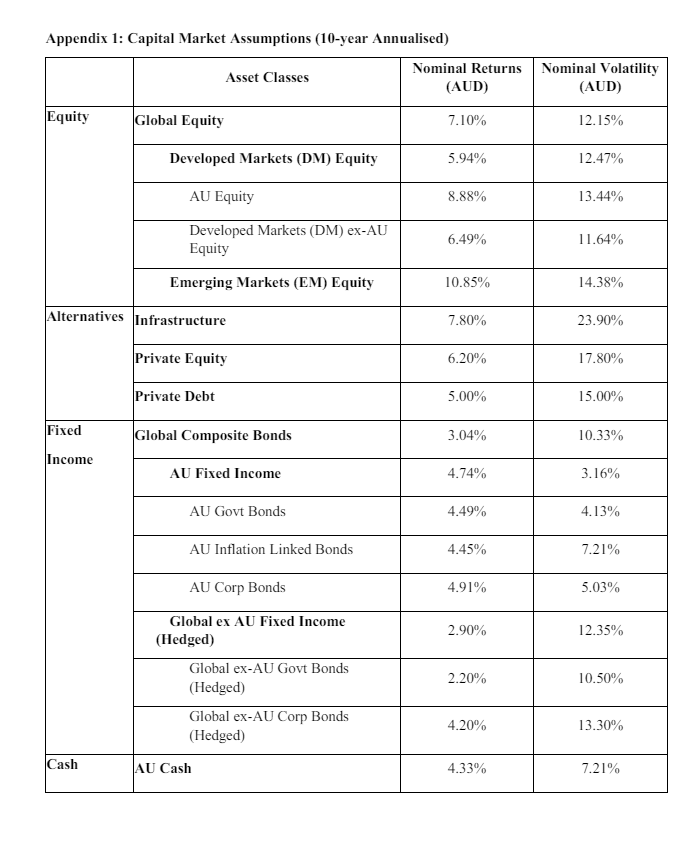

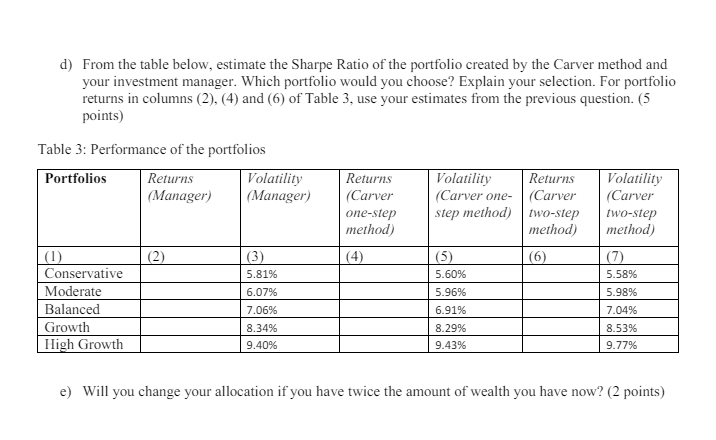

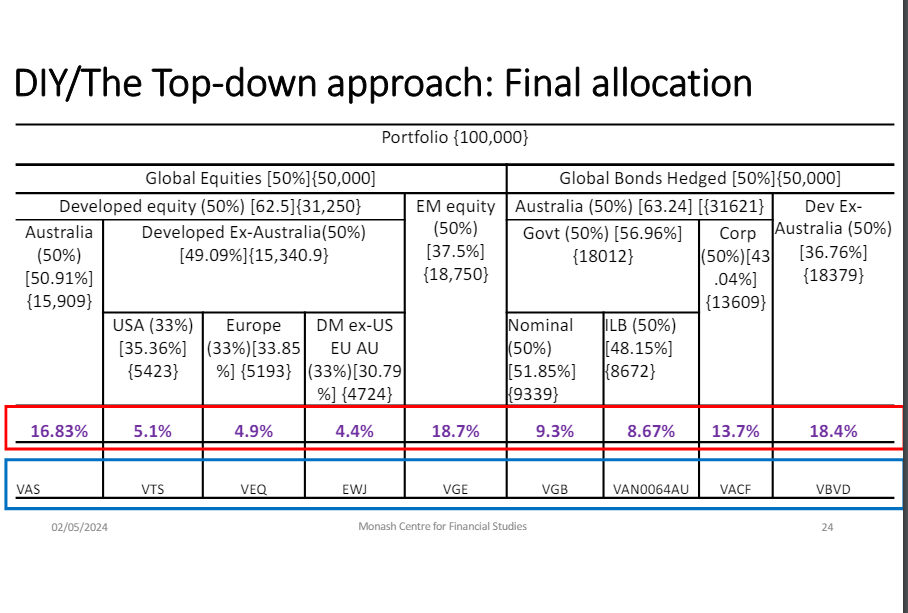

PART A (35 points) Question 1 (30 points) In Part A, students will build a strategic asset allocation consistent with their investor (risk) profile. Each student will be assigned an investor profile based on their age. Find your assigned age from the following table: Your age is assigned based on your first name. Table 1: Investor profile: Age Age in years The student whose first name begins with the following letters 80 A, B, C. D. E, F. G H, I, J, K 40 L, M, N, O, P. Q. R 30 S, T, U, V. W 20 X, Y, Z Students are required to create their strategic asset allocation using this investor profile and the capital market assumptions given in Appendix 1. 1. You have been assigned an investor profile based on your age. Based on this profile, you must answer the following questions (1(a) to 1(e)). To determine your investor profile, follow this rule: Your maximum allocation to Equity must not exceed (100 - your age) %. a) Suppose you have an asset manager who proposes the following Strategic Asset Allocation (SAA) for portfolios suitable for investors in different age groups. Which portfolio would you choose? Why? (3 points)Table 2: SAA for different investor profiles Developed Market (DM) ex-AU 5% Equity Emerging Market (EM) Equity 3 - C(ilobal ex-All Govt Bonds %4 10%a 5% 0% {Hedged) {Hedged) - Fixed Income b) You asked vour investment manager to send vou the Capital Market Assumptions (CMAs) they had used for these allocations. These are given in Appendix 1. Use these CMAs and Carver's top-down approach to create your own 5SAA. Follow these rules while creating your portfolio. (10 points) i) Keep the cash allocation as it 1s. i) Keep the allocation to Equity, Alternatives and Fixed Income as they are in the portfolio suggested by your manager. For example, if you selected the conservative portfolio, your allocation to Equity, Alternatives, and Fixed Income should be kept at 14%, 13% and 30%, respectivelv. i) Use Carver's method to allocate for allocation within Equity, Alternatives and Fixed Income. For example, it you selected the Conservative portfolio in part 1{a) then 14% of your portfolio should be allocated between AU Equity, Developed Market (DM} ex-AU Equity and Emerging Market (EM) Equity using Carver's method. And will do the same for Alternatives and Fixed [ncome assets. There are several ways to distribute your portfolio within Equity and Fixed income. Justify your way. For example, vou can allocate within equity in two steps or in one step. Explain why vou prefer the one you used. (3 points) ) Compare the expected rate of returns of the portfolios suggested by your investment manager and the one you created. Which one would you preter? Why? (5 points) Appendix 1: Capital Market Assumptions (10-year Annualised) Nominal Returns Nominal Volatility Asset Classes (AUD) (AUD) Equity Global Equity 7.10% 12.15% Developed Markets (DM) Equity 5.94% 12.47% AU Equity 8.88% 13.44% Developed Markets (DM) ex-AU 6.49% 11.64% Equity Emerging Markets (EM) Equity 10.85% 14.38% Alternatives Infrastructure 7.80% 23.90% Private Equity 6.20% 17.80% Private Debt 5.00% 15.00% Fixed Global Composite Bonds 3.04% 10.33% Income AU Fixed Income 4.74% 3.16% AU Govt Bonds 4.49% 4.13% AU Inflation Linked Bonds 4.45% 7.21% AU Corp Bonds 4.91% 5.03% Global ex AU Fixed Income 2.90% 12.35% (Hedged) Global ex-AU Govt Bonds 2.20% 10.50% (Hedged) Global ex-AU Corp Bonds 4.20% 13.30% (Hedged) Cash AU Cash 4.33% 7.21%d) From the table below, estimate the Sharpe Ratio of the portfolio created by the Carver method and your investment manager. Which portfolio would you choose? Explain your selection. For portfolio returns in columns (2). (4) and (6) of Table 3, use your estimates from the previous question. (5 points) Table 3: Performance of the portfolios Portfolios Returns Volatility Returns Volatility Returns Volatility (Manager) (Manager) (Carver (Carver one- (Carver (Carver one-step step method) two-step two-step method) method method (1) (2) (3) (4) (5) (6) (7) Conservative 5.81% 5.60% 5.58% Moderate 6.07% 5.96% 5.98% Balanced 7.06% 6.91% 7.04% Growth 8.34% 8.29% 8.53% High Growth 9.40% 9.43% 9.77% e) Will you change your allocation if you have twice the amount of wealth you have now? (2 points)DIY/The Top-down approach: Final allocation Portfolio {100,000} Global Equities [50%] {50,000] Global Bonds Hedged [50%] {50,000] Developed equity (50%) [62.5]{31,250} EM equity Australia (50%) [63.24] [{31621} Dev Ex- Australia Developed Ex-Australia(50%) (50%) Govt (50%) [56.96%] Corp Australia (50%) (50%) [49.09%]{15,340.9} [37.5%] {18012} (50%) [43 [36.76%] [50.91%] {18,750} .04%] {18379} {15,909} {13609} USA (33%) Europe DM ex-US Nominal LB (50%) [35.36%] (33%) [33.85 EU AU (50%) [48.15%] {5423} %] {5193} (33%) [30.79 [51.85%] (8672} %] {4724} (9339) 16.83% 5.1% 4.9% 4.4% 18.7% 9.3% 8.67% 13.7% 18.4% VAS VTS VEQ EWJ VGE VGB VAN0064AU VACF VBVD 02/05/2024 Monash Centre for Financial Studies 24

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!