Question: just the yellow boxes PART 2 Cost Volume Relationships - Profit Planning 8 Big Al is about to begin work on the budget for 20x2

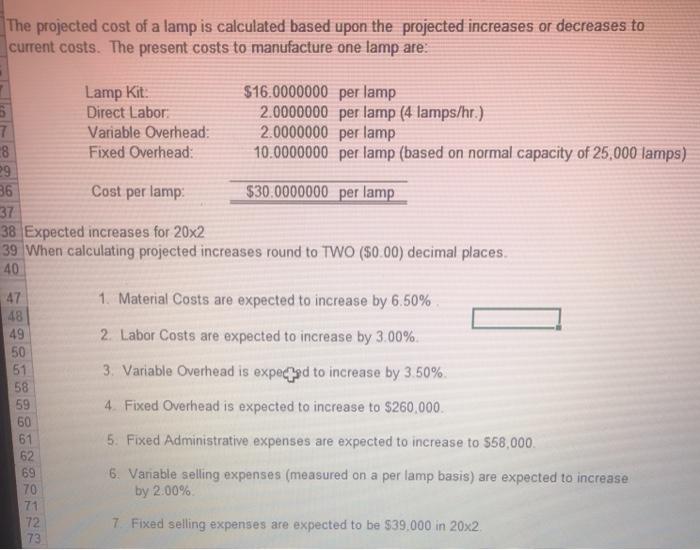

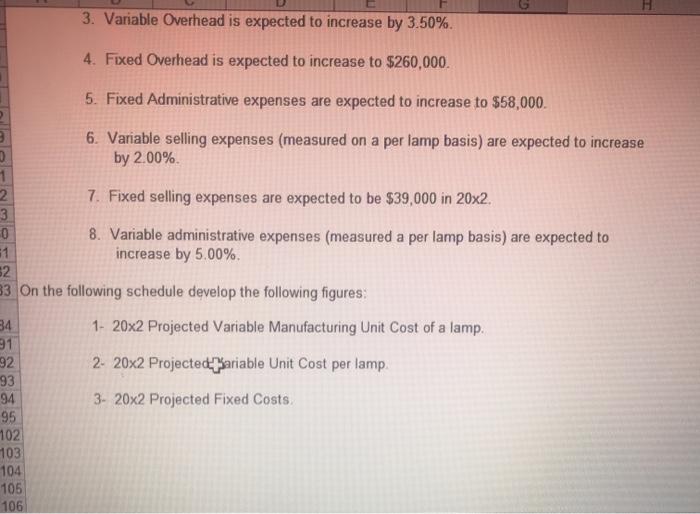

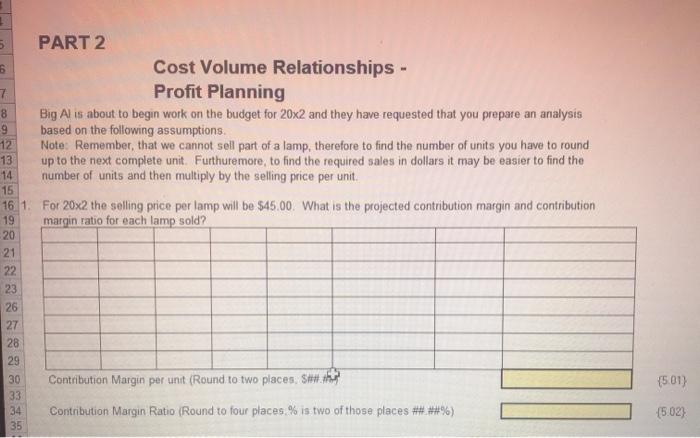

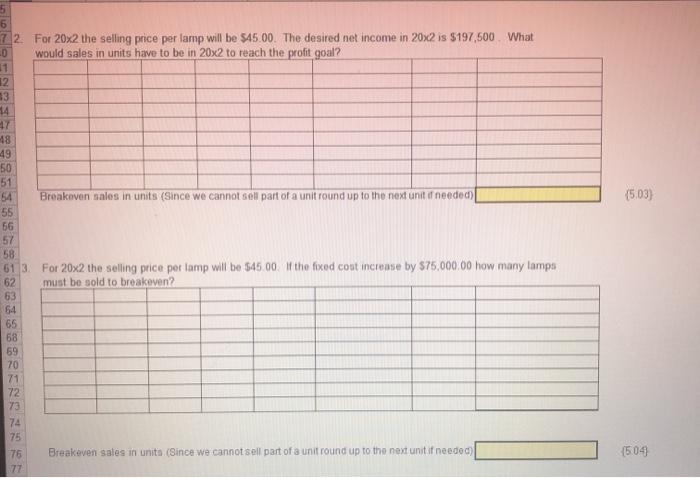

PART 2 Cost Volume Relationships - Profit Planning 8 Big Al is about to begin work on the budget for 20x2 and they have requested that you prepare an analysis 9 based on the following assumptions. 12 Note: Remember, that we cannot sell part of a lamp, therefore to find the number of units you have to round 13 up to the next complete unit. Furthuremore, to find the required sales in dollars it may be easier to find the 14 number of units and then multiply by the selling price per unit: 15 16 1 For 20x2 the selling price per lamp will be $45.00. What is the projected contribution margin and contribution 19 margin ratio for each lamp sold? 20 21 22 23 26 27 28 29 30 Contribution Margin per unit (Round to two places, S) 33 34 Contribution Margin Ratio (Round to four places, % is two of those places w%) 15.01) (502) (503) 377 2. For 20x2 the selling price per lamp will be $45.00. The desired net income in 20x2 is $197.500. What 10 would sales in units have to be in 20x2 to reach the profit goal? 31 42 43 4 47 48 49 50 51 54 Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit is needed) 55 56 57 58 613 For 20x2 the selling price per lamp will be $45.00. If the fixed cost increase by $75,000.00 how many lamps 62 must be sold to breakeven? 63 64 65 68 69 70 71 72 73 74 75 76 Breakoven sales in units (Since we cannot sell part of a unit round up to the next unit it needed) 77 I See The Light Projected Income Statement For the Period Ending December 31, 20x1 750,000.00 $ 375,000.00 Sales 25,000 lamps #****** Cost of Goods Sold Gross Profit Selling Expenses: Fixed Variable (Commission per unit) @ $3.00 75,000.00 $ 98,000.00 Administrative Expenses: Fixed Variable @ $2.00 50,000.00 92,000.00 Total Selling and Administrative Expenses. Net Profit 190,000.00 $ 185,000.00 I See The Light Projected Balance Sheet As of December 31, 20x1 $ 34,710.00 67,500.00 Current Assets Cash Accounts Receivable Inventory Raw Material Lamp Kits Work in Process Finished Goods Total Current Assets 8,000.00 500 @ $16.00 0 3000 @ $30.00 90,000.00 $ 200,210.00 Fixed Assets Equipment Accumulated Depreciation Total Fixed Assets Total Assets $ 20,000.00 6,800.00 13,200.00 $ 213.410.00 $ 54,000.00 $ 54,000.00 Current Liabilities Accounts Payable Total Liabilities Stockholder's Equity Common Stock Retained Earnings Total Stockholder's Equity Total Liabilities and Stockholder's Equity $ 12,000.00 147 410.00 159.410.00 $213.410.00 The projected cost of a lamp is calculated based upon the projected increases or decreases to current costs. The present costs to manufacture one lamp are: Lamp Kit $16.0000000 per lamp Direct Labor 2.0000000 per lamp (4 lamps/hr) 7 Variable Overhead 2.0000000 per lamp 8 Fixed Overhead 10.0000000 per lamp (based on normal capacity of 25,000 lamps) 29 36 Cost per lamp: $30.0000000 per lamp 37 38 Expected increases for 20x2 39 When calculating projected increases round to TWO ($0.00) decimal places 40 47 1. Material Costs are expected to increase by 6.50% 2. Labor Costs are expected to increase by 3.00% 3. Variable Overhead is expected to increase by 3.50% 4. Fixed Overhead is expected to increase to $260,000 48 49 50 51 58 59 60 61 62 69 70 71 72 73 5. Fixed Administrative expenses are expected to increase to $58,000. 6. Variable selling expenses (measured on a per lamp basis) are expected to increase by 2.00% 7. Fixed selling expenses are expected to be $39.000 in 20x2. 3. Variable Overhead is expected to increase by 3.50% 4. Fixed Overhead is expected to increase to $260,000. 5. Fixed Administrative expenses are expected to increase to $58,000 6. Variable selling expenses (measured on a per lamp basis) are expected to increase by 2.00% 1 2 7. Fixed selling expenses are expected to be $39,000 in 20x2. 3 0 8. Variable administrative expenses (measured a per lamp basis) are expected to 51 increase by 5.00% 52 33. On the following schedule develop the following figures: 34 1- 20x2 Projected Variable Manufacturing Unit Cost of a lamp. 31 92 2- 20x2 Projecte d'ariable Unit Cost per lamp 93 94 3. 20x2 Projected Fixed Costs 95 102 103 104 105 106 7 5 PART 2 6 Cost Volume Relationships - Profit Planning 8 Big Al is about to begin work on the budget for 20x2 and they have requested that you prepare an analysis 9 based on the following assumptions. 12 Note: Remember, that we cannot sell part of a lamp, therefore to find the number of units you have to round 13 up to the next complete unit. Furthuremore, to find the required sales in dollars it may be easier to find the 14 number of units and then multiply by the selling price per unit 15 16 1 For 20x2 the selling price per lamp will be $45.00. What is the projected contribution margin and contribution 19 margin ratio for each lamp sold? 20 21 22 23 26 27 28 29 30 Contribution Margin per unit (Round to two places. Stat. 33 Contribution Margin Ratio (Round to four places % is two of those places #*#*%) 35 (5.01) 34 (5.02) 6 72. For 20x2 the selling price per lamp will be 545.00. The desired net income in 20x2 is $197.500. What D would sales in units have to be in 20x2 to reach the profit goal? 11 12 33 14 Breakoven sales in units (Since we cannot sell part of a unit round up to the next unit of needed) (5.03) For 20x2 the selling price per lamp will be $45.00. If the fixed cost increase by $75,000.00 how many lamps must be sold to breakeven? 18 49 50 51 54 55 56 57 58 613 62 63 64 65 68 69 70 71 72 73 74 75 76 77 Breakeven sales in unita (Since we cannot sell part of a unit round up to the next unit if needed) 1504

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts