Question: Lecture 1 - Chapter 19 - Job Order Costing review of Chapter 18 PAGE 1 of 6 I will place emphasis for Chapter 19 on

Lecture 1 - Chapter 19 - Job Order Costing review of Chapter 18 PAGE 1 of 6

I will place emphasis for Chapter 19 on your ability to move costs through a job order system utilizing the required journal entries to show your understanding of job cost. You will be tested on journal entries in this chapter to prove your mastery of the material in the chapter. For a quick overview lets step back and think about what we talked about in Chapter 18 Managerial Accounting Concepts and Principles. We learned that managerial accounting is internal reporting and recording of cost events. We used a Schedule of Cost of Goods Manufactured (COGM) to arrange our accounts used in cost reporting to give meaning to our cost of manufacturing. To confirm with you the Schedule:

Add Direct Materials Used DM

Add Direct Labor Used DL

Add Factory Overhead Used FOH

Then add Beginning WIP Beg WIP

Subtract Ending WIP (End WIP)

This gives us Cost of Goods Manufactured COGM

We also learned that the COGM flows into the Income Statement via an addition in the Cost of Goods Sold section of the Income Statement. Cost of Goods Sold is calculated starting with:

Finished Goods Inventory from the Beginning of the period Beg FG

Add: COGM COGM

Subract: Finished Goods Inventory from the End of the period (End FG)

Gives: Cost of Goods Sold COGS

To review the Income Statement: The Income Statement uses Cost of Goods Sold (COGS) subtracted from Net Sales to give Gross Profit for the period. It looks like this: Sales Less: Sales Returns, Allowances, Discounts. Gives: NET SALES

Less: COGS

When we subtract COGS from Net Sales we get: Gross Profit

Chapter 19 Page 2 of 6

Managerial Accounting is just a plant or factory wide information system. Accumulating the plant or factory costs incurred (that is used) into accounts that we can arrange into reports. NEW ACCOUNTS WE WILL USE IN MANAGERIAL/COST ACCOUNTING. The following accounts are Inventory accounts and are current assets with a debit balance. Work in Process Inventory, Raw Materials Inventory and Finished Goods Inventory. General information and definitions that might be helpful: Work in Process WIP work that has been started in production but not completed. Raw Materials Inventory RM - goods purchased for use in production and in the factory. Finished Goods Inventory - FG - completed goods that are ready to sell

The next group of accounts are cost that we incur in the manufacturing process: Direct Materials - Raw materials used that go directly into the product being made. Indirect Materials - Raw materials used in the production/factory facility but do not go directly into the product.. Direct Labor DL peoples wages that manufacture our goods. Indirect labor peoples wages that work in the manufacturing facility but do not make the goods. Factory Overhead FOH - indirect costs that are accumulated in the FOH account and then applied to WIP through an overhead rate, this includes Indirect Labor and Indirect Materials.

YOU NOW HAVE THE TERMINOLOGY AND ACCOUNT NAMES, SO LETS LOOK AT WHAT JOURNAL ENTRIES WE CAN MAKE WITH THEM IN JOB COST ACCOUNTING

Chapter 19 PAGE 3 of 6

NOW lets get those pesky journal entries down this will explain how the Costs are gathered in accounts! You need to be able to write these entries based on information that I give to you on your test for this chapter.

MATERIALS

Buy Raw Materials: (both direct and indirect materials) Debit Raw Materials Credit A/P or cash

SEE MATERIALS PURCHASES PAGE 691

___________________________________________________________________________

Requisition direct raw materials into production: Debit Work in Process Credit Raw Materials

SEE RECORDING DIRECT MATERIALS USED NEED TO KNOW 19-2 PAGE 692

_____________________________________________________________________________

Use indirect materials (Factory Supplies) in our manufacturing plant: Debit FOH Credit Raw Materials

SEE RECORDING INDIRECT MATERIALS USED PAGE 697

LABOR Page 4 of 6

Pay people that directly make the product we are producing: Debit Work in Process Credit Wages Payable

SEE RECORDING DIRECT LABOR USED PAGE 694 Need to Know 19-3

Pay people that work in our factory but are indirectly involved with the manufacturing process: ( do not make the product but work in the factory) Debit FOH Credit Wages Payable

SEE RECORD INDIRECT LABOR USED PAGE 698

Chapter 19 Page 5 of 6

FACTORY OVERHEAD PAGE 694 IN BOOK

- ACCUMULATE FACTORY OVERHEAD IN THE FOH ACCOUNT.

We discussed this in chapter 18 as they do in chapter 19 that indirect labor, indirect materials used AND factory rent, factory taxes, factory insurance, factory maintenance - gets debited to the FOH account and credited to Accounts Payable or Wages Payable. IN YOUR BOOK THIS IS RECORDING Other Overhead Costs PAGE 697. Debit FOH. Credit A/P

SEE NEED TO KNOW 19 5 for a good example of accumulating factory overhead into the FOH account.

- APPLY FACTORY OVERHEAD TO WORK IN PROCESS

In Chapter 19 we apply Factory Overhead to the WIP account at a pre-determined rate. Usually based on Direct Labor hours used or machine hours used. That is a dollar amount per hour of direct labor used or machine hours used.

SEE NEED TO KNOW 19-4 Recording Applied Overhead

EXAMPLE: if we used 10,000 hours of direct labor and we applied factory overhead at a rate of $2.00 for each hour of direct labor used we would: Debit: WIP (for 10,000 hours at the rate of $2 per hour) $ 20,000 Credit: FOH (for 10,000 hours at the rate of $2 per hour) $20,000

SELLING THE GOODS WE HAVE FINISHED. Now that we have made our goods and moved them to Finished Goods Inventory lets sell them:

The first entry is at cost - Debit Cost of Goods Sold. Credit Finished Goods Inventory

The second entry is at selling price - Debit A/R or cash. Credit Sales

******************************************************************************************************************************************************

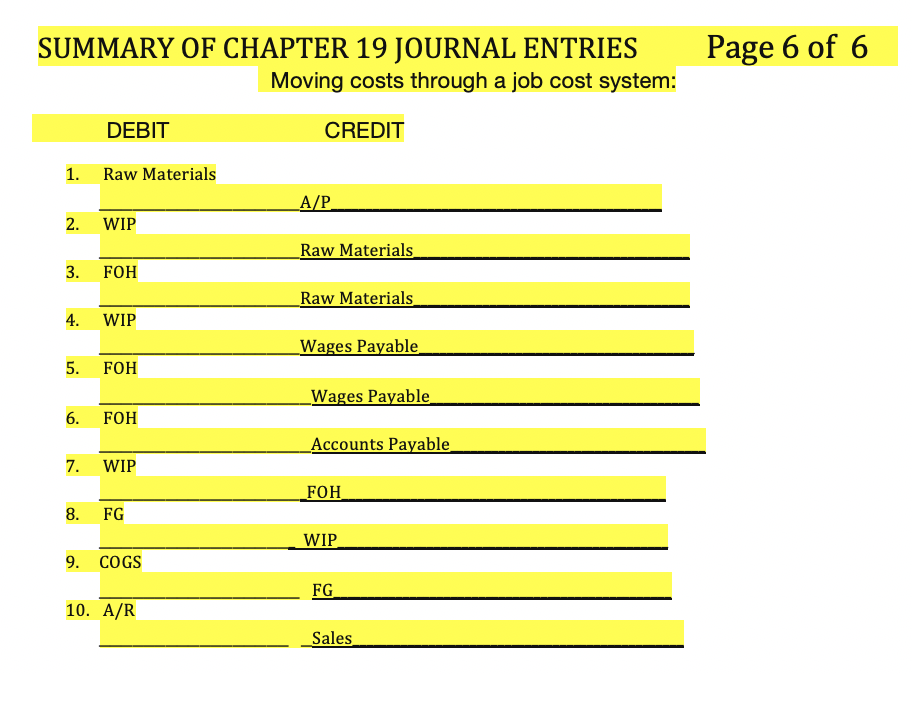

Please help! The highlighted picture below the ****** line is what I need solved. everything above the ******* line will help solve everything below the ******** live.

For your first graded assignment go to the last page of the lecture notes on Chapter 19, page 6. On Page 6 you will find a series of journal entries numbered 1 through 10. Please number a document with lines 1, 2, 3, 4, 5, 6, 7, 8, 9, and 10 and put your name in the upper right hand corner of the document. Beside each number (1 through 10) WRITE the correct description of the journal entry that corresponds to that number on page 6 of lecture notes for week 1 online chapter 19.

Page 6 of 6 SUMMARY OF CHAPTER 19 JOURNAL ENTRIES Moving costs through a job cost system: DEBIT CREDIT 1. Raw Materials A/P 2. WIP Raw Materials 3. FOH Raw Materials 4. WIP Wages Payable 5. FOH Wages Payable 6. FOH Accounts Payable 7. WIP _F0H 8. FG WIP 9. COGS FG 10. A/R _Sales

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts