Question: Last question answer options: decrease, increase. Brandon is an analyst at a wealth management firm. One of his clients holds a $10,000 portfolio that consists

Last question answer options: decrease, increase.

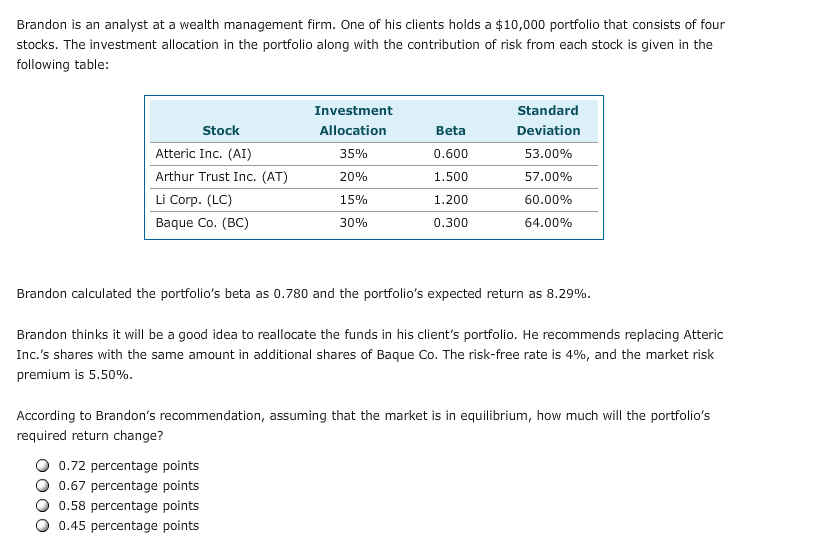

Brandon is an analyst at a wealth management firm. One of his clients holds a $10,000 portfolio that consists of four stocks. The investment allocation in the portfolio along with the contribution of risk from each stock is given in the following table Investment Allocation 35% 20% 15% 30% Standard Deviation 53.00% 57.00% 60.00% 64.00% Stock Atteric Inc. (AI) Arthur Trust Inc. (AT) Li Corp. (LC) Baque Co. (BC) Beta 0.600 1.500 1.200 0.300 Brandon calculated the portfolio's beta as 0.780 and the portfolio's expected return as 8.29% Brandon thinks it will be a good idea to reallocate the funds in his client's portfolio. He recommends replacing Atteric Inc.'s shares with the same amount in additional shares of Baque Co. The risk-free rate is 4%, and the market risk premium is 5.50% According to Brandon's recommendation, assuming that the market is in equilibrium, how much will the portfolio's required return change? O 0.72 percentage points O 0.67 percentage points O 0.58 percentage points O 0.45 percentage points

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts