Kish is an employee of Sin Ltd and his only source of income in 2019/20 is theremuneration

Question:

Kish is an employee of Sin Ltd and his only source of income in 2019/20 is theremuneration received from Sin Ltd. Kish pays 5% of his salary into thecompany pension scheme and Sin Ltd pays 2% contributions. Kish also paid £24,000 (net) into his personal pension scheme. The company accounts show the following remuneration paid to Kish:

| Bonus | |

£ | £ | |

30 June 2019 | 120,000 | 5,000 |

30 June 2020 | 128,000 | 8,000 |

The bonuses are paid on 1 January following Sin Ltd’s year end.

Calculate Kish’s total tax liability for the tax year 2019/20. Calculate the maximum personal pension contribution that Kish can make in the tax year 2020/21 assuming his salary remains the same.

You should assume the tax rates for 2019/20 continue to apply in the future.

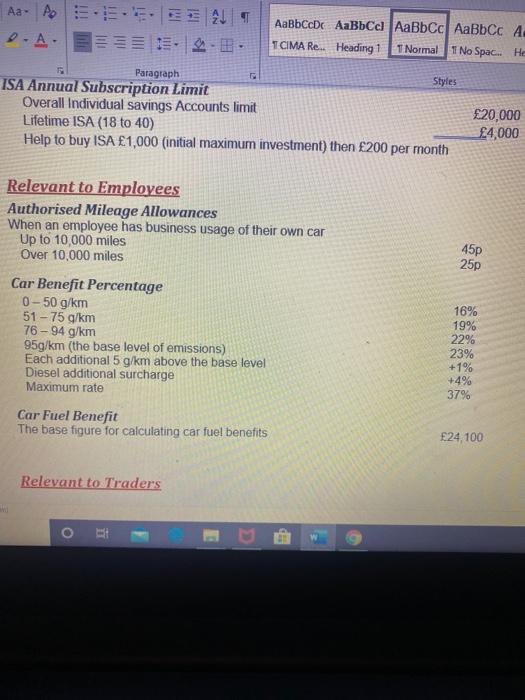

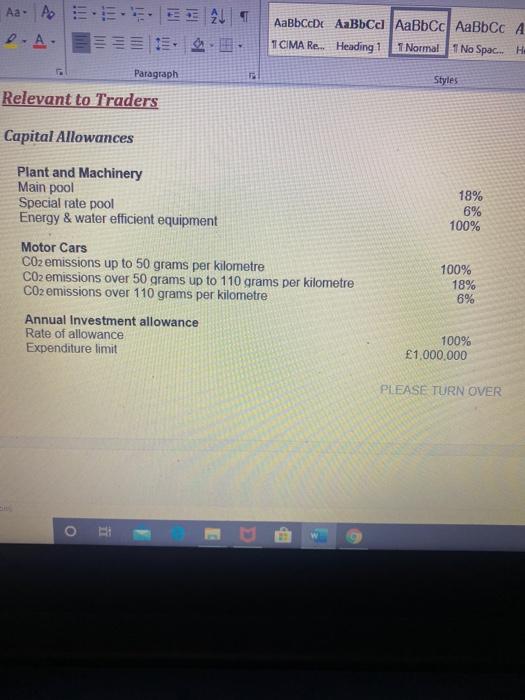

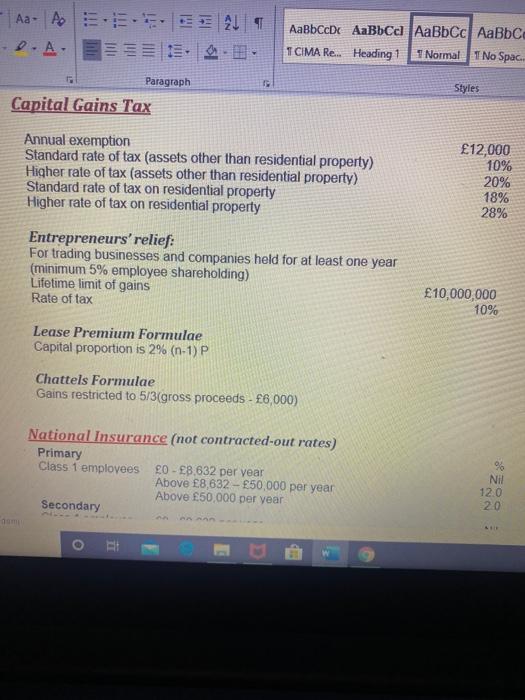

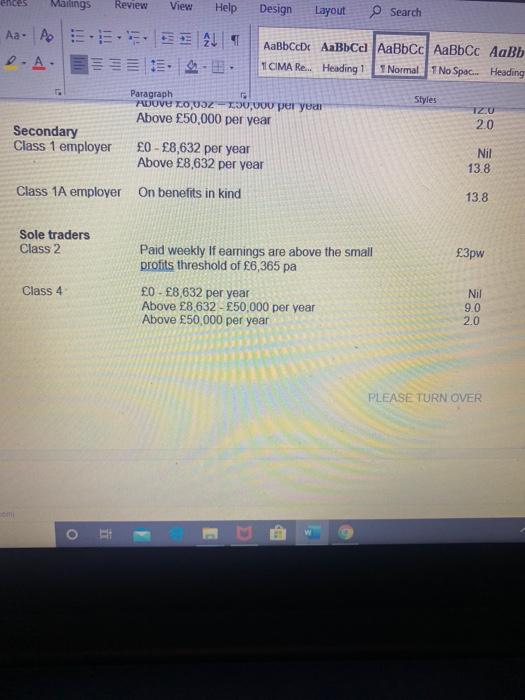

Tax Rates and Allowances 2019/20

Income Tax

Main Personal Allowances

Personal allowance | 12,500 |

Income limit for personal allowance (Note 1) Marriage allowance (Note 2) | 100,000 1,250 |

Note 1: When income exceeds the limit a clawback applies reducing the personal

allowance by £1 for every £2 above the limit.

Note 2: Spouses/civil partners are able to transfer £1,250 of their unused personal

allowance to their partner if both are basic rate taxpayers.

Tax Rates and Taxable Bands

Normal rate | Dividend rate | ||||

Basic rate | £0 - £37,500 | 20% | 7.5% | ||

Higher rate | £37,501 - £150,000 | 40% | 32.5% | ||

Additional rate | Over £150,000 | 45% | 38.1% | ||

Note 3: A personal savings allowance applies at a 0% tax rate, applied after the personal

allowance have been applied as follows:

£

Basic rate taxpayers 1,000

Higher rate taxpayers 500

Additional rate taxpayers Nil

Note 4: The first £2,000 of dividend income is taxed at 0% for all taxpayers.

Note 5: The first £7,500 of rental income from renting part of the taxpayer’s home is tax free if rent a room relief is claimed.

Pension Scheme Limits

Annual allowance | £40,000 |

Lifetime allowance | £1,055,000 |

Maximum contribution than can qualify for tax relief without earnings | £3,600 |

Expert Answer:

Accounting concepts and applications

ISBN: 978-0538745482

11th Edition

Authors: Albrecht Stice, Stice Swain