Question: KBA2 X study X G dec 2 - Cour: x G dec 2 x 2 FIN 5 Answ X G Answ x Teleg X

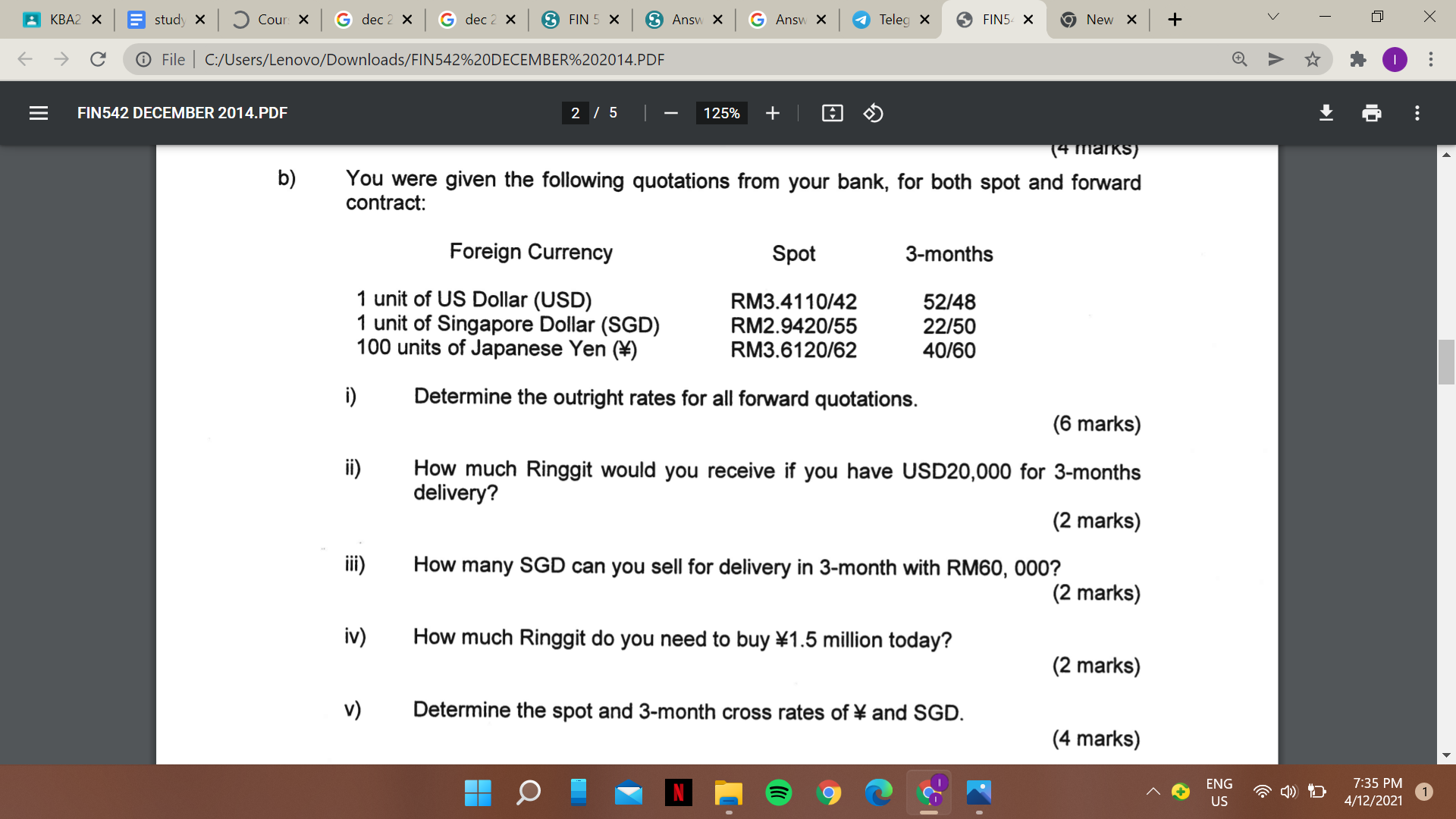

KBA2 X study X G dec 2 - Cour: x G dec 2 x 2 FIN 5 Answ X G Answ x Teleg X FIN5 X New X C File C:/Users/Lenovo/Downloads/FIN542%20DECEMBER%202014.PDF III FIN542 DECEMBER 2014.PDF b) 2 / 5 - 125% + (4 marks) You were given the following quotations from your bank, for both spot and forward contract: Foreign Currency Spot 3-months 1 unit of US Dollar (USD) RM3.4110/42 52/48 1 unit of Singapore Dollar (SGD) RM2.9420/55 22/50 100 units of Japanese Yen () RM3.6120/62 40/60 i) Determine the outright rates for all forward quotations. (6 marks) ii) How much Ringgit would you receive if you have USD20,000 for 3-months delivery? (2 marks) iii) How many SGD can you sell for delivery in 3-month with RM60, 000? (2 marks) iv) How much Ringgit do you need to buy 1.5 million today? (2 marks) v) Determine the spot and 3-month cross rates of \ and SGD. (4 marks) + ENG US 7:35 PM 4/12/2021 ...

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts