Question: Last Lecture - In the last lecture, we covered selected materials on contract law in Chapter 13 (Practical Contracts] and Chapter 14 (Sales] We discussed

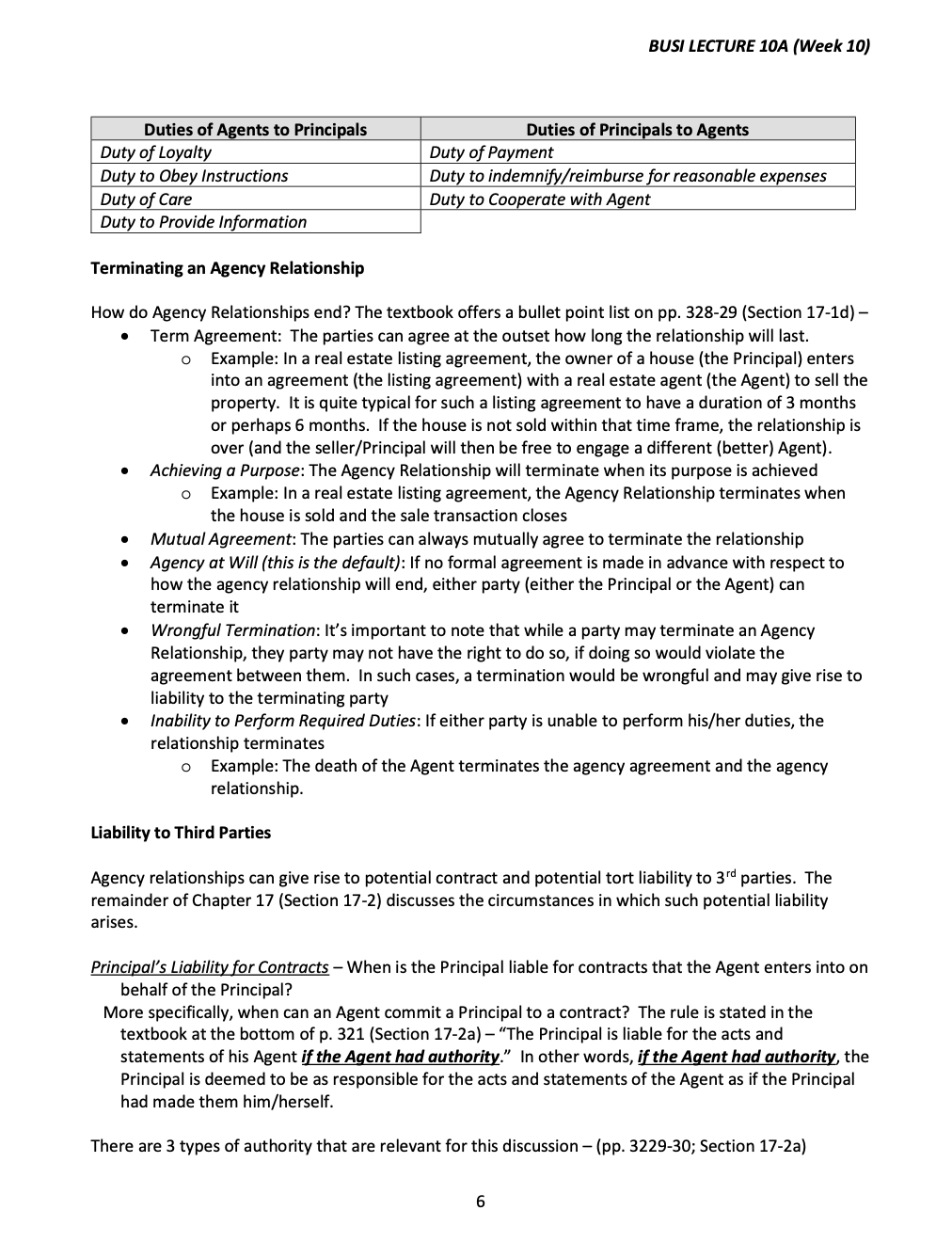

Last Lecture - In the last lecture, we covered selected materials on contract law in Chapter 13 (\"Practical Contracts\"] and Chapter 14 (\"Sales"] We discussed when parties should want their contracts to be in writing (rather than oral] We discussed how mistakes that occur in contract drafting are resolved vagueness, ambiguity and typos We discussed the organizational structure of a typical contract, and spent time defining and distinguishing the covenants that are in a contract (which are promises] from the representations & warranties (which are statements of fact about the present and past] We then moved on to the material in the textbook chapter on \"Sales\" and discussed express and implied warranties, the definition of \"merchant\" and of \"merchantability\An Agent is required (again, defined as "the person who is acting on behalf of a Principal") The Principal and Agent must mutually consent that the Agent will act on behalf of the Principal . The Principal and Agent must mutually consent that the Agent will be subject to the Principal's control When both the Principal and the Agent mutually consent, a fiduciary relationship is thereby created What then is a "fiduciary relationship"? The definition is set forth on pp. 325-26 Section 17-la as "one of trust in which a trustee acts for the benefit of the beneficiary, always putting the interests of the beneficiary before his own." The last part of this definition -- always putting the interests of the beneficiary before his own - is crucial. o It's important to understand what a fiduciary relationship is. If the definition is still unclear, re-read the bullet points above, and re-read the textbook discussion as well. What are some examples of Agency Relationships? Engaging a financial advisor to manage your investment assets - The nature of this agency relationship is typically detailed in a formal agreement between you and the financial advisor - It should be noted here that not all financial advisors are held to fiduciary standard of care under the law. What does this mean? If the financial advisor is a fiduciary, it means that the financial advisor must put the client's interests ahead of the advisor's interests. o However, some financial advisors are not fiduciaries, and are held to a more limited "suitability" standard, meaning that they are required only to provide "suitable" financial advice to the client (and not necessarily the best advice for the client). Whether financial advisors should be held to the higher standard by financial market regulators has been a topic of a great deal of debate in the past several years. I've included a short article by Becca Stanek, entitled "What is a Fiduciary" (SmartAsset, June 11, 2020) that summarizes some of the issues and the current state of the law (as of June 2020). A link to the article is below, and a pdf copy of the article is posted in the Canvas Module for Lecture 10A. There will be a question about the material in the article in the Worksheet; you should read the linked article (it's short) prior to completing the Worksheet. https://smartasset.com/financial-advisor/what-is-fiduciary-financial-advisor Engaging a lawyer to represent you on a legal matter o The fiduciary relationship here is typically detailed in a formal engagement letter and regulated by law and by attorney state bar rules The lawyer is always a fiduciary, and is obligated to put the client's interests (the Principal) ahead of the lawyer's interests (the Agent) Engaging a real estate agent to represent you on a real estate purchase/sale transaction o The fiduciary relationship here is typically detailed in a listing agreement and regulated by law and by national realtor association rules. 2Again, the real estate agent is always a fiduciary, and is obligated to put the client's interests (the Principal] ahead of the real estate agent's interests (the Agent]. In each of the above examples, you are the Principal, and the other party is the Agent in the relationship. With the exception of certain financial advisors, the Agent is a fiduciary and must always put your interests above and before hisfher own. Again, this is the essence of a fiduciary relationship. Duties that Agents owe to Principals in an Agency Relationship What specific duties do Agents owe to Principals (pp. 326+; Section 17-1b]? There are several 0 Agents owe Principals a Duty of Lgalg. o What does this Duty of Loyalty entail? There is a list in the textbook on p. 326+ (Section 17-1b] that provides details as to what the Duty of Loyalty includes Outside benefits An Agent may not receive outside profits arising from the relationship without the Principal's knowledge and approval Example: investment management. You have engaged me to be the manager of your financial assets, and to make investment decisions on your behalf. I am the Agent, you are the Principal, and you pay me a fee for performing this service for you. If I decide to invest your assets into a mutual fund, and the mutual fund pays investment managers a \"commission\" of 5% of the amount that the investment manager puts into the fund (in other words, I direct $100,000 of your funds to be invested into the mutual fund, the mutual fund manager will pay me a 5% \"commission\" or $5,000], can I receive and keep the 5% commission? 0 No I cannot receive and keep the $5,000, unless you are aware of the commission and you have approved it. Confidential information Agents can neither disclose, nor use for their own benefit, any confidential information they acquire during the agency relationship Example: One ofthe worksheet questions includes a hypothetical involvingjust this issue arising from a real estate transaction Competition with Principal Agents are not allowed to compete with the Principal in any matter within the scope of the agency business Example: real estate transaction: You want to purchase a reasonably priced house in the South Bay, and you have hired me to help you find a reasonably priced house for you to purchase. I research the local housing market, and discover a wonderful house that is perfect for you it's priced below the market, and is in a good school district. In fact, this house is such a great deal that I decide that I will purchase the house myself. Can I do this? 0 No I cannot. I cannot \"compete\" with you in the scope of the agency business (which in this example is buying a house]. Conflict of interest between Two Principals An Agent may not act for two Principals whose interests conflict, unless othenvise agreed. 3 Example: Actor/Director representation [this example is straight from the textbook on p. 32?; Section 17-1b] Travis represents both fim director Steven Spielberg and film actress Jennifer Lawrence. Spielberg is casting the title role in a movie he is directing, and Lawrence very much wants that role. Can Travis represent them both? 0 Travis cannot represent both clients when they are negotiating with each other unless both of them agree to it. Secretly Dealing with the Principal If a Principal hires an Agent to arrange a transaction, the Agent may not become a party to the transaction withoutthe Principal's permission Example: Script-Writer/Director [this example is also straight from the textbook on p. 327; Section 17-1b) Film director Stephen Spielberg has hired Trang to read incoming new scripts for him. Unbeknownst to Spielberg, Trang has written her own script as well. Can she try to sell it to him without telling him that she is the author? 0 No, she cannot. She must disclose to him that she is the author. He may then buy it or not buy it, but she cannot transact with him secretly without adequate disclosure. Appropriate Behavio An Agent may not engage in inappropriate behavior that reflects badly upon the Principal Example: Agent disporoges Principoi I am your attorney representing you in a contract dispute that is being litigated in court. The judge overseeing the trial asks me why you signed a contract that contains the contract provision that is in dispute, and I respond to the judge \"Because my client is a complete idiot more stupid than any other client I have ever represented.\" Have I done something wrong here? 0 Yes, absolutely. In representing you, I cannot simultaneously disparage you and/or act inappropriately while working for you in ways that reflect badly upon you. Other Agent duties (p. 327+; Section 17-1b) -) There are other Agent duties as well beyond the Duty of Loyalty. These include o Duty to Obey Instructions An Agent must obey the Principal's instructions [unless the instructions are illegal or unethical) Example: Attorneys and pleo offers dents You are my attorney in a criminal law matter, and | tell you that I am innocent of the crime charged, and that I do not want to accept any plea offer of any kind. Must you follow my instructions? Yes. You cannot negotiate or accept a plea offer on my behalf if I have instructed you not to do so. 0 Duty of Care An Agent has a duty of reasonable care and to act with reasonable care Example: Attorneys and Lego! Competence/Experience Prior to teaching at Foothill, I worked for 10+ years as a business attorney, advising company clients on a range of corporate law matters and business contracts. You have recently been arrested on a criminal violation and are facing felony charges. lam the only attorney you know, and you ask me to represent you. I have no experience handling criminal law matters, and have never set foot inside a criminal courtroom. Should I agree to represent you on a criminal law matter? I definitely should not do so, as I have no competence or experience in criminal law matters (A BUSI 18 student once asked me to represent him on a criminal law matter a few years ago involving charges of vandalism; I declined to do so because I was and am not sufficiently skilled and experienced to provide the kind of legal representation on a criminal matter that the student needed). o Duty to Provide Information - An Agent has a duty to provide the Principal with all information in her/his possession that the Principal might want to know. Example: An Agent cannot keep information secret from the Principal, and some of the hypotheticals above reflect this point (for example, Duty of Loyalty - Outside Benefits; Duty of Loyalty - Secretly Dealing with the Principal). Obviously, there is a great deal of potential conflict in an Agency Relationship, and in fact, such conflicts are fairly common. (Most attorney malpractice claims and attorney disbarment actions arise out of the failure of the Agent/Attorney to adhere to his/her duties that are owed by the Agent/Attorney to his/her Principal.) When an Agent breaches his/her duty to a Principal, there are 3 remedies that the Principal may seek against the Agent (p. 328; Section 17-1b) . Damages - the Principal can recover from the Agent any damages the breach has caused . Profits - if the Agent has breached the duty of loyalty, s/he must turn over to the Principal any profits earned as a result of the wrong-doing. Rescission - if the Agent has violated her/his duty of loyalty, the Principal may rescind the transaction Duties that Principals owe Agents in an Agency Relationship All of the discussion thus far has focused on the duties owed by Agents to Principals. Do Principals owe any duties to Agents? Yes, Principals do owe duties to Agents in an Agency relationship, but these are much more straightforward (p. 328; Section 17-1c). The Principal's duties to Agents include - . Duty of Payment: The Principal must pay the Agent as required by the agreement between them Example: Accounts/Attorneys - Clients/Principals must pay to their Agent Accountants or Attorneys the amounts agreed to in the initial engagement agreement between them. Duty of Indemnification/Reimbursement: The Principal must agree to indemnify/reimburse the Agent for reasonable expenses incurred in the Agency Relationship Example: Court Costs/Fees - A client who hires an attorney to pursue a legal claim must compensate and reimburse the attorney for all reasonable expenses arising from the representation - court costs, filing fees, investigator expenses, etc. Duty of Cooperation: The Principal must cooperate with the Agent in performing the Agency tasks. o Example: Legal Representation. When a client hires an attorney to represent him/her, the client has a duty to cooperate with the attorney in the representation. The textbook has a nice table at the bottom of p. 328 (Section 17-1c) summarizing the principal duties of Agents to Principals and Principals to Agents. I have reproduced this summary table here - 5BUSl LECTURE 10A {Week 10) Duties of Agents to Principals Duties of Principals to Agents Duty of Loyalty Duty of Payment Duty to Obey instructions Duty to indemnify/reimburse for reasonable expenses Duty of Core Duty to Cooperate with Agent Duty to Provide information Terminating an Agency Relationship How do Agency Relationships end? The textbook offers a bullet point list on pp. 328-29 (Section 17-1d] 0 Term Agreement: The parties can agree at the outset how long the relationship will last. 0 Example: In a real estate listing agreement, the owner of a house (the Principal] enters into an agreement (the listing agreement] with a real estate agent (the Agent] to sell the property. It is quite typical for such a listing agreement to have a duration of 3 months or perhaps 6 months. If the house is not sold within that time frame, the relationship is over (and the sellerlPrincipal will then be free to engage a different (better) Agent]. 0 Achieving a Purpose: The Agency Relationship will terminate when its purpose is achieved 0 Example: In a real estate listing agreement, the Agency Relationship terminates when the house is sold and the sale transaction closes o MutualAgreement: The parties can always mutually agree to terminate the relationship 0 Agency at Wiii {this is the default): If no formal agreement is made in advance with respect to how the agency relationship will end, either party (either the Principal or the Agent] can terminate it o Wrongfui Termination: It's important to note that while a party may terminate an Agency Relationship, they party may not have the right to do so, if doing so would violate the agreement between them. In such cases, a termination would be wrongful and may give rise to liability to the terminating party 0 inability to Perform Required Duties: If either party is unable to perform his/her duties, the relationship terminates 0 Example: The death of the Agent terminates the agency agreement and the agency relationship. Liability to Third Parties Agency relationships can give rise to potential contract and potential tort liability to 3rd parties. The remainder of Chapter 1? (Section 17-2] discusses the circumstances in which such potential liability arises. Princigoi's Liability for Contracts When is the Principal liable for contracts that the Agent enters into on behalf of the Principal? More specifically, when can an Agent commit a Principal to a contract? The rule is stated in the textbook at the bottom of p. 321 (Section 17-2a] "The Principal is liable for the acts and statements of his Agent it the Agent had an thorijy.\" In other words, if the Agent had authorijy, the Principal is deemed to be as responsible for the acts and statements of the Agent as if the Principal had made them him/herself. There are 3 types of authority that are relevant for this discussion (pp. 3229-30; Section 17-2a] BUS! LECTURE 10A {Week 10) [1] Express Authority; [2] Implied Authority; and [3] Apparent Authority Express Authority - 0 Definition: \"Either by words or conduct, the Principal grants an Agent permission to act\" (p. 329; Section 17-2a) 0 Express Authority is the most straightforward kind of authority an Agent can have, in which the Principal instructs the Agent to do something. 0 Exompie: The Principal expressly authorizes an action [sell an investment, or enter into a contract), and the Agent does the action. The Agent has express authority to act. Im plied Authority- 0 Definition: \"The Agent has authority to perform acts that are reasonably necessary to accomplish an authorized transaction, even if the Principal does not specify them\" [p. 330; Section 17-2a) o The rule for Implied Authority is that \"Unless otherwise agreed, the authority to conduct a transaction includes authority to perform acts that are reasonably necessary to accomplish it\" (p. 330; Section 17-2a] The Principal does not have to micromanage the Agent. The law assumes that the Agent has the authority to do anything that is reasonably necessary to accomplish the task. 0 Exompie [from the textbook): A Principal engages an Agent to auction the contents of a house. The Agent then hires an auctioneer, advertises the auction, rents a tent, etc. These actions are appropriate because there is implied authority to undertake them. Apparent Authority- 0 Definition: \"A Principal does something to make an innocent third party believe that an Agent is acting with the Principal's authority, even though the Agent is not authorized." (p. 330; Section 17-2a} o Apparent Authority is the most interesting of the three kinds of authority, and the rule here is that "A Principal can be liable for the acts of an Agent who is not, in fact, acting with authority if the Principoi's conduct causes a third party to reasonably believe that the Agent is authorized\" (p. 330; Section 17-2a]. Because the Principal has done something to make the 3'd party beiieve the Agent is authorized, the Principal becomes liable to the 3'd party as if the Agent did have the authority. 0 Exompie [from the textbook): Fraudster stockbrokers are selling fraudulent stock out of their offices at a legitimate [non-fraudsterl brokerage house, using firm e-mail and making presentations to investors in company offices and conference rooms. Although the fraudsters did not have express authority or implied authority from their employers to sell fraudulent stock, it appeared to a 3'd party that they did, and for that reason, the brokerage house [the Principal] is going to be liable for the fraud as well on an apparent authority theory the fraudsters appeared to a 3rd party to have the authority to be selling fraudulent stock. Agent's Liobiiity for Contracts When does the Agent have liability on a contract that the Agent enters into with a 3''1 party on behalfof a Principal? It's a little complicated, and the rules are set forth on pp. 330+, Section 17-2b. BUS! LECTURE 10A {Week 10} Fully Disclosed Principal - An Agent is not liable for any contracts with 3'd parties that the makes on behalf of a fully disclosed Principal. o What does \"fully disclosed Principal\" mean? A Principal if fully disclosed ifthe 3rd party knows of the Principal's existence and identity. If the 3rd party lacks the necessary information to investigate the Principal, the Agent him/herself will have liability on the contract, but not necessarily the Principal. 0 Example: An Agent is purchasing a property from a 3'" party on behalf of a wealthy, fully disclosed Principal. If the Principal is \"fully disclosed\" to the 3rd party, the Agent will not necessarily have liability for claims arising from the contract [but the Principal will have liability for such claims on these facts}. Unidentied Principal The 3rd party can claim contract liability against either the Principal or the Agent in the case of an "unidentied Principal\" o What does \"unidentified Principal\" mean? That the 3rd party knew of the Principal's existence but not the Principal's identity. On those facts, both the Principal and the Agent are \"faintly and severally liable\" for claims from the 3"1 party arising from the contact. 0 \"Joint and Several tiabilitg\" is defined on p. 330 [Section 17-2b) as follows: "All members of a group re liable. They can be sued as a group, or any one of them can be sued individually for the full amount owed. But the Plaintiff cannot recover more than the total she is owed.\" 0 Example: An Agent is purchasing a property from a 3'\" party on behalf of an unidentified wealthy Principal (\"My client is a high ranking executive in Silicon Valley who prefers be remain anonymous\") On these facts, there isjoint and several liability for claims arising from the 3\"1 party under the contract for both the Agent and the Principal. Undisclosed Principal - The rule here is similar as with an unidentified Principal "the 3rd party can recover from either the Agent or the Principal\" lp. 331; Section 17b-2). What does \"undisclosed\" mean? That the 3rd party did not know either the Principal's identity or the Principal's existence. This concludes the discussion of Agency Law and contract liability. The discussion now turns to Agency Law and m liability. Principal liability for Torts lp. 331+; Section 17-2c] When is the Principal liable for torts that the Agent causes? Most cases of tort liability in Agency Law arise in an employment/se rvices context, and the general rule for this is set forth on p. 332 [Section 17-2c}: An employer {the Principal) is liablefor physical torts negligently committed by an emgloyee {the Agent) acting within the scoge of employment. It's important to note here the two separate parts ofthis rule 0 Liability arises only for acts committed by employees 0 Liability arises only for acts committed within the scope of employment This general rule is based upon the principle of Respondent Superior, which is a Latin phrase meaning \"Letthe Master Answer.\" Conceptually, it is the idea that the Employer [the master) is responsible for the torts committed by the Employee. Employees vs. independent Contractors: There is an important distinction in Age ncy Law, however, between Employees and independent Contractors. BUS! LECTURE 10A { Week 10) 1Why is this distinction important? Because the above rule about tort liabilityflowing to employers applies to employees but NOT to independent contractors (p. 332; Section 17-2c]. This distinction has become very important in recent years with the so-called rise of the "gig economy\". How is it determined whether an Agent who works for a Principal is an employee or an independent contractor? The rules are set forth in a set of bullet points on p. 332 [Section 17-2c}, but there is no clear bright line rule that distinguishes employees from independent contractors. Essentially, if the Principal has more control over the Agent, it's more likely that the Agent will be deemed under the law to be an Employee [whose torts the Employer is responsible for) rather than an Independent Contractor (whose torts the Employer is NOT responsible for]. The key variables considered in determining whether an Agent is an Employee or an Independent Contractor are as follows 0 The Principal supervises the details of the work 0 The Principal supplies the tools and the place of work 0 The Agents work full time for the Principal o The Agents receive a salary or hourly wages, not a fixed price for the job 0 The work is part of the regular business of the Principal o The Principal and Agents believe they have an employer-employee relationship 0 The Principal is in business. \"Scope of Emplogment\": Tort liabilityflows to Employers (Principals) only for acts committed by Employees (Agents} acting within the \"scope of employment\" What does "scope ofemployment\" in this context mean? The textbook provides a useful set of bullet points on p. 333-34 (Section 17-2c] that courts use to determine scope of em ployment an Employee (Agent] is acting within the scope of employment if the act o Is one that employees are generally responsible for o Takes place during hours that the employee is generally employed o Is part of the Principal's business o Is similar to the one the Principal authorized 0 Is one for which the Principal supplied the tools 0 Is not seriously criminal What Is a Fiduciary? Becca Stanek, June 11, 2020 (haps:/smartasset.com/financial-advisor/what-is-fiduciary-financial-advisor) In legal terms, a fiduciary is an individual or organization that has taken on the responsibility of acting on behalf of another person or entity with utmost honesty and integrity. For example, bankers, attorneys and officers of public companies are all fiduciaries, meaning they must act in the best interest of their customers, clients or shareholders. If they don't, they are legally liable. Similarly in the investment world, fiduciary financial advisors manage dient assets with the clients' best financial interests in mind. Therefore, be sure to limit your search for a financial advisor to only fiduciary advisors in your area What Is a Fiduciary? The term "fiduciary" is a good word to hear when you're searching for a financial advisor. An advisor that calls themselves a fiduciary seeks to minimize conflicts of interest, be transparent and live up to the trust placed in them. Fiduciary financial advisors must . Put their clients' best interests before their own, seeking the best prices and terms. Act in good faith and provide all relevant facts to clients. Avoid conflicts of interest and disclose any potential conflicts of interest to clients Do their best to ensure the advice they provide is accurate and thorough. Avoid using a client's assets to benefit themselves, such as purchasing securities for their own account before buying them for a client. Fiduciary usually refers to someone who manages assets on the behalf of an individual, a family, a company or any other entity. In addition to a banker or financial advisor, this person could be an accountant, executor, trustee or board member. In theory, a fiduciary can be anyone to whom you delegate your personal, legal or financial choices. What Is Fiduciary Duty? Fiduciary duty is a legal responsibility to put the interests of another party before your own. If someone has a fiduciary duty to you, he or she must act solely in your financial interests. A fiduciary cannot, for example, recommend a strategy that doesn't benefit you but instead provides a kickback. You can think of it like the doctor-patient relationship, where one party has a duty to provide the best care it can to the other party. Fiduciary duty is important for guiding the actions of the professionals who deal with clients' money. It's also important because, when violated, it provides an avenue for legal action. If a financial professional who isn't a fiduciary has been knowingly selling you low-performing, high- fee investments, you don't have the legal standing that you would have if the professional were a fiduciary. A breach of fiduciary duty occurs when a fiduciary fails to honor his or her obligation. A breach could happen if a fiduciary benefits from his or her recommendations, fails to provide proper guidance or acts in any way that's adverse to your best interests. Examples include: Account chuming (making an excessive number of trades to make commissions) Misrepresentation (making a false statement about a security transaction) Making unauthorized trades Acting negligently Fiduciaries can be held financially and civilly responsible for any actions they make that are not in your best interest. You are entitled to damages even if you don't incur harm. How to Know If a Financial Advisor Is a Fiduciary Al investment advisors registered with the U.S. Securities and Exchange Commission (SEC) or a state securities regulator must act as fiduciaries. Broker-dealers, stockbrokers and insurance agents are only required to fulfill a suitability obligation. This means that while they must provide suitable recommendations to their clients, they don't have to put their clients' interest before their own. There are several resources available that can help you know if an advisor is a fiduciary. The National Association of Personal Financial Advisors (NAPFA) has an online search tool that easy to find certified financial plan a. Every advisor in that system operates on a fee-only basis and promises to act as a fiduciary. Garrett Planning Network is another planner organization of fiduciary financial planners who charge an hourly rate. Additionally, the Certified Financial Planners Board has an advisor search tool. You can use it to look up a particular planner and see their experience and history. The vetting process shouldn't stop there. Once you identify potential advisors, here are the sorts of questions you should ask advisors to ensure that they suit your needs and have minimal conflicts of interest: How do you earn money? What certifications and licenses do you hold? What services do you offer? Who is your typical client? How often do you typically communicate with clients? Can you provide a written guarantee of your fiduciary duty? You should also request a copy of a financial advisor's Form ADV and Form CRS, which is paperwork the SEC requires advisory firms to file. This will provide information about an advisor's business, pay structure, educational background, potential conflicts of interest and disciplinary history. That information is also available online through the SEC's Investment Advisor Public Disclosure (IAPD) tool. You should also request a performance record and list of client references to contact. Why Working With a Fiduciary Financial Advisor Is Important Choosing a fiduciary financial advisor can give you greater peace of mind. With a fiduciary financial advisor, you'll know that the person managing your money must make decisions in your best interest. In general, fiduciary financial advisors tend to have fewer conflicts of interest and they're required to disclose any potential conflicts of interest that they have. Financial professionals who eam commissions may be incentivized to sell their own products even if there are comparable products available at a lower cost. Fiduciaries must seek the best prices and terms for their clients. Thus, if you work with a fiduciary you're more likely to and up with the product or recommendation that's truly right for you. In general, financial professionals bound by fiduciary duty tend to be more transparent. Fiduciaries must thoroughly discuss their decisions with their clients, providing all relevant information and pertinent facts. This makes it easier to ensure you understand the decisions that are being made in regards to your assets and financial future. While not all non-fiduciaries are necessarily bad actors, it's easier to ensure that you're working with someone who has your best interest if you opt to work with a fiduciary. Moreover, If you're working with someone who doesn't have a fiduciary duty to you, you have fewer legal options in The event that you discover your interests haven't been served. Fiduciary Duty vs. Suitability Rule Some financial professionals such as investment brokers and insurance agents aren't bound by fiduciary duty. Instead, they're only required to fulfill a suitability obligation. While fiduciaries must put their clients' best interests before their own, financial professionals who adhere to the suitability standard must only provide suitable recommendations to their clients. To determine whether a recommendation is suitable, these professionals must consider your financial situation, goals and risk tolerance. Additionally, they must ensure that you won't incur excessive costs and that excessive trades won't be made. However, they may still suggest products that aren't necessarily in your best interest or that benefit them more than they do you. Here's a detailed comparison of fiduciary duty and the suitability rule: Suitability Rule vs. Fiduciary Duty Suitability Standards Fiduciary Standards Recommendation Recommendations must be Recommendations must be in Requirements suitable for the client client's best interest Disclosure Less strict rules regarding Required to disclose conflicts Requrements disclosure of conflicts of interest of interestHere's a detailed comparison of fiduciary duty and the suitability rule: Suitability Rule vs. Fiduciary Duty Suitability Standards Fiduciary Standards Recommendation Recommendations must be Recommendations must be in Requirements suitable for the client Client's best interest Disclosure Less strict rules regarding Required to disclose conflicts Requrements disclosure of conflicts of interest of interest Loyalty Requirements May be loyal to the broker-dealer. Must be loyal to the client and not necessarily the client act in good faith The Department of Labor (DOL) Fiduciary Rule The term fiduciary" has made headlines over the last few years thanks to the Department of Labor's (DOL) fiduciary rule. The rule required any financial professionals - including brokers and insurance dealers - who provide retirement advice or work with retirement plans to act as fiduciaries. The Obama administration proposed this rule to create greater transparency around retirement planning. The rule required financial professionals to disclose potential conflicts of interest and clearly state fees and commissions. The Obama administration said the rule could save Americans as much as $17 bilion a year due to conflicted advice. However, as of June 2018, the fiduciary rule is effectively dead. After President Trump took office, he delayed the rule's implementation due to resistance from the financial industry. Opponents argued that the rule would make it more expensive for advisors to manage smaller accounts, in turn making it harder for lower-income investors to get financial advice. Then, in June 2018, the Fifth Circuit Court confirmed that it had finalized is decision to end the fiduciary rule. The court argued that the Department of Labor had overstepped its authority to regulate financial services and providers. President Trump has requested that the DOL look over the rule once again and prepare an analysis. The DOL could then ask the court to review the rule again, or the fiduciary rule could even make his way up to the Supreme Court Is a Robo-Advisor a Fiduciary? A robo-advisor is a great alternative for investors who perhaps can't afford the account minimums and management fees of a traditional financial advisor. But the question of whether robo-advisors are fiduciaries is one that's up for debate in the financial services industry. Robo-advisors that hold a registration with the SEC insist that they are fiduciaries. As registered resiment advisors, they are required to act in their clients' best interests. Furthermore, robo- advisors that offer advice on 401(k) plans must comply with ERISA's fiduciary rules. Robo- advisors also don't sell proprietary products. The other camp argues that only human advisors can truly embody the fiduciary role. Robo-advisors typically only offer investors advice based on their goals, rather than their full financial situation. This limits the scope of their advice and can make it less personalized than a traditional advisor's. Bottom Line When you're working with a financial professional, it's key to find out if he or she follows the fiduciary standard. A fiduciary has different obligations than someone bound only by the suitability rule. Fiduciaries must always act in their clients' best interest - and if they don't, you have legal options to pursue. Ultimately, when it comes to choosing someone to manage your money, you should find someone you can trust.BUSl .18 WORKSHEETIOA {WEEK 10) Please submit responses to the following questions (1) In Agency Law, what is an Agent? What is a Principal? Please illustrate with a brief example. (2} Are all financial advisors duciaries? Explain. {It will be helpful in answering this question to make reference to the linked article \"What is a Fiduciary\" that is on the Canvas lecture page that corresponds to this worksheet} What are the two different standards for financial advisors? Explain briefly the different standards in a sentence or two. (3} Bill is a real estate agent, and Susan has engaged Bill to help her buy a house. Susan tells Bill that Susan can afford to pay a maximum of $600,000 for the house purchase, but that she would like the best deal possible. Bill shows Susan a house for sale that Susan likes very much (nice neighborhood; good schools; close to work; etc.) with an asking price of $550,000. Susan {with Bill's help} makes an offer to purchase the house for $500,000. The seller's agent receives Susan's offer to purchase the house for $500,000 and calls Bill [Susa n's real estate agent) to discuss Susa n's offer with Bill. During that discussion, the seller's agent casually inquires of Bill what the maximum amount Susan can pay is. Bill replies "Susan told me that the maximum she can afford to pay is $600,000." [Note that Bill's real estate commission is calculated as a percentage of the real estate transaction price {typically 3%), and that Bill will make more money in commission with a higher priced transaction. if the house sells for $500,000, Bill's commission for acting as Susan's agent will be $15,000 {3% of$500,000),' if the house sells for $600,000, Bill's commission will be $18,000 {3% of $600,000\" The seller then rejects Susan's offer of $500,000 and makes a counter-offer to Susan of $599,950. Susan, who really wants the house, then reluctantly accepts the counter-offer and pays $599,950 [just $50 under the maximum she can afford], wishing very much that she had been able to purchase the house more cheaply. Has Bill done wrong on these facts? Explain. (4} List and explain {with a sentence or two) 2 of the more detailed elements of the Duty of Loyalty that Agents owe Principals. (5} You are a student who is currently enrolled in BUSI 18 at Foothill College, and you have been taking BUSI 18 from me for several weeks now. I am your instructor, and I have been teaching BUSI 18 to you for several weeks now. Do we (instructor and student] have a Principal-Agent relationship? Do we {instructor and student} have a duciary relationship? Explain why or why not in a few sentences. [HlNT: The correct answer is that we do n_ot have either relationship. in your response, you should explain why not.]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Law Questions!