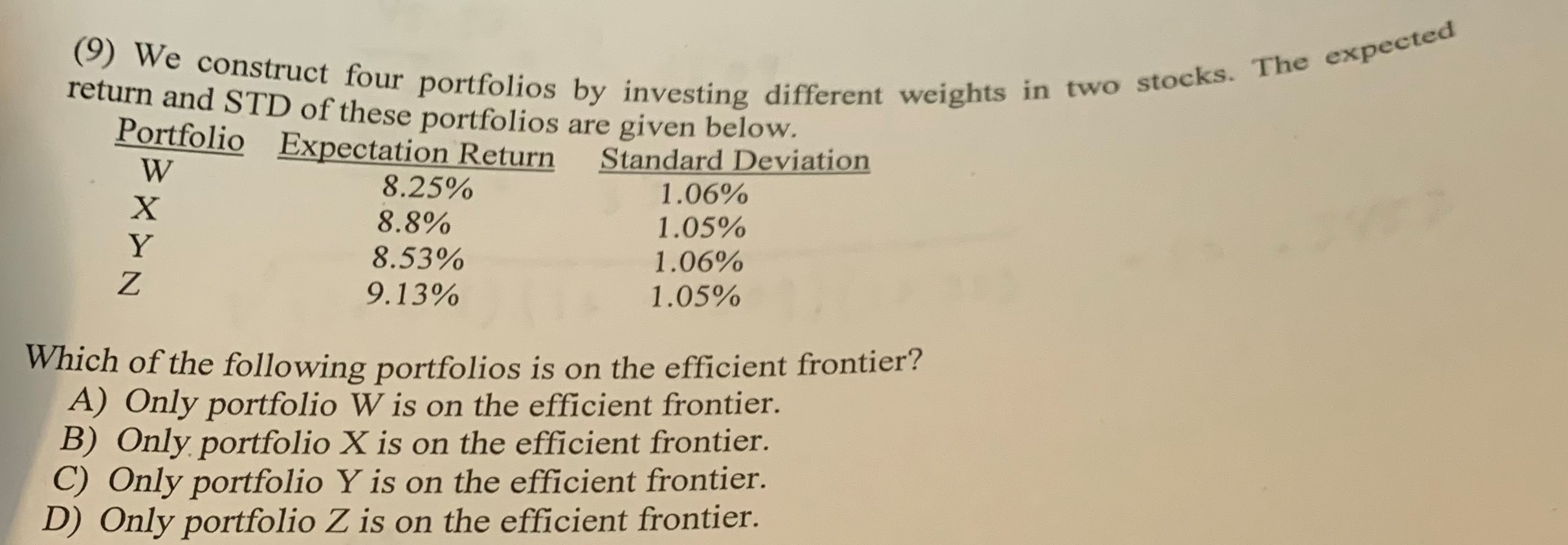

Question: Ks. The expected (9) We construct four portfolios by uct four portfolios by investing different weights in two s return and STD of these portfolios

Ks. The expected (9) We construct four portfolios by uct four portfolios by investing different weights in two s return and STD of these portfolios are given below. Portfolio Expectation Return Standard Deviation W 8.25% 1.06% 8.8% 1.05% Y 8.53% 1.06% 9.13% 1.05% Which of the following portfolios is on the efficient frontier? A) Only portfolio W is on the efficient frontier. B) Only portfolio X is on the efficient frontier. C) Only portfolio Y is on the efficient frontier. D) Only portfolio Z is on the efficient frontier

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock