Question: kindly do provide the working solution Austral-Asian Credit, a large financial service firm, has just reported the following year-end results: Selected Reported Year-End 2015 figures

kindly do provide the working solution

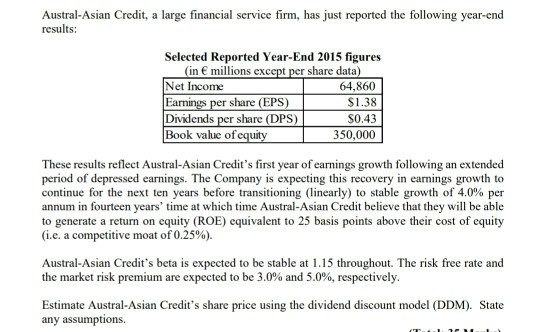

Austral-Asian Credit, a large financial service firm, has just reported the following year-end results: Selected Reported Year-End 2015 figures (in millions except per share data) Net Income 64,860 Earnings per share (EPS) $1.38 Dividends per share (DPS) S0.43 Book value of equity 350,000 These results reflect Austral-Asian Credit's first year of earnings growth following an extended period of depressed earnings. The Company is expecting this recovery in earnings growth to continue for the next ten years before transitioning (linearly) to stable growth of 4.0% per annum in fourteen years' time at which time Austral-Asian Credit believe that they will be able to generate a return on equity (ROE) equivalent to 25 basis points above their cost of equity (i.e. a competitive moat of 0.25%). Austral-Asian Credit's beta is expected to be stable at 1.15 throughout. The risk free rate and the market risk premium are expected to be 3.0% and 5.0%, respectively. Estimate Austral-Asian Credit's share price using the dividend discount model (DDM). State any assumptions

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts