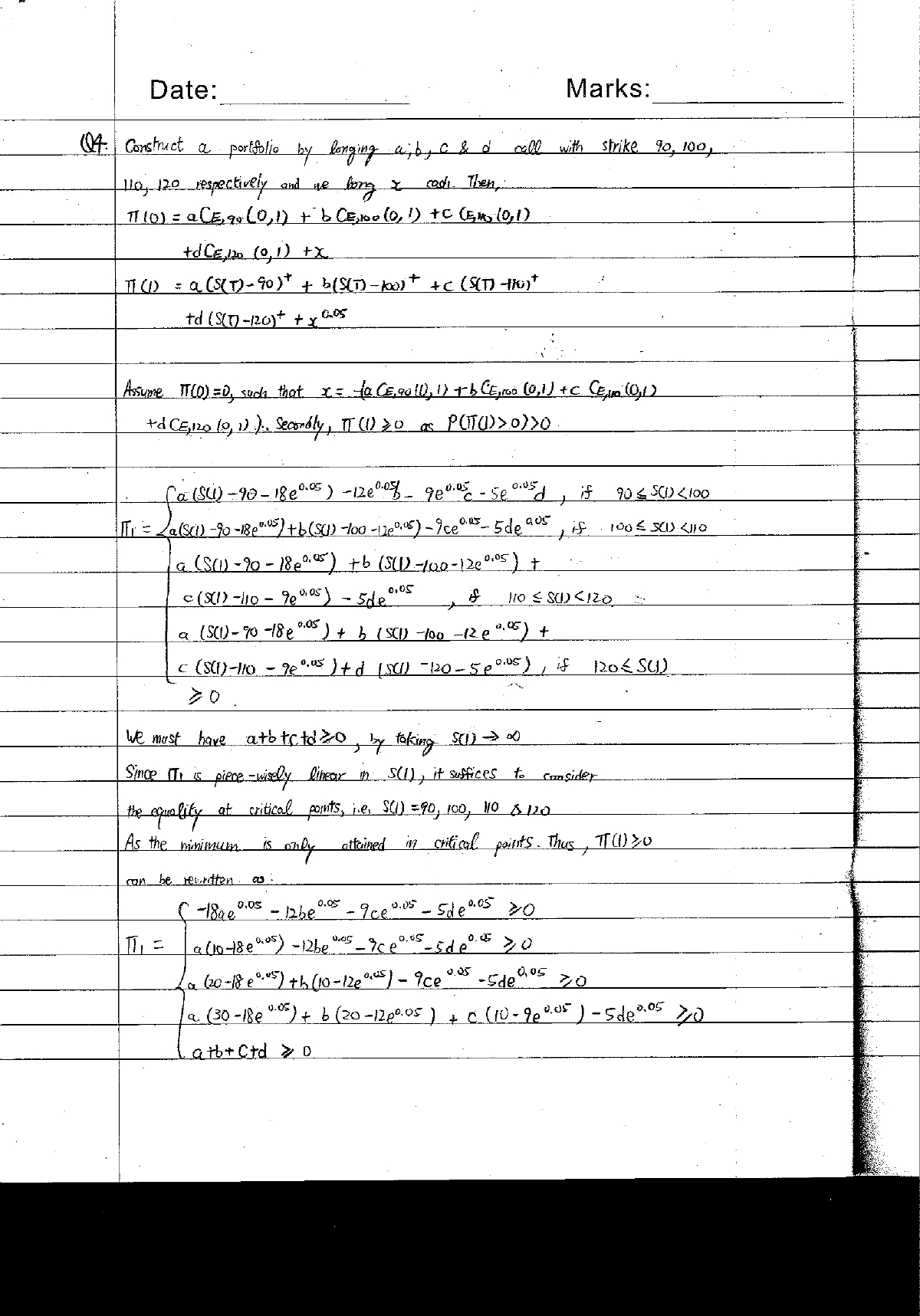

Question: Just Question 4 Only, Thank you! Date: Marks: A Construct a portfolio by longing a; by c & d wall with strike 90, 100, Ilo,

Just Question 4 Only, Thank you!

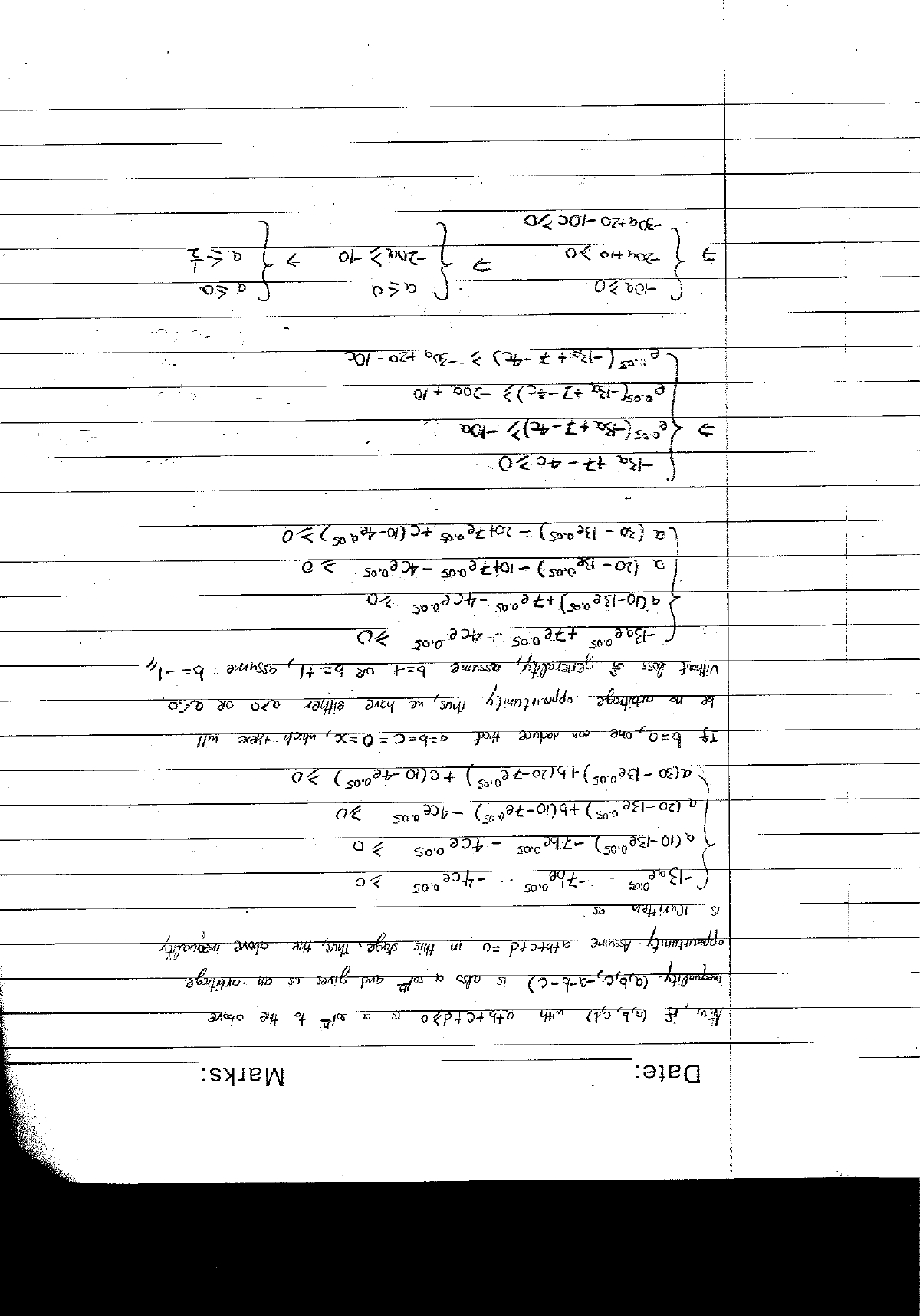

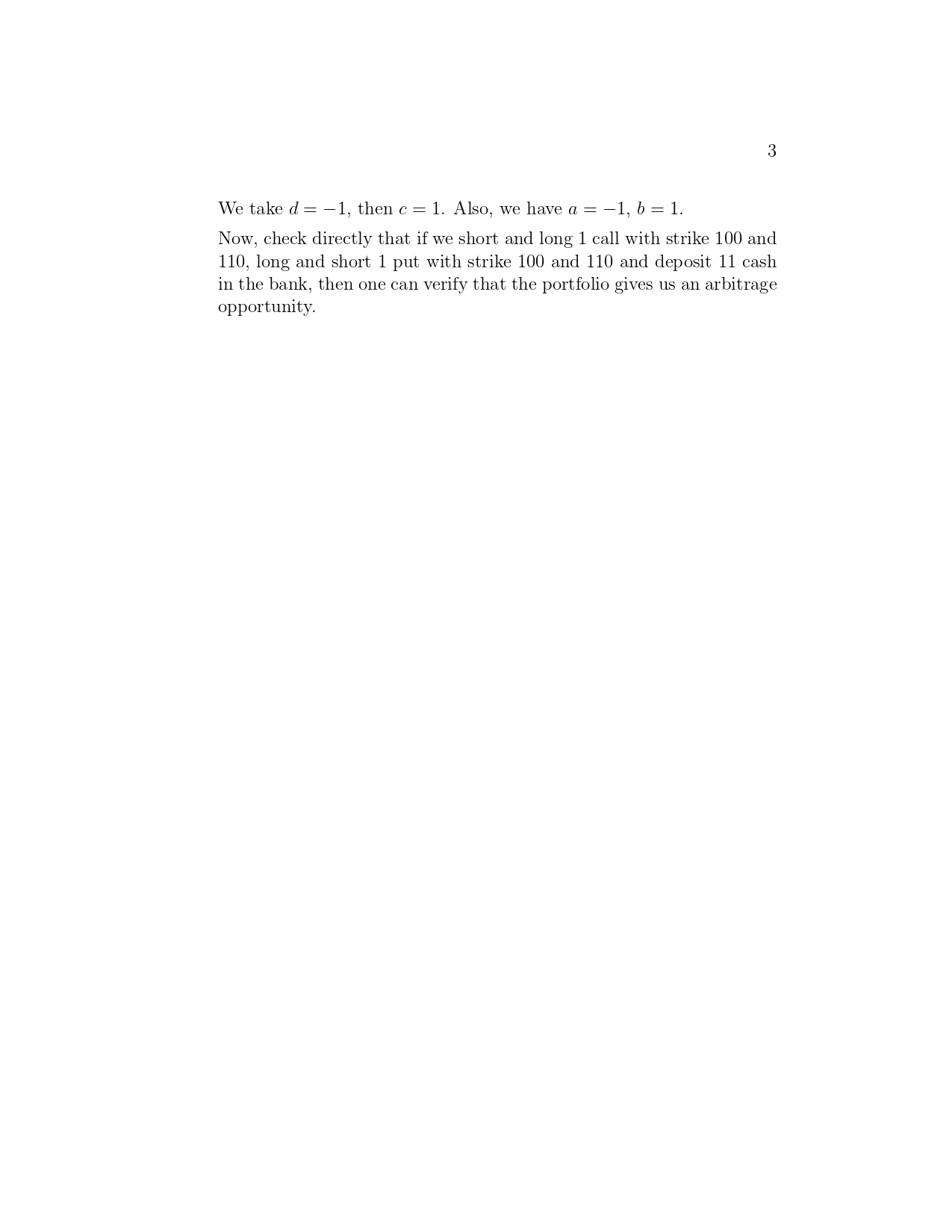

Date: Marks: A Construct a portfolio by longing a; by c & d wall with strike 90, 100, Ilo, 120 respectively and we long & codi. Then, TI (0) = a CE, 94 (0, 1) + 6 CE, 10. ( 0, 1) +C ( Ex, 10,1) todCE, Do (0, 1 ) + x I(1 = Q (S(T ) - 90 )+ + 6 (S(D) - post + c ( S(D) - the) + td (S (D - 120)+ + y 605 Assume IT(D) =0, such that X = (a (E,gold, 1) +- b CE, roo ( 0, 1) + C. CE,I (0, 1 ) +d CE,Izo (0, 1) ). Secondly, TT (1) 20 as P(IT()> > >0 Ca ( s() - 90 - 18 0 0:05 ) - 120 08 90"- - 5ed, if 90% S( 1) /0 aib+ Ctd > DDate: Marks: New if ( a ,b , cd ) with atbretdo is a soth to the above inequality . ( Q , b, c , - a -b - ( ) is also a soft and gives is an artitags opportunity Assume athreed =0 in this stage . This , the above inequality IS Huritter as - Bae oius . - the los .. -4ce 205 20 a (10-130":05)- 760205 - 4CQ 0.05 a (20 -130 05 ) +b(10-70 05) - 4ce205 20 a ( 30 - Be0.05 ) +h ( 20- 7 20 5 ) + 6( 10 -40 0. 05 ) 20 If b=0 , one con deduce that sEb=CE OsX , which there will be no arbitrage opportunity thus , we have either ano on ato Without loss of generally, assume but of beth , assume . be - 1 , +70 0.05 " 409 0.05 7 0) 9010-13e )+7205-4080 05 20 a (20- 13).05 ) - 10170 0 05 - 460 05 2 0 La (30 - 13 205 )- 20+ 705 + C(10-40 # 05 , 20 - Ba +7 - 4020'- Pass ( Ba + 7- 40)7 - Da ( 505 ( - 1a + 7-4() > -209 + 10 Les.5 ( -132:+ 7-4c) > -30g +20- 10c -109 20 Q So. 27 209 +0 20 -200 7 -10 -30a+20 -10c 20THE CHINESE UNIVERSITY OF HONG KONG Department of Mathematics MATH4210 Financial Mathematics 2021-2022 T1 Assignment 2 Due date: 17 October 2021 11:59 p.m. Please submit this assignment on blackboard. If you have any questions regarding this assignment, please email your TA Yang Fan fyang@math.cuhk.edu.hk). 1. (Put-Call Parity Relation with Dividend) Assume that the value of the dividend of the stock paid during [t, T] is a deterministic constant D at time to E (t, T]. Prove that CE(t, K) - PE(t, K) = S(t) - Ke-r(I-t) - De-r(to-t). 2. Suppose we have continuous compounding interest rate r in the market, for a stock paying proportional dividend (d x Sto ) at time to E (0, T) where de (0, 1), prove that the forward price is F(0, T) = a SoerT. 3. Two Vanilla put options have the same strike K, but different maturity dates 71 0) > 0. By consid ering II(1) 2 0, we have -45e0.05a - 40e0.05b + (100 - S(1) - 36e0.05)c + (110 - S(1) - 420.05)d if 0 co contradicts the third inequality. Since II(1) is piece-wisely linear in S(1), it suffices to consider the equality at critical points, i.e. S(1) = 0, 100 and 110, asthe minimum is only attained at the critical points. Thus, 11(1) 2 U can be rewritten as 74530115.; 7 4061055 + (100 7 3e'5)c + (110 7 42301130! 2 0 45e'5a 40611055 3660350 + (10 4260'05)d 2 O (10 7 4560'05)a 7 40.41053; 7 3650-"5c 7 425M5d _ a | b 2 0 Since if (a, b, c, d) with a + b > O is a solution to the above inequality, (:1, o,c,d) is also a solution and gives us an arbitrage opportunity. We may assume a + b = O at this stage. Thus, the above inequality is rewritten as 5e'05a + (100 7 36e'105)c + (110 7 42905\" > 0 7530-053 7 3680-050 + (10 7 425mm 2 0 (10 580'05) 3660'05c 42603515! > 0 If a : 0, one can deduce that c : d : b : :3 : U, which is not arbitrage opportunity. Thus, we either have a > O or a

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Mathematics Questions!