Question: Kindly assist Consider a standard multiple linear regression model with time series data: VI = bo + bixn + ... + box+ Uit. Assume that

Kindly assist

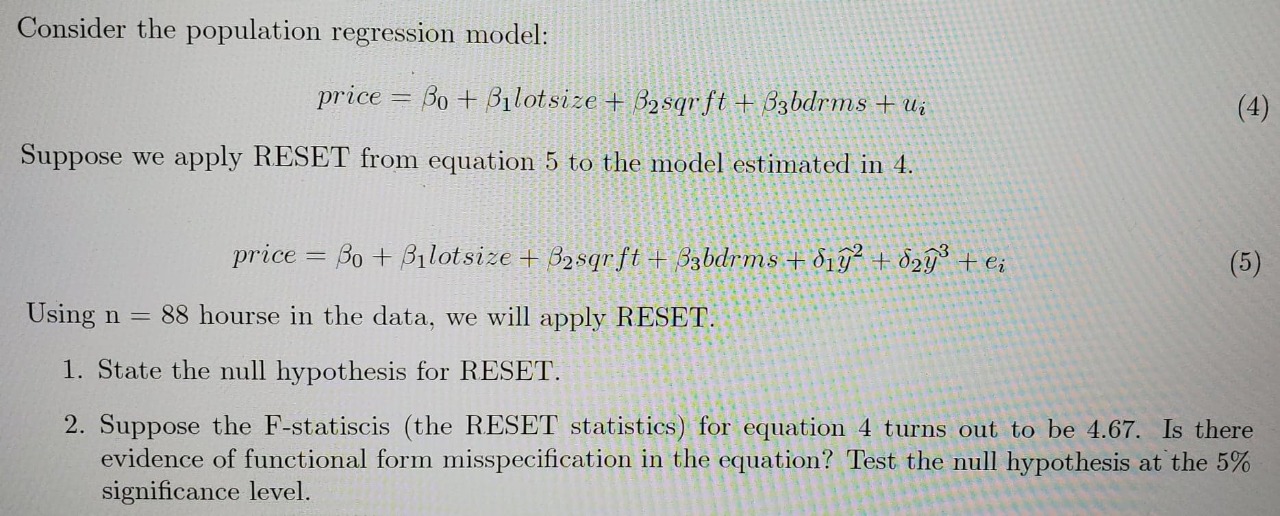

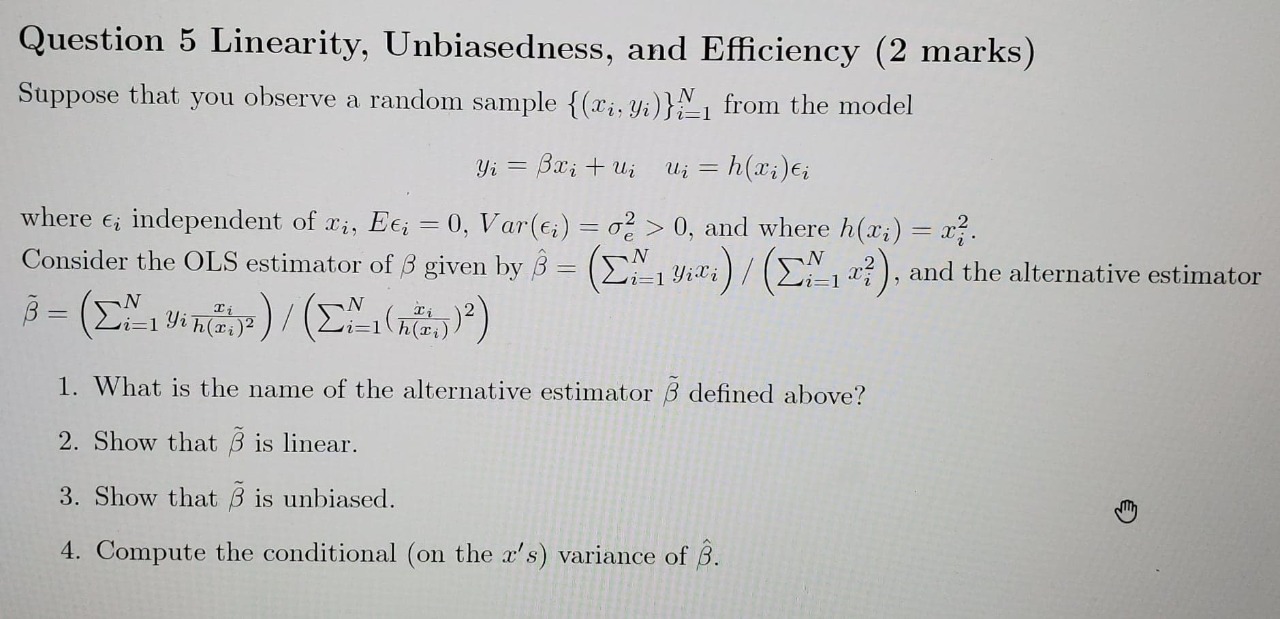

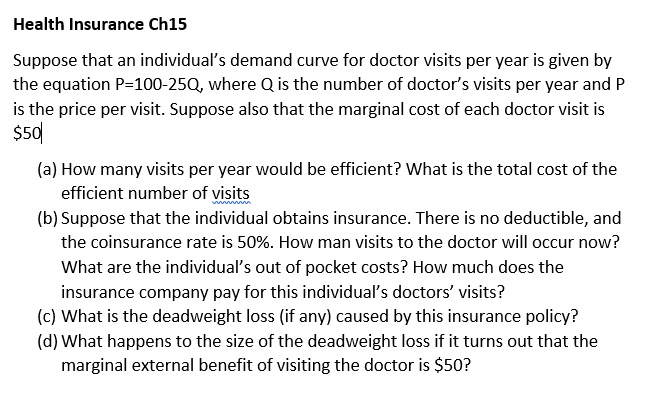

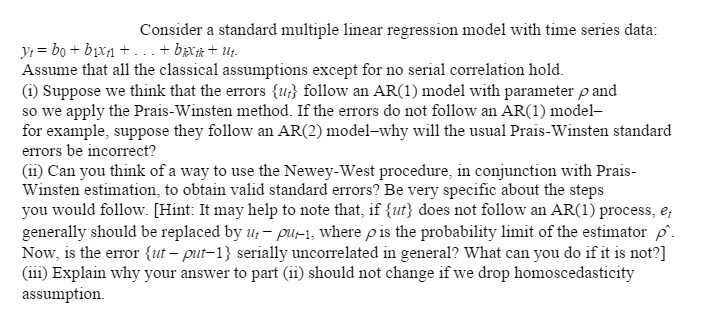

Consider a standard multiple linear regression model with time series data: VI = bo + bixn + ... + box+ Uit. Assume that all the classical assumptions except for no serial correlation hold. (i) Suppose we think that the errors {u} follow an AR(1) model with parameter p and so we apply the Prais-Winsten method. If the errors do not follow an AR(1) model- for example, suppose they follow an AR(2) model-why will the usual Prais-Winsten standard errors be incorrect? (ii) Can you think of a way to use the Newey-West procedure, in conjunction with Prais- Winsten estimation, to obtain valid standard errors? Be very specific about the steps you would follow. [Hint: It may help to note that, if {ut) does not follow an AR(1) process, et generally should be replaced by u - pur-1, where p is the probability limit of the estimator p. Now, is the error {ut - put-1} serially uncorrelated in general? What can you do if it is not?] (iii) Explain why your answer to part (ii) should not change if we drop homoscedasticity assumption.Consider the population regression model: price = Bo + Bilotsize + B2sqrft + 33bdrms + ui ( 4) Suppose we apply RESET from equation 5 to the model estimated in 4. price = Bo + Bilotsize + Basqraft + Babdrms + by- + day' tei (5) Using n = 88 hourse in the data, we will apply RESET. 1. State the null hypothesis for RESET. 2. Suppose the F-statiscis (the RESET statistics) for equation 4 turns out to be 4.67. Is there evidence of functional form misspecification in the equation? Test the null hypothesis at the 5% significance level.Question 5 Linearity, Unbiasedness, and Efficiency (2 marks) Suppose that you observe a random sample {(xi, yi)} from the model yi = Bxi tui ui = h(xi)ci where c independent of xi, Eci = 0, Var(ci) = 02 > 0, and where h(xi) = x?. Consider the OLS estimator of B given by B = (Cyixi) / (Ex? ), and the alternative estimator B = Zi= lyin(1 1 ) 2 )2 ) 1. What is the name of the alternative estimator 3 defined above? 2. Show that 3 is linear. 3. Show that S is unbiased. 4. Compute the conditional (on the x's) variance of B.Health Insurance Ch15 Suppose that an individual's demand curve for doctor visits per year is given by the equation P=100-250, where Q is the number of doctor's visits per year and P is the price per visit. Suppose also that the marginal cost of each doctor visit is $50 (a) How many visits per year would be efficient? What is the total cost of the efficient number of visits (b) Suppose that the individual obtains insurance. There is no deductible, and the coinsurance rate is 50%. How man visits to the doctor will occur now? What are the individual's out of pocket costs? How much does the insurance company pay for this individual's doctors' visits? (c) What is the deadweight loss (if any) caused by this insurance policy? (d) What happens to the size of the deadweight loss if it turns out that the marginal external benefit of visiting the doctor is $50

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts