Question: Kindly provide solutions for both part (a) and (b). Question 3 3. (a) Three models namely Mean Variance Optimization, Capital Asset Pricing Model and the

Kindly provide solutions for both part (a) and (b).

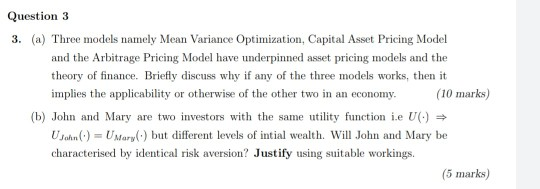

Question 3 3. (a) Three models namely Mean Variance Optimization, Capital Asset Pricing Model and the Arbitrage Pricing Model have underpinned asset pricing models and the theory of finance. Briefly discuss why if any of the three models works, then it implies the applicability or otherwise of the other two in an economy. (10 marks) (b) John and Mary are two investors with the same utility function i.e () UJohn() = Umary() but different levels of intial wealth. Will John and Mary be characterised by identical risk aversion? Justify using suitable workings. (5 marks) Question 3 3. (a) Three models namely Mean Variance Optimization, Capital Asset Pricing Model and the Arbitrage Pricing Model have underpinned asset pricing models and the theory of finance. Briefly discuss why if any of the three models works, then it implies the applicability or otherwise of the other two in an economy. (10 marks) (b) John and Mary are two investors with the same utility function i.e () UJohn() = Umary() but different levels of intial wealth. Will John and Mary be characterised by identical risk aversion? Justify using suitable workings

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts