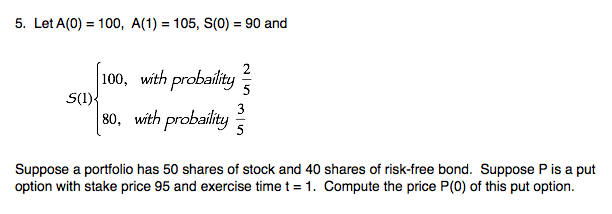

Question: Let A(0) = 100, A(1) = 105, S(0) = 90 and S(1) = {100, with probability 2/5 80, with probability 3/5 Suppose a portfolio has

Let A(0) = 100, A(1) = 105, S(0) = 90 and S(1) = {100, with probability 2/5 80, with probability 3/5 Suppose a portfolio has 50 shares of stock and 40 shares of risk-free bond. Suppose P is a put option with stake price 95 and exercise time t = 1. Compute the price P(0) of this put option

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock